MasterCard & Visa announced strong quarter financial results

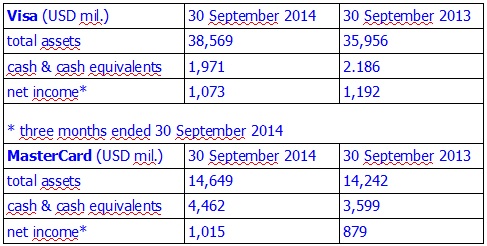

At the end of septembrie 2014, the total assets of the two companies represents more than USD 53,000 mil., out of which 12% stands for cash and cash equivalents. This special item from the balance sheet is twice bigger for MasterCard compared to Visa (see table). For the three months ended 30 September 2014, both companies reported net income that exceeds USD 1 bln.

For the three months ended 30 September 2014, MasterCard reported net income of $1 billion, up 15% versus year ago period. Net revenue for the third quarter of 2014 was $2.5 billion, a 13% increase versus the same period in 2013.

Net revenue growth was driven by the impact of the following:

. A 12% increase in gross dollar volume, on a local currency basis, to $1.2 trillion;

. An increase in cross-border volume of 15%; and

. An increase in processed transactions of 10%, to 11 billion.

For the nine months ended September 30, 2014, MasterCard reported net income of $2.8 billion, up 13%. Net revenue for the nine months ended September 30, 2014 was $7.1 billion, an increase of 13% versus the same period in 2013.

Visa also reported a better-than-expected adjusted quarterly profit and said the mobile payment industry would be „a great driver” for business. Several analysts have estimated that mobile payments will be a $1 trillion global industry by 2017.

„We have our traditional ways of doing business but … we see the mobile opportunities in both the developing, the less developed and the developed world being great drivers,” Visa Chief Executive Charlie Scharf said on a conference call.

For the fiscal fourth quarter of 2014, Visa Inc. announced a GAAP net income of $1.1 billion or $1.72 per share, a decrease of 10% and 7% over the prior year, respectively. GAAP net income for the full-year 2014 was $5.4 billion or $8.62 per share, an increase of 9% and 14% over the prior year, respectively.

Payments volume growth, on a constant dollar basis, for the three months ended June 30, 2014, on which fiscal fourth quarter service revenue is recognized, was 12% over the prior year at $1.2 trillion. Payments volume growth, on a constant dollar basis, for the three months ended September 30, 2014, was 11% over the prior year at $1.2 trillion. Cross-border volume growth, on a constant dollar basis, was 10% for the three months ended September 30, 2014. Total processed transactions, which represent transactions processed by VisaNet, for the three months ended September 30, 2014, were 16.9 billion, a 9% increase over the prior year.

For the fiscal full-year 2014, service revenues were $5.8 billion, an increase of 8% over the prior year. Data processing revenues rose 11% over the prior year to$5.2 billion. International transaction revenues, which are driven by cross-border volume, grew 5% over the prior year to $3.6 billion. Other revenues, which include the Visa Europe licensing fee, were $770 million, a 7% increase over the prior year. Client incentives, which are a contra revenue item, were $2.6 billionand represent 16.9% of gross revenues. Total processed transactions, which represent transactions processed by VisaNet for the twelve months ended September 30, 2014, totaled 64.9 billion, an 11% increase over the prior year.

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: