The pandemic supercharged digital banking—and this shift created an array of new challenges. Forward-thinking banks will keep investing in digital to meet the competitive challenges while also balancing their customers’ need for branches and advisers.

For this year’s Retail Banking Radar, Kearney surveyed more than 7,500 consumers across 13 countries. They found that while COVID-19 has led to a permanent shift in digital behaviors for most consumers, some are partially returning to a preference for in-person banking (see figure 1). However, the preference for digital channels, mainly mobile, remains robust as banks seek to service the divergent preferences of their customers: one-third online, one-third offline, and one-third a mix of these two.

Consumers’ use of digital channels ramped up during the pandemic, with the preference for digital channels jumping from 20 percent to 50 percent—a rise that under normal circumstances would have taken years, potentially a decade to reach (see figure 2). Kearney 2022 Retail Banking Radar study shows a slight decrease in digital usage across most European countries, indicating that parts of the population are partially returning to pre-lockdown behaviors, with preferences for digital channels reduced by 5 percentage points.

Across all products, around half of Europeans prefer doing their research on digital channels: 55 percent prefer researching their next bank account or card online, 49 percent when it comes to savings and consumer finance, and 46 percent when looking for a mortgage.

The products most frequently signed for in digital channels are transactional (48 percent) followed by savings (45 percent) and consumer loans (43 percent). Mortgages—because of the complexity of paper processes and the need for advice—are closed online by only 39 percent of consumers. Indeed, mortgages experienced the most significant drop in digital sales between 2021 and 2022, with that figure falling from 47 percent.

Kearney study also shows that 21 percent of Europeans never go to a bank branch and carry out all of their banking remotely—a figure that almost doubled during the pandemic, rising from 12 percent in 2019 (see figure 3). Meanwhile, more than a quarter (26 percent) say they visit a branch no more than once a year.

By contrast, branches still perform an important role for the third of European retail banking customers who visit at least once a month, usually for a cash transaction rather than for advice or to purchase products. Kerney study shows that branches are least in demand in the Netherlands, where a third of those surveyed never visited one before the pandemic. In 2022, this figure grew to 48 percent. By contrast, branches are used most frequently in Germany, where 48 percent of consumers say they visit at least once a month.

One might think that multichannel behaviors have become the norm and could account for the majority of customer journeys across Europe. However, Kearney study shows that only a third of consumers research and then purchase online across all products, while a third still research and purchase either in a contact center or in a branch through an independent financial advisor (see figure 4).

And only a third of consumers switch channels. In most cases, they do their research online but then make the purchase in a branch. Ultimately, there is no clear pattern across Europe. Throughout these customer journeys, however, face-to-face personal interactions are still highly valued.

Younger consumers may be more tech-savvy, but they are looking for an omnichannel experience—balancing the ease of online and mobile banking with in-person advisory for support and education around products such as mortgages and long-term savings.

With at least two-thirds of Europeans researching their banking purchases online, price comparison websites have become more prevalent, posing a threat to banks by commoditizing products based only on price (see figure 5). The most important guiding criteria is the interest rate offered on a loan or deposit, leaving all other considerations—from customer service to advice—as secondary. Across Europe, 9 percent of consumers research their next purchase in this way, with 5 percent buying directly through this channel. An additional 3 percent research and purchase through social media.

Consumers’ use of price comparison websites differs by country. In the United Kingdom, 16 percent use these websites for research and 9 percent for purchases, with Italy and Germany closely following for research at 12 percent. In Sweden, nine out of 10 follow up their research at such an online portal with a purchase. The product most frequently purchased via these websites, in part because of the ease of closing online, is consumer lending.

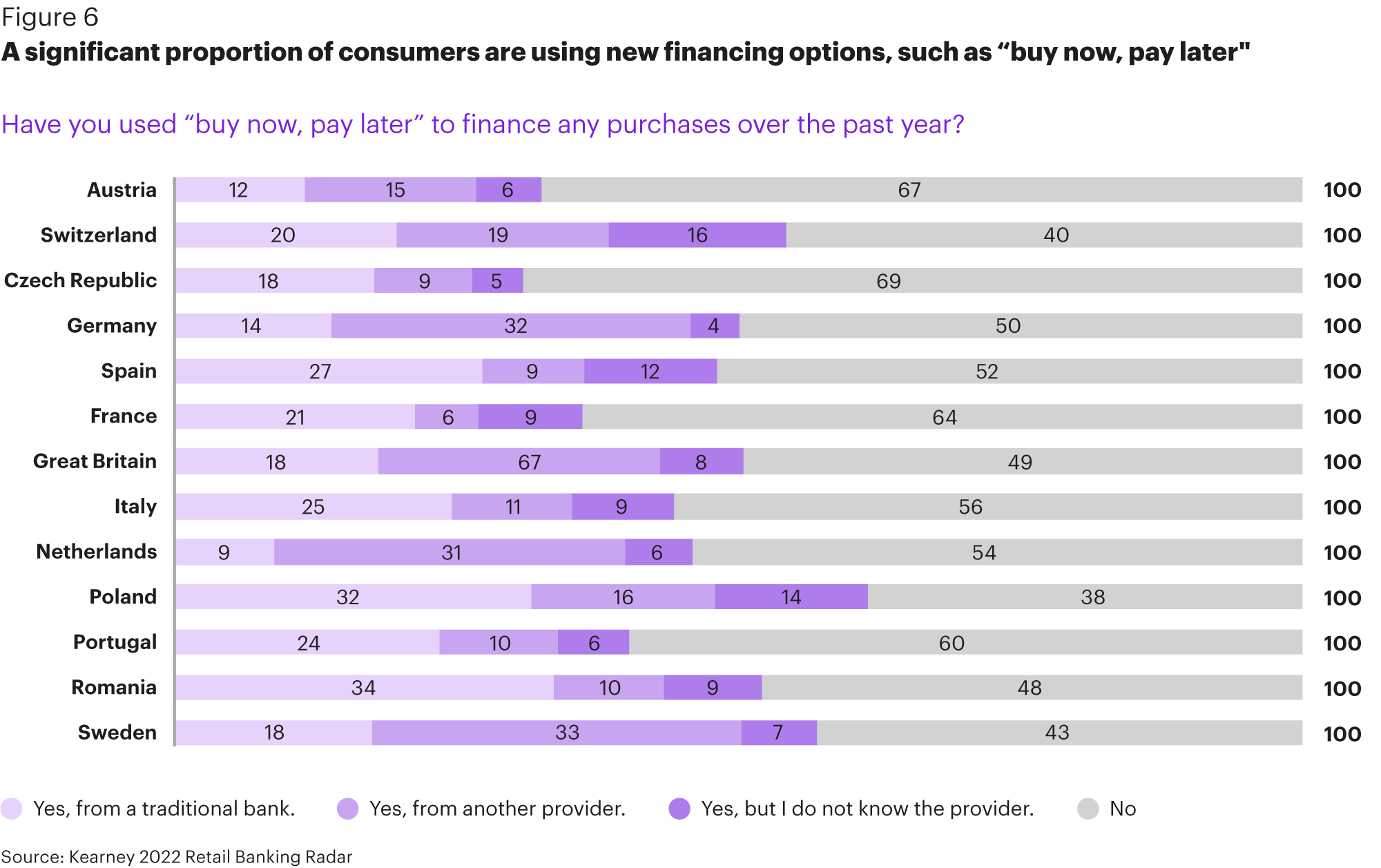

Changing customer behaviors have also led to new embedded finance options, such as the emerging buy-now, pay-later (BNPL) models that have gained significant share (see figure 6). Almost half of Europeans have already used BNPL: Poland and Sweden lead the way with 62 percent and 57 percent respectively, while the Czech Republic and Austria have been slower to adopt on only 31 percent and 33 percent. There are also key differences between markets in terms of the providers. In some countries, 80 percent of BNPL is via the banking sector, whereas in others, such as the United Kingdom and Germany, 80 percent is outside of the banking sector and now a growing threat to retail banks.

Across all European markets, 37 percent of the consumers we surveyed who have used BNPL have used it from a non-bank provider, while 47 percent have used this option from a traditional bank (but not always their home bank).

The transformation needs to accelerate. The goal for banks must be to develop end-to-end digital capabilities across all products, making them intuitive and easy to use while offering new services to compete with digital native neobanks. Progress needs to be quicker and not just for simple journeys such as opening a current account.

Face-to-face advice remains essential, particularly for more complex products such as mortgages and wealth management. Despite the shift to digital, personal interaction is still highly valued. There will always be moments when FAQs and chatbots can’t help customers and where a face-to-face discussion is crucial, either in a branch, reviewing their role and model, or via a video call.

Embedded finance is becoming more important. Consumers are embracing the convenience and simplicity of embedded finance options, such as BNPL. The seamless access to financial services as part of the digital shopping experience will continue to fuel their growth. Retail banks will need to take a clear position on if and how they will participate in this growing field and better focus their strategies on open banking, leveraging the level of trust with their customers. As part of improving the customer experience, embedded finance allows for better monetization of financial products, which can aid the stagnating topline results of retail banks.

The risk of disintermediation is real and growing. Despite the importance of personal interactions, the rise of embedded finance and the continued growth of price comparison websites pose a threat to banks’ traditional role in the ecosystem—with both the ownership of their customer relationships and revenue streams at risk, particularly amid the ongoing growth of digital adoption and e-commerce.

Banks have already made a commitment to becoming digital first, in terms of both customer interactions and daily operations. However, considering the continuous pressure on costs, they will need to smartly prioritize their digital investments, understanding which part of the customer journey should be fully digital. Also, the role of the advisor—either in person or remote—must be managed thoughtfully within future operating models.

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: