![]()

![]()

an article written by David Birch, advisor, influencer, best selling authors, world-class speaker on fintech

Elon Musk has talked about plans to turn Twitter, now known as X (or TwiX, to me) into a payments platform that will give users the ability to send money to one another and move money into and out of bank accounts. The company has committed to launch peer-to-peer payments, „unlocking more user utility and new opportunities for commerce, and showcasing the power of living more of your life in one place”. This is part of what seems to be a wider vision of X as a a kind of “super app”, a Western version of WeChat, where users will read the news, book travel, pay taxes and everything else. It’s an exciting and challenging goal, but I think it’s going to be difficult to disrupt this particular market.

People who are tweeting from time to time (eg, me) tend to think that everyone is on X. But they are not. It is not even in the top 10 most used social media networks. Facebook has more than three billion monthly active users, whereas X has a tenth of that and most of them are not particularly active, since data shows that almost all tweets (92%) come from just 10% of them. Most people come to X to check in on the news or find entertainment rather than to contribute to the sum total of human knowledge.

Nonetheless, there are users (mostly male, dominated by the 25-34 age group) who do represent a monetisable pool of potential financial services customers and it is a plausible hypothesis that I might pay a friend who uses X for a Taylor Swift ticket by sending them money from my bank account to their bank account using X (rather than my bank’s instant payment option) if it easy and convenient.

Central to this grand vision are Money Transmitter Licenses (MTLs), and at the time of writing X has already obtained a bunch of these licences. Amercia has no equvialent of the European Payments Institution licence, so companies have to obtain these licences in every state, which is time-consuming (Mr. Musk says he undderestimated that) and tedious. It is, however, a necessary first step on the journey to replace Citi and Revolut, Wise and Wells Fargo on users’ home screens.

But what is a money transmitter licence? Writing in the Journal of Payments Strategy & Systems 17(3): 315-322 (Fall 2023), Ximeng Tang (an associate at Goodwin Procter LLP) explains that the Bank Secrecy Act of 1970 (BSA) and the regulations implemented by the Financial Crimes Enforcement Network (FinCEN) impose customer identification, reporting and other compliance requirements on regulated financial institutions, includng Money Services Businesses (MSBs). MSBs provide a number of different financial services, including:

Put another way, MSBs are non-bank financial companies with three general functions: receiving and sending money on behalf of consumers; providing products that receive, store, or send money for consumers; and providing an exchange for currencies. MSBs that are money transmitters are regulated and licensed at the state level and, as the Congressional Research Service report on the regulations notes, the terms money transmitter and MSB are effectively synonymous. Indeed, for the purposes of the BSA, a ‘money service business’ (MSB) is a regulated businesses that includes a money transmitter. Most companies providing domestic and international money transfer services are MSBs, such as Western Union and PayPal, as well as some payment processors such as Square and Stripe.

A fundamental element in FinCEN’s interpretation of a money transmitter is that the person must engage in both ‘acceptance’ and ‘transmission’ of money to be a money transmitter. Although “acceptance” is not defined (and as it happens neither is “transmission”), a number of interpretive letters issued by FinCEN suggest that they key is the control of the funds and where they are directed to, which seems liek a good working definition: if X routes the money from me to the person with the Taylor Swift tickets, they are a money transmitter. Which is why they need these licences.

Money transmitters play a crucial role in America’s financial ecosystem which is why they are subject to these regulatory obligations including background checks on officers, maintaining sufficient liquid assets, periodic reports and (here comes the hard part) AML compliance including customer identity verification and transaction monitoring. The mixture of varying state regulations and the fact that America has no digital identity infrastructure (nor does the UK) so that means compliance is expensive and inconvenient and, as has been obvious for some time, undeniably inhibits valuable innovation by forcing startups to spend dollars on lawyers instead of new products and services.

(It should be noted that things are changing on the MTL front. Many states have already opted to adopt the Model Money Transmission Modernization Act (MTMA), sample legislation developed by the Conference of State Bank Supervisors to establish nationwide standards and requirements for licensed money transmitters. For traditional money transmitters and new fintech entrants, the MTMA has the potential to reduce compliance burdens, encourage innovation, and remove barriers to entry for new market participants. It is very important given the growth in person-to-person payments via apps. Among all US consumers, half of P2P payments were sent using noncash methods in 2022, up from less than a third two years previously.)

But back to Mr. Musk and his plan. While the potential is undoubtedly great (WeChat’s payment revenues are heading towards $100m per annum), I rather agree with Sangeet Paul Choudary, a global expert on platform economics and network effects, who says that „Payments cannot just be bolted on”. His point is that there must be some organic use case within the TwiX ecosystem (he uses the analogy of the red packets that triggers WeChat’s payment hockey stick) „

In the US context, the provision of peer-to-peer transfers is, as American Banker put it, a “more modest plan” than the global payments system that he was going to build sometime this year, but it is realistic.

But what I keep wondering is why Mr. Musk is bothering with all of this. In order to offer payment services to American users, X will need licences that will cost several million dollars according to Aaron Klein, a senior fellow focused on financial technology and regulation at the Brookings Institution. Why would Mr. Musk want to spend a ton of money on AML compliance and identity verification?

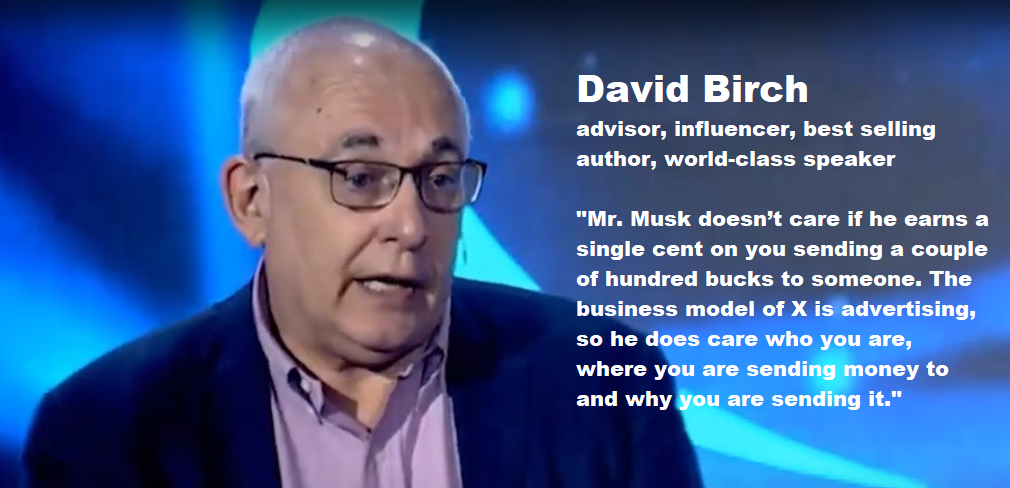

Perhaps this really all about identity, not money. Mr. Musk doesn’t care if he earns a single cent on you sending a couple of hundred bucks to someone for that Taylor Swift ticket. The business model of X is advertising, so he does care who you are, where you are sending money to and why you are sending it.

That data is worth vastly more than any transaction fees he might be able to collect from you.

Banking 4.0 – „how was the experience for you”

„So many people are coming here to Bucharest, people that I see and interact on linkedin and now I get the change to meet them in person. It was like being to the Football World Cup but this was the World Cup on linkedin in payments and open banking.”

Many more interesting quotes in the video below: