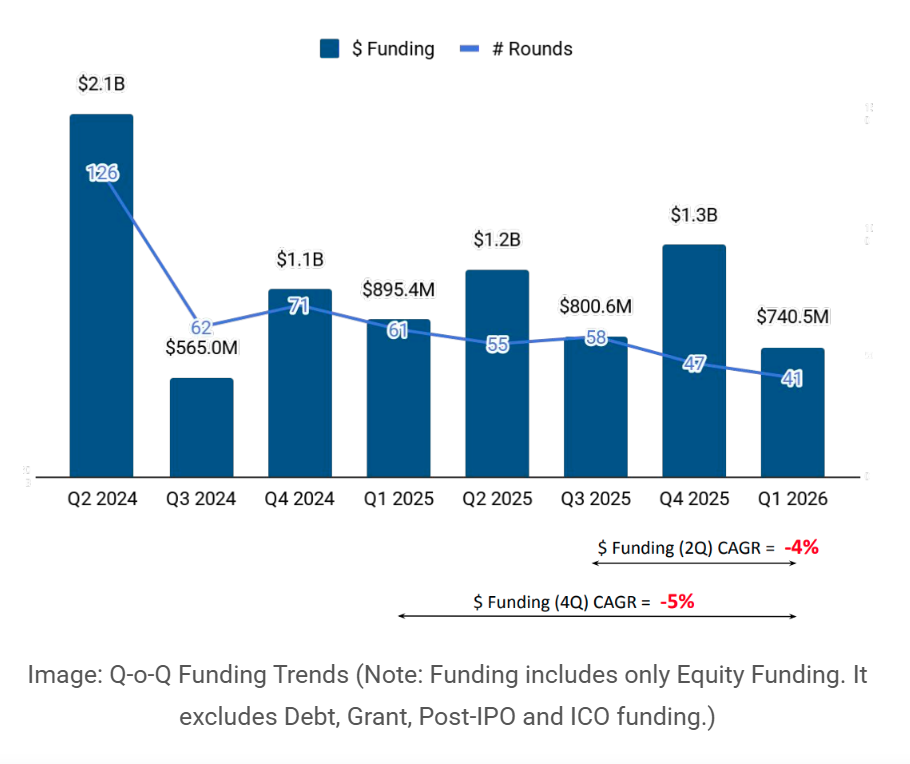

UK Fintech raises $741M in Q1 2026 – down 43% from the $1.3bn raised in the previous quarter

The UK Fintech Quarterly Funding Report from data intelligence platform Tracxn, found that $741m was raised across 41 funding rounds. However, this represents a fall of 43% from the $1.3bn raised in the previous quarter.

Tracxn Technologies Limited, a leading data intelligence platform, today released the UK Fintech Quarterly Funding Report – Q1 2026, a comprehensive analysis of funding activity, investor behaviour, exits, and geographic trends across the United Kingdom’s financial technology sector.

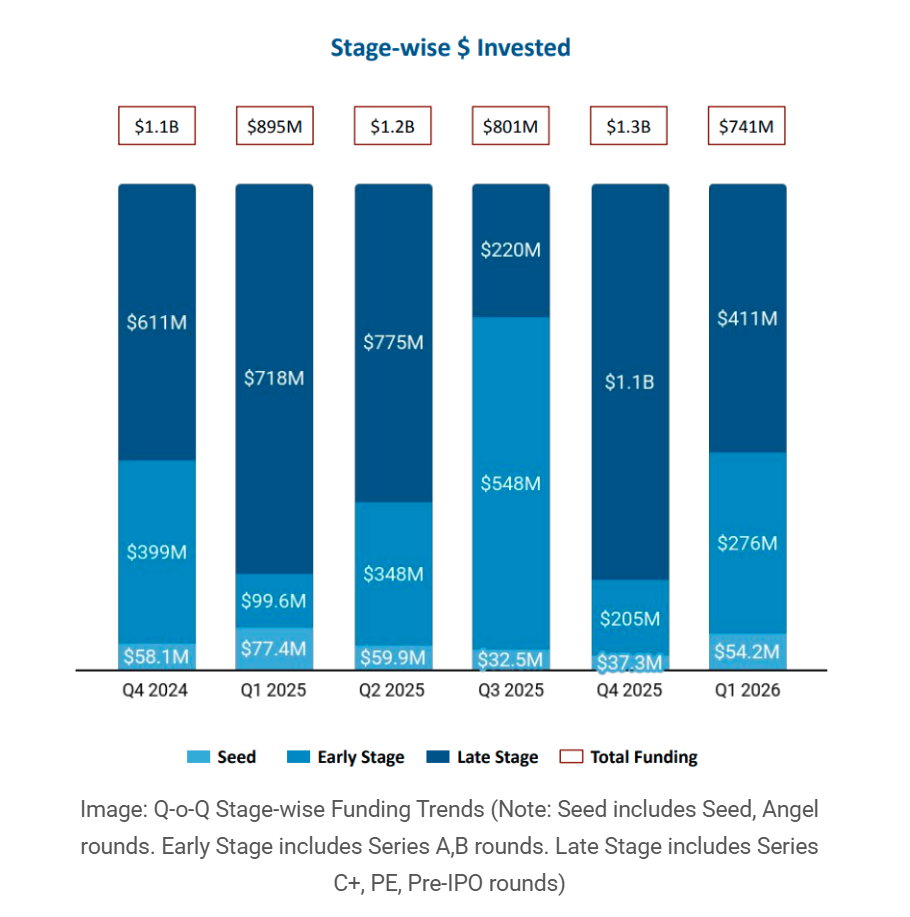

UK Fintech raised $741M across 41 rounds in Q1 2026 – a 43% decline from $1.3B in Q4 2025, yet the quarter’s composition tells a different story. Early-stage funding rose 35% vs Q4 2025 and 177% vs Q1 2025, seed funding climbed 46% vs Q4 2025, and four companies joined the Soonicorn Club. Late-stage funding contracted 62% vs Q4 2025 to $411M, driving the aggregate decline – but a closer read suggests investors are repositioning rather than withdrawing.

The most significant structural shift in Q1 2026 was the divergence across funding stages. Early-stage investment reached $276M – up 35% from $205M in Q4 2025 and 177% above $99.6M in Q1 2025 – even as the overall market declined, underscoring that compression was concentrated at the top of the funding ladder.

Late-stage funding bore the full weight of the retreat, falling 62% from $1.1B in Q4 2025 to $411M, with only two rounds exceeding $100M – 9fin Technologies ($170M, Series C) and Allica Bank ($155M, Series D) – while seed funding reached $54.2M, up 46% from $37.3M in Q4 2025, with 41 total rounds reflecting fewer but larger cheques being written across all stages.

Key Highlights:

. $741M raised in Q1 2026 – down 43% vs Q4 2025 and 17% vs Q1 2025. Late-stage compression drove the decline, while seed and early-stage funding grew sequentially – signalling a market rebalancing toward earlier bets rather than a broad-based pullback.

. Early-stage funding surged 177% vs Q1 2025, reaching $276M. Investors are doubling down on the next generation of UK Fintech companies – backing earlier and with greater conviction, as early-stage emerges as the dominant force shaping UK Fintech’s next cycle.

. Allica Bank emerged as Q1 2026’s sole unicorn, having raised $334M in prior funding. A longer, more capital-intensive path than the global tech unicorn average – reflecting the distinct demands of building a regulated banking institution.

. 22 acquisitions in Q1 2026 – down 39% vs Q4 2025 and 27% vs Q1 2025, yet consolidation concentrated at the top. Three deals – BVNK ($1.8B), Reward ($230M), and Flock ($109M) – accounted for the bulk of exit value: fewer transactions, larger bets.

. London dominated with 97% of all funding at $718M, as Belfast ($12M) and Cambridge ($8M) made their first appearances in the top cities. Regional hubs are beginning to stir in an otherwise concentrated ecosystem.

Read the full Report

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: