The fintech unicorns now, an endangered species

an article written by Isabel Woodford

The fintech bull run looks like it’s run out of steam and investors say the mightiest companies will fare the worst.

Fintech startups have enjoyed booming valuations over the last five years. But with public stocks now in freefall amid Covid-19 fears, the private fintech bubble is looking fragile — with the highest-value companies most at risk.

A report by Rosenblatt Securities, a US brokerage company, predicts that financial tech startups valued at $1bn could be the worst hit by a shock to the global economy.

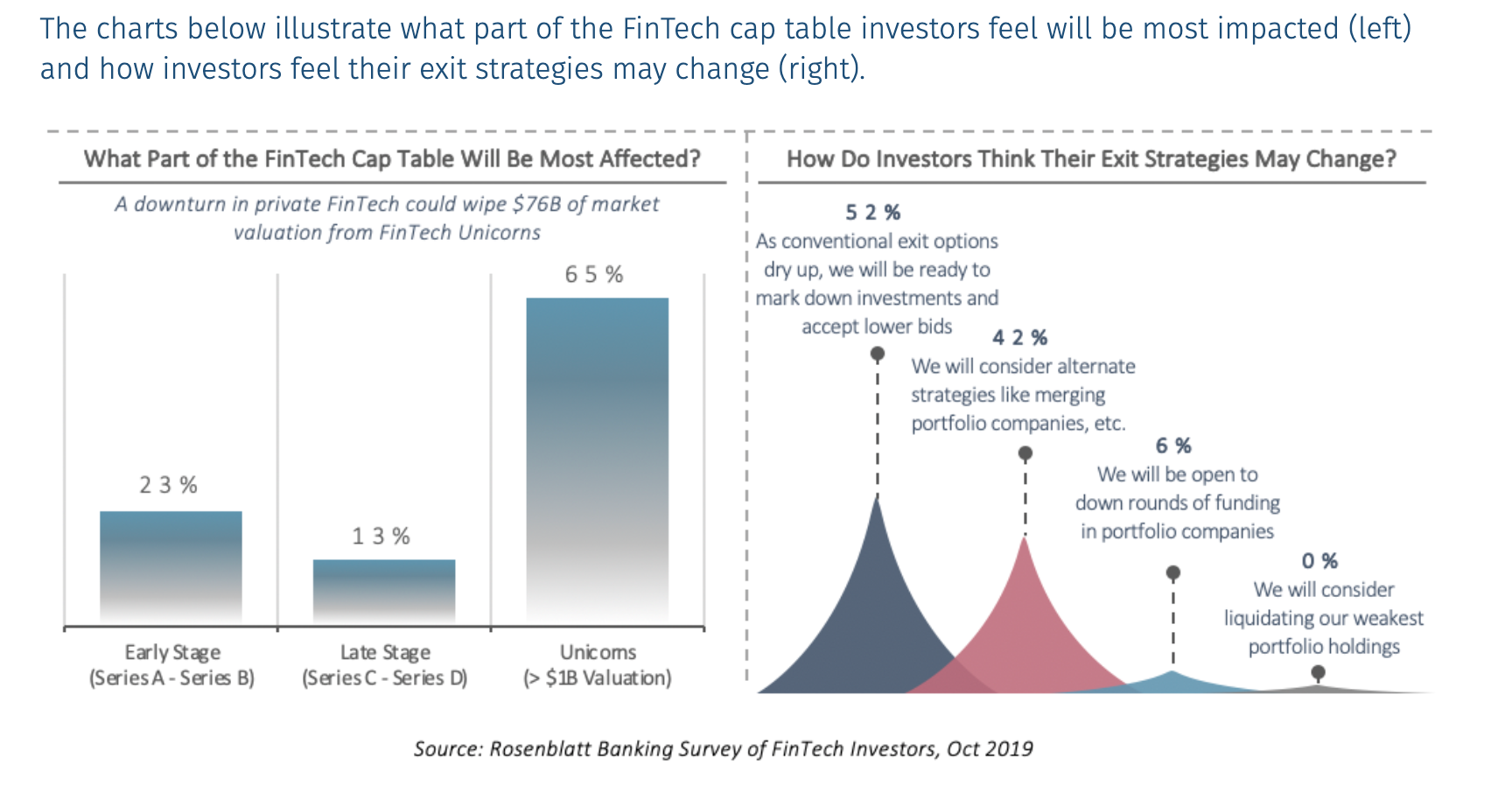

The report — inspired by a survey of fintech investors — estimates the world’s 58 fintech unicorns could each contract by 15% on average in the event of an extended recession; amounting to a $76bn drop in their combined market value (see * for full methodology).

The projection points to a bigger question in the private markets of startups: how will valuations be impacted by the economic turmoil prompted by the virus?

Already multiple reports suggest smaller startups, who are short of cash, are being forced to halve valuations to raise the money needed to meet payroll in the coming months.

But fintech unicorns are especially at risk of a write-down, the Rosenblatt report argues, noting the billion-dollar valuations are based on a series of (often optimistic) assumptions about future growth, profits and exit prospects, which are now in question.

“The bump up we have seen [in fintech valuations] between funding rounds may flatten out or even contract significantly in cases of down rounds,” the report explained, adding that squeezed investors are also likely to deploy less capital if the downtown continues.

This could mean that major fintechs — and the venture capital funds driving them — may have to radically adjust their expectations for raising fresh funds and for expansion.

Those currently rumoured to be raising include European unicorns like Monzo and Monese, while Revolut and Starling locked in their deals ahead of the market crash.

Run for the exit

Weaker exit prospects are a key factor for slashing startups valuations, but a dampened economy can also see poor exits actually materialise.

According to the findings in the Rosenblatt survey, the main threats to fintech unicorns now are cheap mergers or acquisitions, driven by opportunistic buyers looking to capitalise on the fintechs’ shortage of liquidity.

Fintech unicorns are also especially vulnerable here because of their notorious shortage of revenue, says Radboud Vlaar, partner at Finch Capital.

“Unicorns with negative unit economics and high cash burn will likely have to rethink and restructure. There’s a risk that the foundations of the hyper-growth unicorn story implode like a house of cards,” he told Sifted.

As such, the most aggressive fintech ‘unicorns’ (and those with the weakest revenue streams) could fare the worst in a recession if they haven’t yet secured funding. As such, investors expect business-to-consumer (B2C) companies like personal finance management apps to be worse affected.

Another risk is that if the coronavirus-fuelled slump continues, its economic bruising might be felt even in a distant initial public offering, again dampening unicorns’ exit prospects.

The revenue curse

Even without a full-blown recession, coronavirus could eat into the revenue of Europe’s fintech unicorns as follows:

Klarna — borrowers not paying back and even defaulting, potentially leading to continued losses

Tide — people not starting businesses so fewer customers

Monzo/ Starling — deposits and lending market fractured

Revolut — drop in international payments amid travel ban

Most large fintechs also rely on revenue from bank partnerships, which may be at risk as major institutions close the cash gates, primarily affecting business-to-business (B2B) fintech unicorns like Germany’s Deposit Solutions.

Additionally, investors fear fintech revenues may be under renewed threat from larger, older financial incumbents, who are better resourced to make a comeback in these extreme conditions.

“Traditional financial institutions will gain a competitive advantage over fintechs… as they are better capitalised, have bigger brands and benefit from customers becoming more risk-averse,” the Rosenblatt report noted.

Indeed, US trading app Robinhood has struggled to cope with significant volumes in recent weeks, proving its operational gaps.

Finally, the vulnerability of fintech startups can also be gauged from the sector’s performance in the public markets. This has historically been a useful indicator for private markets, which usually see a similar downturn around six months later.

The index of public US fintech companies crashed even more heavily than the S&P in the last few weeks, perhaps speaking to the sector’s lack of experience in weathering a downturn or that expectations have been bloated.

Specifically, Mastercard and PayPal have seen their share prices plummet by 35% and 24% respectively in the last month.

Combined, these data points help inform valuations in the private market, where investors ultimately judge businesses revenue potential based on future consumer spending or interest.

With fintechs’ revenue prospects currently in doubt across the spectrum — from payment processors to alternative lenders — the space’s famed boom certainly looks more fragile.

If the economic downturn continues through to the end of the year, it’ll be bad news for nearly everyone. But none more so than the fintech unicorns — now, an endangered species.

*Investors said they expected fintech unicorns globally to be most impacted by a recession, with valuations contracting by an average of ~15%. With a combined market capitalisation of $510bn at the time of the survey (Oct 2019), a protracted downturn could wipe off $76 bn of unicorn market value of the 58 fintech unicorns.

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: