![]()

![]()

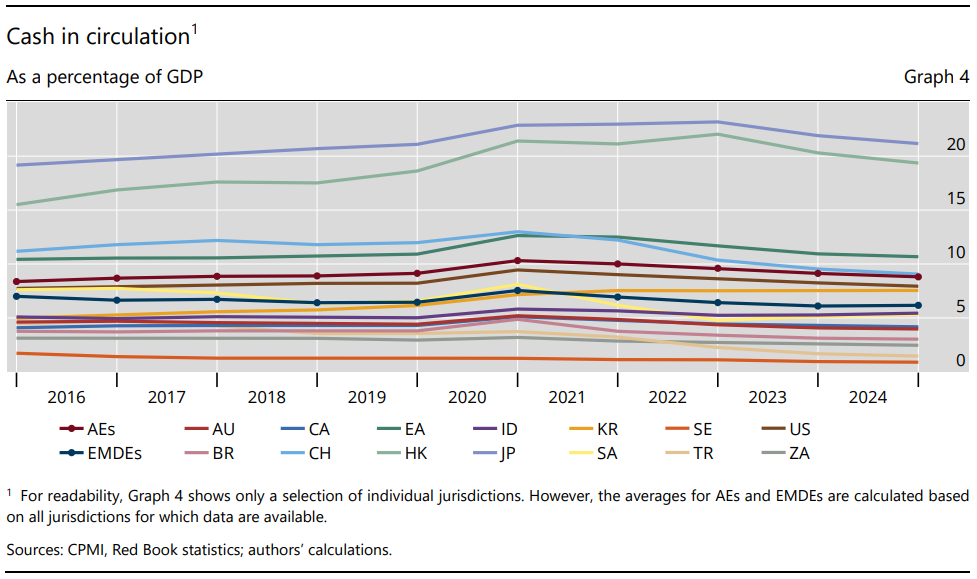

In 2024, cash in circulation as a percentage of GDP reached its lowest levels in Sweden (0.9%) and Turkey (1%).

New technologies, payment system enhancements and evolving user expectations are changing the way people pay. Cashless payments, such as card payments, electronic fund transfers and e-money payments, have been rising for years. In particular, the introduction of retail fast payment systems and increased demand for convenience and speed have spurred the use of fast payments. „Even so, it is impossible to imagine a world without cash, as it still plays a prominent role in people’s lives.” – according to the latest BIS – Committee on Payments and Market Infrastructures (CPMI) White Paper series called „Tap a card, pay by phone, but cash still holds its own”.

This CPMI Brief highlights key retail payment trends as observed in the 2024 Red Book statistics. These statistics were collected in the second half of 2025 from member jurisdictions of the Bank for International Settlements’ (BIS) Committee on Payments and Market Infrastructures (CPMI) and are publicly available at the BIS Data Portal. The Brief starts with an overview of the use of cashless payment methods and subsequently focuses on trends in fast payments. It then discusses global trends in cash in circulation and cash withdrawals. The Brief concludes with a summary of the key takeaways.

. The use of cashless payments continues to increase globally. Credit transfers are the fastest growing cashless payment method in emerging market and developing economies (EMDEs), while the growth in cashless payments in advanced economies (AEs) is mainly driven by growth in card payments.

. Fast payments are gaining ground and are a key driver behind the growth of credit transfers in EMDEs. Fast payments are increasingly used for small-value payments in both EMDEs and AEs.

. Cash withdrawals are declining. However, cash in circulation has largely stabilised, underscoring the enduring relevance of cash in economies.

Cash in circulation plateaued in many jurisdictions

In 2024, cash in circulation decreased slightly or stabilised in most CPMI jurisdictions. On average, cash in circulation as a percentage of GDP slightly declined to about 9% in AEs and remained near 6% in EMDEs (Graph 4). Differences across CPMI jurisdictions have remained large. Despite a further decline, cash in circulation was still highest in Japan (21%) and Hong Kong SAR (19%). It was lowest in Sweden (0.9%) and Türkiye (1%).

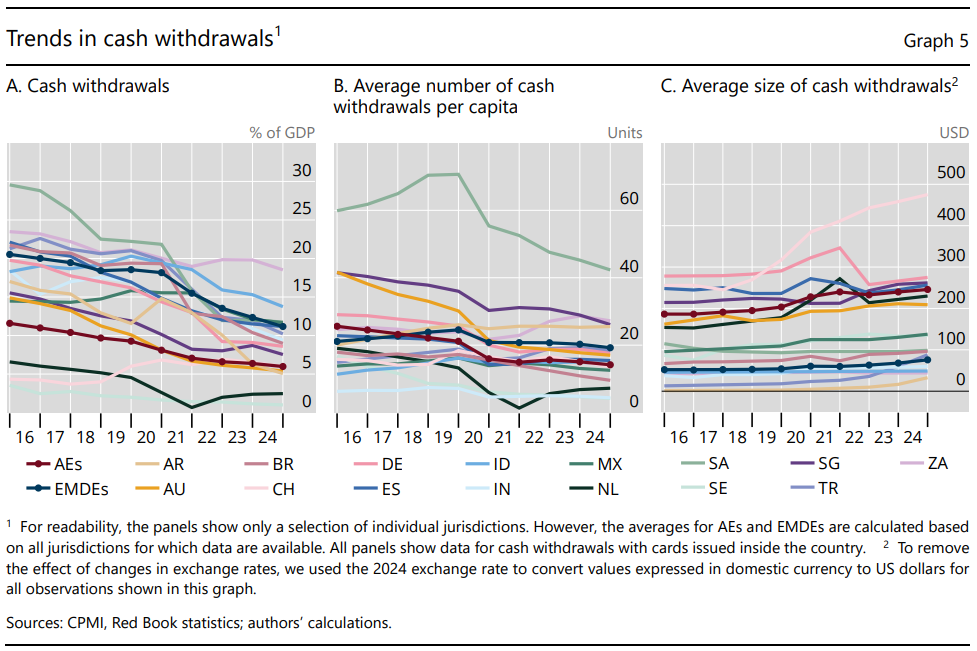

Since a large portion of outstanding cash in circulation is often used as a store of value, cash withdrawals are a better indicator of the use of cash as a means of payment than the total value of cash in circulation. While a short uptick and stabilisation were observed in a few jurisdictions during and immediately after the Covid-19 pandemic, cash withdrawals as a percentage of GDP declined again in most CPMI jurisdictions in 2024 (Graph 5.A). The value of cash withdrawals was generally lower in AEs (6%) than in EMDEs (11%).

However, there are large jurisdictional differences. It was lowest in Sweden (1%) and the Netherlands (2%) and highest in South Africa (19%) and Indonesia (14%). The number of cash withdrawals per capita also declined in most jurisdictions (Graph 5.B). Like the total value of cash withdrawals, the annual number of per capita withdrawals remained higher in EMDEs (19) than in AEs (14) and varied widely across jurisdictions. It ranged from four in Sweden and India to 42 in Saudi Arabia.

The decline in the number of cash withdrawals per capita generally went hand in hand with an ncrease in the average withdrawal value, suggesting that people withdrew cash less often but in larger amounts. At the aggregate level, the average withdrawal value in EMDEs increased from USD 51 in 2016 to USD 76 in 2024 (Graph 5.C). In AEs it grew from USD 186 to USD 246 over the same period.

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: