UK Finance analysis of nearly seven thousand authorised push payment1 (APP) scam cases shows that 70 per cent of scams originated on an online platform2 — highlighting the internet’s significant role in enabling fraud. The new analysis comes as the government published the draft Online Safety Bill this week, to include user-generated content on social media and dating apps but not all economic crime.

With the Covid-19 pandemic accelerating consumers’ shift online, fraudsters are adapting their tactics to exploit this societal change. In 20203, the banking and finance industry saw a jump in online-enabled push payment or bank transfer fraud with increases in investment (32 per cent), romance (38 per cent) and purchase scams (7 per cent).

Drilling down on findings from the new UK Finance dip sample4 shows that most investment (96 per cent), romance (96 per cent) and nearly all purchase5 (98 per cent) scams originated online. As it stands, the draft Online Safety Bill will tackle fraudulent investment schemes posted by users on social media – but will not tackle the same scam when digitally advertised or set up through a cloned website.

Impersonation scams, which have also grown significantly in recent months, were the only scams solely initiated via telephone calls and text messaging.

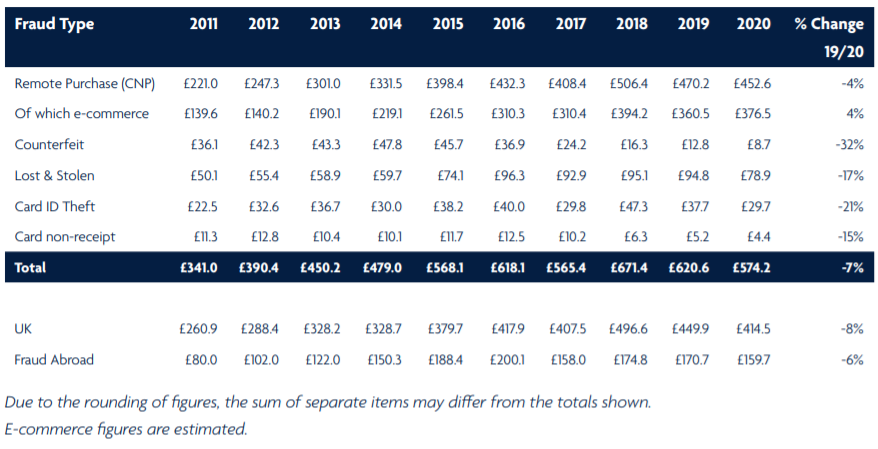

The money lost to APP scams totalled nearly half a billion (£479 million)6 in 2020, with proceeds often funding serious organised criminal activities, including terrorism, drug trafficking and child sexual exploitation: undermining the UK’s standing as a safe place to live and to do business.

Criminals expertly adapt scams to capitalise on the shift in consumer behaviour and vulnerabilities across digital platforms.

While this week’s news that user-generated content will be included in the upcoming Online Safety Bill is a welcome step, to effectively tackle all online scams and stop fraudsters capitalising from loopholes the Bill needs to include all economic crime for a holistic approach.

David Postings, Chief Executive at UK Finance, said:

„As more of us have shifted online because of the pandemic, we’ve seen a spike in money mule activity and investment and purchase scams because criminals can target people directly in their homes across online platforms. The banking and finance industry is continuing to tackle fraud on all fronts, but there is a limit to what we can do alone.”

“We were pleased to hear that the upcoming Online Safety Bill will tackle some aspects of fraud, but it won’t protect people from fraudsters’ online adverts and cloned websites. We encourage government to include all economic crime within the Bill when it is formally introduced. Not doing so leaves a large proportion of the public at high risk of being scammed online, because criminals are experts in adapting their tactics to exploit any loopholes.„

“I welcome the recent steps taken by some online platforms to work with us on tackling this issue. „

Recent successful cross-sector initiatives include the industry-sponsored Dedicated Card and Payment Crime Unit working with social media platforms to take down 700 accounts linked to fraudulent activity last year, of which over 250 were money mule recruiters.

____________

[1] An authorised push payment (APP) scam is where customers are tricked into authorising a payment to another account controlled by a criminal.

[2] UK Finance analysis of APP scam cases looked at where the scam first originated from (i.e. via an email or text message). It defined emails, social media, websites (including auction sites), and apps (including dating apps) as online platforms. For scams which were not enabled online, they were initiated in person or by a telephone call or text message.

[3] UK Finance Fraud the Facts 2021

[4] UK Finance dip sample:

UK Finance dip sample of nearly seven thousand authorised push payment scam cases

*The overall data has been weighted according to the proportion of each scam type in the total number of APP scams reported by UK Finance members in 2020. There was a total of 149,946 cases of APP scams in 2020 – further data is available in Fraud the Facts 2021.

Scam definitions

Impersonation scam: criminals contact victims purporting to be from a trusted organisation such as the police, or the victim’s bank to convince the victim to make a payment to an account they control.

Investment scam: criminals convince the victims to move their money to a fictitious fund or to pay for a fake investment.

Romance scam: criminals persuade victims to make a payment to a person they have met, often online through social media or dating websites, and with whom they believe they are in a relationship.

Purchase scam: criminals ask victims to pay in advance for goods or services that are never received.

Invoice or mandate scam: criminals convince victims, who are attempting to pay a legitimate payee, to redirect the payment to an account they control.

CEO fraud: criminals manage to impersonate the CEO or other high-ranking official of the victim’s organisation to convince the victim to make an urgent payment to the scammer’s account.

Advance fee scam: criminals convince victims to pay a fee which they claim would result in the release of a much larger payment or high value goods.

[5] In a purchase scam, the victim pays in advance for goods or services that are never received.

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: