Making digital currency interoperable

Visa is working on a ‘universal payment channel’ (UPC) that enables interoperability between different digital currencies such as CBDCs and private stablecoins.

article written by Catherine Gu, Global CBDC Product Lead, Visa

Imagine splitting the check with your friends, when everyone at the table is using a different type of money — some using a central bank digital currency (or CBDC) like Sweden’s eKrona, and others preferring a private stablecoin like USDC. How about sending $500 in USDC to a friend in London, and having those funds automatically converted to digital British pounds before they arrive in her CBDC wallet. Now imagine all this happening in real-time, across multiple networks, and compatible with multiple digital wallets.

In the not-too-distant future, this very well may be a reality. But getting there will take solving one key problem: cross-chain interoperability. In other words, how do you get different digital currencies, relying on different tech stacks and protocols, with different compliance standards and market requirements, to “talk” to each other in a wider network of value?

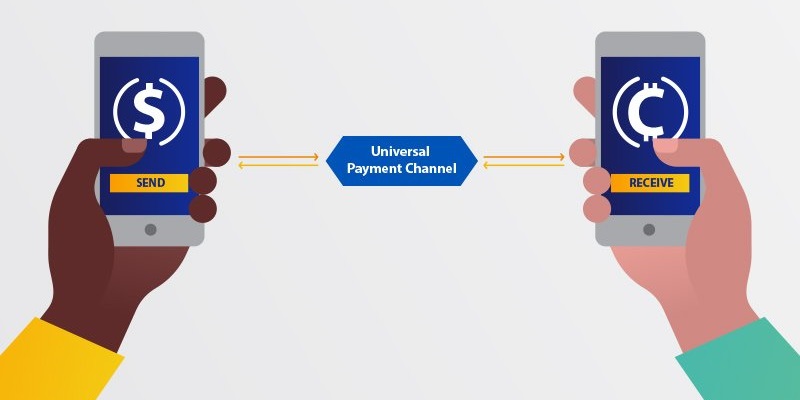

Visa’s research and product teams have developed a new concept to move the conversation forward. We’re calling it a “Universal Payment Channel” (UPC) and it acts like a hub, interconnecting multiple blockchain networks and allowing for secure transfer of digital currencies. Think of it as a “universal adapter” among blockchains, allowing central banks, businesses, and consumers to seamlessly exchange value, no matter the form factor of the currency.

We’re excited to share the mechanics of UPC in our research paper, as well as policy guidance for central banks and regulators on the implication of this research from the Visa Economic Empowerment Institute.

Why cross-chain interoperability matters for CBDC

Before we dive into the specifics, let’s address a burning question: if many of us are already splitting checks and tipping for services with existing financial tools and traditional currencies, why might we need a Universal Payment Channel?

While digital currencies may not be a part of your daily financial life today, it’s likely that they will play an important role in the future. Over the past two years, central banks around the world have shown an increasing interest in exploring CBDC — a new, digital form of central bank money that can be used directly by consumers, merchants, and financial institutions.

In the coming years, many central banks will likely implement some form of a digital ledger. Central banks will select the tech stacks and design protocols that make the most sense for their constituents, taking factors like governance, market requirements, technology providers, compliance standards, and nation-specific priorities into consideration.

As the number of digital currency networks increases — each with unique design characteristics — the likelihood that consumers, businesses, and merchants are transacting on the same network and utilizing the same type of money decreases.

We believe that for CBDCs to be successful, they must have two essential ingredients: a great consumer experience and widespread merchant acceptance. It means the ability to make and receive payments, regardless of currency, channel, or form factor. And that’s where Visa’s UPC concept comes in.

A network of blockchain networks

The story of UPC begins in 2018. The Visa Research team — a group of scientists and engineers focused on emerging technologies —began developing a framework for interoperability that would work across different blockchain networks and be independent of the underlying blockchain mechanisms.

The UPC hub concept that emerged would connect different blockchain networks by establishing dedicated payment channels between them — whether that means connecting CBDC networks between countries or connecting CBDC networks with vetted private stablecoin networks. New, trusted blockchains could easily be added to the network of networks by creating new payment channels within the UPC hub.

More than advance a vision for interoperability, UPC also has implications for transaction speeds in digital currencies. Where today’s modern payment networks can handle tens of thousands of transactions per second, some of the largest existing blockchain networks can currently handle only a fraction of those volumes. UPC’s specialized payment channels would be established off the blockchain and leverage smart contracts to communicate back with the various blockchain networks, delivering high transaction throughput securely and reliably and improving speeds overall.

While UPC would exist in the background for most users, it would deliver the kind of cross-chain interoperability that makes CBDC useful and attractive for consumers and businesses globally.

A network working for everyone

Ultimately, the UPC solution aims to serve as a network of blockchain networks — adding value to multiple forms of money movement, whether they originate on the Visa network, or beyond.

We’re excited to share this concept with the global community of researchers, builders and policy makers exploring new frontiers in money movement. As we continue our applied research, we’re working to translate our ideas into actual lines of code — check out a sample of our basic smart contract for UPC here.

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: