![]()

![]()

Why the next frontier in payments has no human in it. What it is, why it works now, and whether it’s where the next payment companies get built – an article by Dwayne Gefferie.

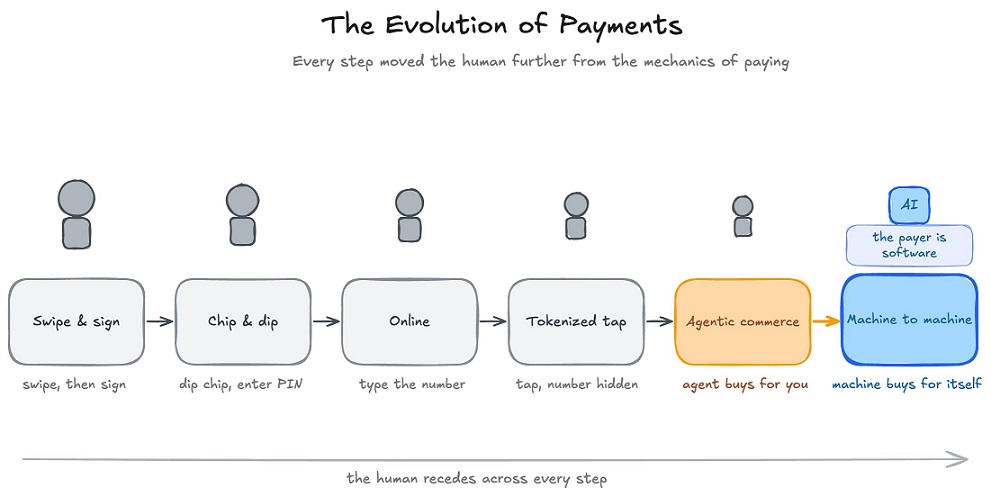

Every leap in payments has done the same thing. It has moved the human further from the mechanics of paying. We swiped and signed. Then we dipped a chip, and the card’s secret moved into the silicon. Then we typed the number into a browser. Then we stopped typing it at all.

Apple Pay, Google Pay, a tap, done. Visa has provisioned more than 12.6 billion network tokens. Most people who use them never learn that the real card number stays with the bank.

Each step abstracted the human from the credential. A person still decided, and a person still paid.

Then came agentic commerce, the story of the past year. An AI agent acts on a person’s behalf, sometimes only suggesting a purchase, sometimes preparing it and waiting for a click, and increasingly completing the buy on its own inside limits the person set once. (If you need a refresher on which protocols exist, check out “Payments Protocols”).

Agentic commerce still points one direction, though. An agent buying from a merchant, for a human, mostly on the card rails.

There’s one step past that. The machine stops shopping for a person and starts buying for itself.

That’s machine-to-machine payments. The payer is software, the payee is software, and the thing changing hands is usually a service the machine needs to do its own job. Compute, a model call, data, an API.

This isn’t theoretical. In the first half of 2026, Coinbase, Stripe, Google, Visa, Mastercard and AWS all shipped agent-payment products. In May, AWS wired agent payments into Bedrock’s AgentCore in preview, built with Coinbase and Stripe, letting software discover a service, agree a price, pay, and move on inside a single loop, settling in a fraction of a second with no human approval.

Two of those launches are the clearest lens on where this goes. Coinbase built a rail for machine payments, called x402. And in June 2026, Mastercard built a product for them, called Agent Pay for Machines. Most of this piece breaks down those two.

What follows is what machine-to-machine payments are, why they work now when they never did before, and the question that matters most. Is this a frontier where new payment companies get built? Or is it early crypto again, interesting to specialists and no one else for a few more years?

Let’s dive in.

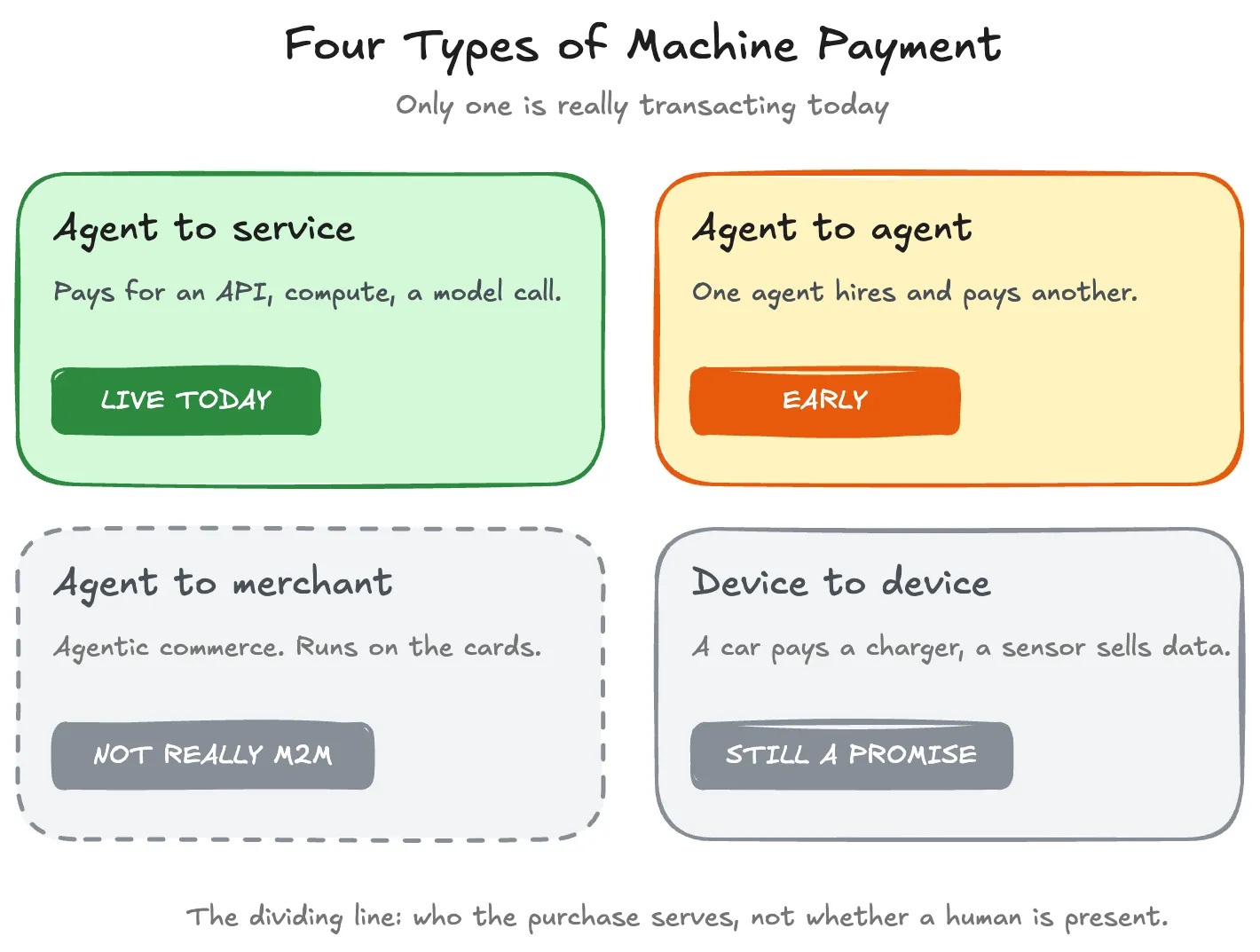

Two terms get used as if they’re one. They aren’t.

Agentic commerce is an agent transacting on behalf of a person. It runs across three modes. Discovery, where the agent finds and recommends. Human in the loop, where it prepares the purchase and waits for approval. Fully autonomous, where it completes the buy within the guardrails the person sets in advance. All three are agentic commerce, and all end with a merchant buying something for a human, mostly on cards.

Machine-to-machine moves the buyer. Here the software is the customer. It pays for what it needs to finish its own work, and it pays other software, not a store. Compute, an API call, a dataset, or a task handed to another agent.

Autonomy isn’t the dividing line, which is where the terms get muddled. A fully autonomous agent buying someone a pair of headphones is still agentic commerce. The same agent buying the compute it runs on is machine-to-machine. The question is who the purchase serves and what’s being bought.

There are four kinds of machine payment, and only one is really live.

Agent-to-service is an agent paying for an API, a model call, or a slice of compute. That’s the one transacting today. Agent-to-agent, one agent hiring and paying another, is real but mostly experiments. Agent-to-merchant is agentic commerce again, running on cards. Device-to-device, for example a car paying for a charger or a sensor selling its data, is still mostly a promise in 2026.

So “machine-to-machine payments are exploding” means one narrower thing. Agents are paying for software services, in small amounts, very often.

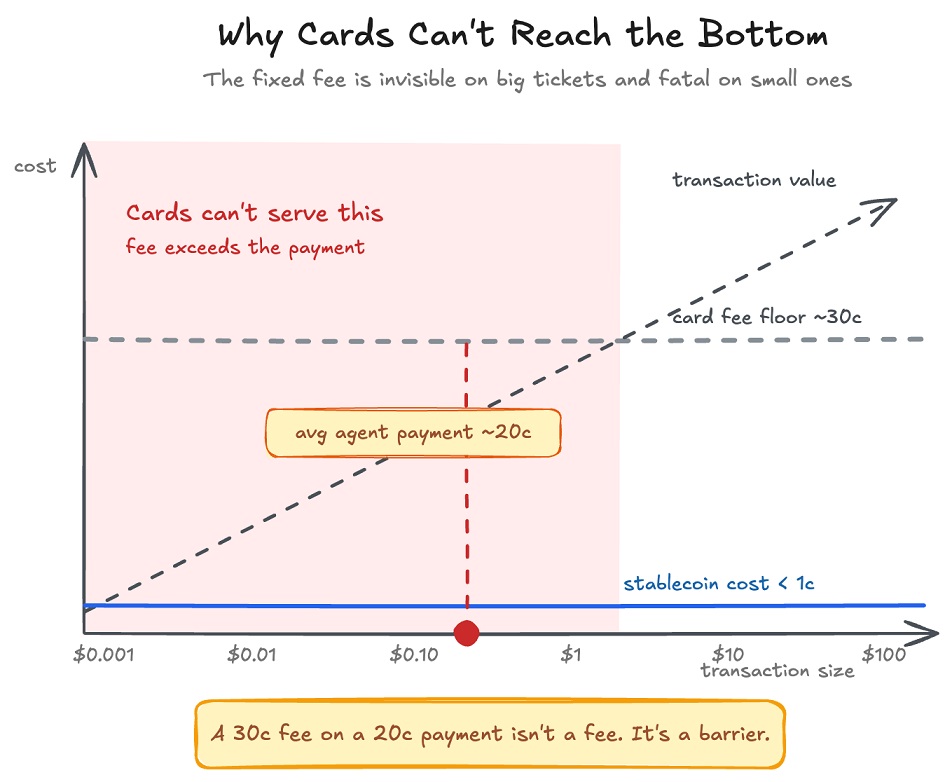

The honest number is worth stating plainly. On rails like x402, agents have run well over 100 million transactions and tens of millions of dollars in volume since 2025, at an average ticket near 20 cents.

That figure needs a caveat. A large share of it is test traffic and meme-coin activity, not commerce anyone would recognize. The plumbing is real and shipping fast. The genuine demand is still small.

Both are true at once. A transaction count quoted without that caveat is a headline, not an analysis.

So why would we care?

Small today doesn’t mean small forever. Tokenization started small too, now more than half of all transactions are tokenized either via a wallet or network tokens.

The mechanical reason a new rail exists at all comes down to a fixed cost.

A card transaction incurs roughly 30 cents in fixed costs before any percentage is added. That’s invisible on a 90-dollar pair of shoes. It’s fatal on a 20-cent API call.

A fixed 30-cent fee on a 20-cent purchase isn’t a fee. It’s a barrier. Most machine payments live below it.

When an agent calls a model a thousand times a minute, each call costing a fraction of a cent, card economics don’t survive the contact.

Cost is only half of it. The rest of the card stack assumes a person is present.

No one taps a phone, approves a push, clears a 3DS check, or squints at a CAPTCHA. Those steps exist to prove a human authorized the payment. Remove the human, and they lose their meaning.

A machine can’t prove it isn’t a robot. It is one.

The theme is familiar from these breakdowns. Payments got cheaper; complexity did not. The card rails are built around one assumption: a person at checkout decides to buy, and machine payments break that assumption at its root.

That break is the opening. It’s why there’s room, for the first time in years, to build something new underneath.

Follow the link to see the article in full

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: