Gold’s rally: mapping central banks’ demand for the precious metal in 2026

A survey published by the World Gold Council found that central banks remain highly bullish on gold, with a record 45% of reserve managers expecting to increase their gold holdings over the next 12 months. This follows a period of unprecedented accumulation, as central banks added an average of 1,000 tonnes of gold annually over the past four years, double the average of 500 tonnes per year recorded during the preceding decade.

an analysis by Paul Hoffman, data analyst at investing research platform BestBrokers

Gold had already been on a strong run in 2025, when it repeatedly set new records and its price ultimately surged 64% over the year – its largest annual gain since 1979. Momentum carried into early 2026, when gold climbed above $5,100, driven by safe-haven demand amid geopolitical tensions, expectations of looser U.S. monetary policy, strong central bank purchases (including China’s continued buying streak), and record inflows into exchange-traded funds.

Central banks were particularly active in 2025: several countries, including Poland, Kazakhstan, Brazil, and China, expanded their gold holdings as part of broader strategies to strengthen financial stability. While some nations increased reserves to hedge against geopolitical tensions and currency volatility, others, such as Singapore and Uzbekistan, reduced holdings to rebalance portfolios and manage liquidity. These movements highlight gold’s continuing role as a strategic and highly valued component of national reserves.

As of June 2026, gold has remained a focal point of global financial markets, even as prices have oscillated in response to shifts in monetary policy expectations and dollar strength. In view of this, the BestBrokers team undertook a comprehensive analysis of central bank demand for gold throughout 2025 and into the early months of 2026. Drawing on the latest World Gold Council data, we identified which countries expanded their official gold holdings most markedly and which reduced them, offering a detailed view of how sovereign reserve strategies have evolved alongside broader macroeconomic and market developments.

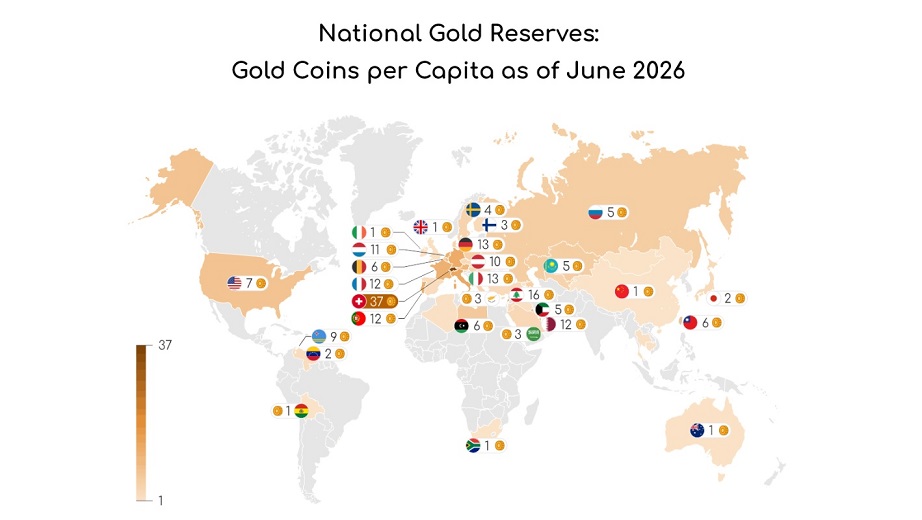

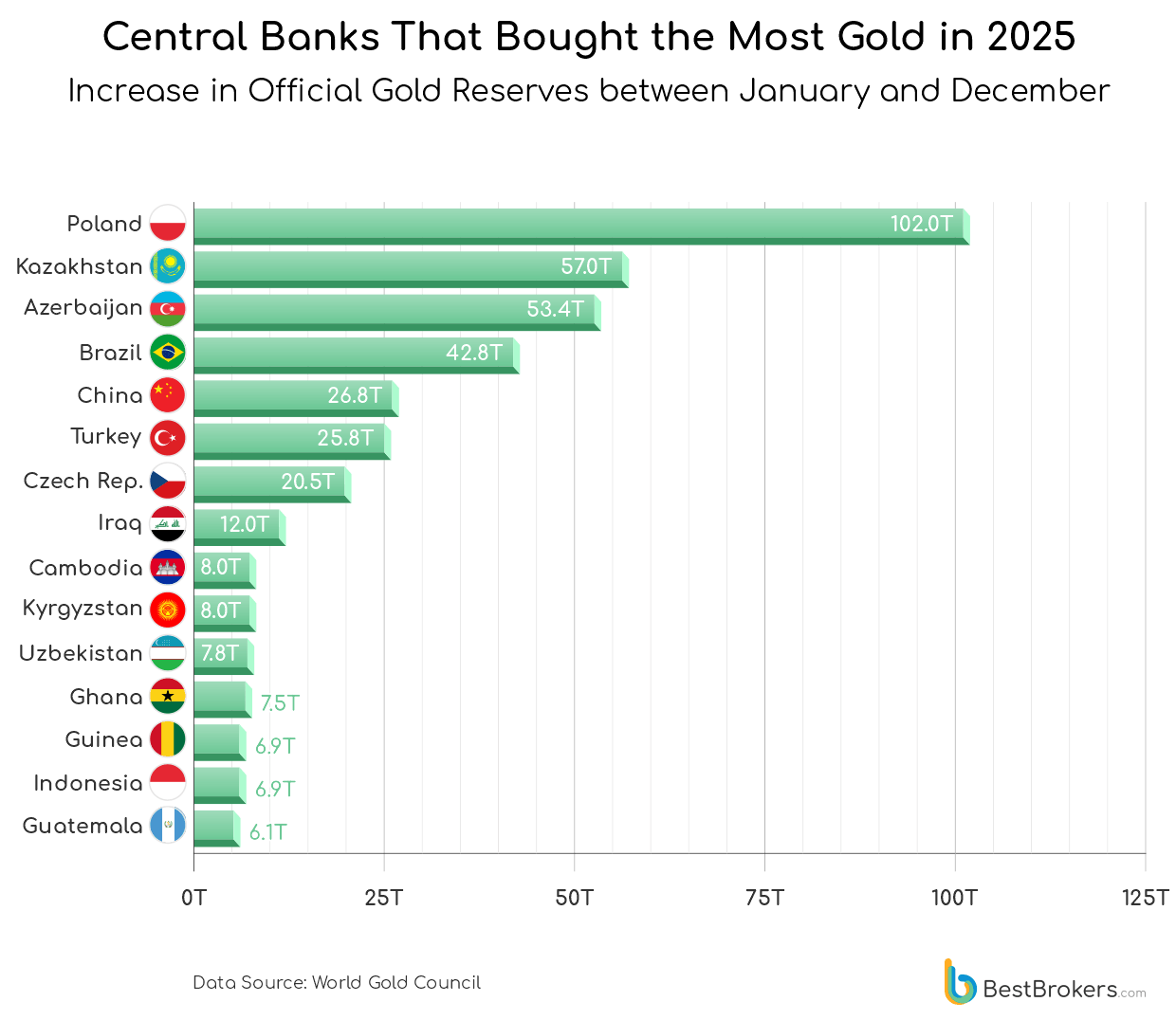

Countries That Expand Their Gold Reserves

In 2025, several countries continued to bolster their gold reserves, with Poland at the forefront, adding 102 tonnes, a 14% increase over the 89.5 tonnes acquired the previous year. The National Bank of Poland’s approach remains guided by persistent geopolitical uncertainty, particularly the enduring fallout from Russia’s war in Ukraine, which has kept security considerations paramount. Record-high gold prices did little to temper accumulation, as evidenced by 34.9 tonnes purchased in the final quarter following a brief period of relative stagnation. As of April 2026, Poland’s holdings stand at 550.215 tonnes, accounting for roughly 30.1% of its total reserves and securing the country’s position as the 12th-largest official gold holder in the world.As of June 2026, Poland’s holdings stand at 595.647 tonnes, accounting for roughly 29.70% of its total reserves and securing the country’s position as the 11th-largest official gold holder in the world.

Kazakhstan, Brazil, and China also expanded their gold reserves last year. Kazakhstan added 57 tonnes, a notable reversal after net sales of 10.2 tonnes in 2024, signalling a renewed strategic commitment to gold as a core reserve asset. Brazil remained largely inactive for most of the year, only to re-enter the market decisively with substantial acquisitions in September, October, and November, totalling 42.8 tonnes. Meanwhile, China continued its methodical accumulation, adding 26.8 tonnes on top of the 44.2 tonnes purchased in 2024, bringing its official holdings to over 2,307 tonnes and solidifying its position as the world’s sixth-largest gold holder.

After a substantial 77.4-tonne increase in 2024, Turkey continued to build its reserves, adding 25.8 tonnes. The pace, however, has moderated compared with its more aggressive accumulation in 2022 (147.6 tonnes) and follows a modest reduction in 2023 (-1.6 tonnes). Beyond the major players, other notable buyers in 2025 included the Czech Republic, Iraq, the Kyrgyz Republic, Cambodia, and Uzbekistan, each adding roughly 8 tonnes or more and securing a place among the year’s top ten gold purchasers.

Guinea, Indonesia, Guatemala, India, Serbia, Egypt, and several other countries also added to their gold reserves in 2025, with purchases ranging between 2.5 and 7 tonnes. Meanwhile, Bulgaria re-entered the market for the first time in several years, acquiring 2.05 tonnes ahead of its planned adoption of the euro in 2026. The purchase was linked to the country’s preparations for euro-area accession, which requires the Bulgarian National Bank to transfer part of its reserve assets, including gold and foreign currency, to the European Central Bank.

The State Oil Fund of the Republic of Azerbaijan (SOFAZ) boosted its gold holdings by 53.4 tonnes in 2025, making it the third-largest addition of the year after Poland and Kazakhstan. Unlike the central bank, which does not report any gold reserves and therefore is not included in official rankings of net buyers, SOFAZ manages the country’s oil and gas revenues and has treated gold as a strategic portfolio asset since 2012. Since then, the fund has continued building its position, accumulating roughly 200 tonnes of gold by March 2026, before reducing its holdings by 21.9 tonnes.

What Has Been Driving Gold’s Rally?

Gold’s historic rally throughout 2025 and into early 2026 has been fuelled by a potent combination of investment demand, central bank buying, geopolitical risk, and macroeconomic dynamics. According to the World Gold Council, gold prices set more than 50 all‑time highs in 2025 as global sentiment shifted toward safe‑haven assets amid geopolitical and trade tensions, while investment demand alone surged by roughly 84% year‑on‑year, driven largely by record inflows into gold‑backed ETFs and elevated bar and coin purchases. ETF holdings climbed to their highest level on record, with global AUM doubling to historic peaks, underscoring how investor flows have amplified price momentum.

Official sector buying also remained substantial: central banks collectively purchased well above long‑term averages throughout 2025, adding signals of structural reserve diversification that helped absorb supply and lend underlying support to prices. Even as real yields and U.S. Treasury rates fluctuated, the weakening U.S. dollar, influenced by expectations of Federal Reserve rate cuts and shifting trade policy dynamics, lowered the opportunity cost of holding non‑yielding gold, broadening international demand.

As of mid-2026, gold is no longer in a straight-line rally. After reaching record highs earlier in the year, prices have experienced a significant correction as stronger U.S. dollar performance and shifting expectations for Federal Reserve policy prompted some investors to take profits. At the same time, structural drivers remain largely intact. Central bank reserve diversification continues to provide long-term support, while concerns over government debt levels, inflation risks, geopolitical uncertainty, and the broader outlook for major currencies continue to sustain demand for safe-haven assets.

Although global gold ETF inflows have slowed markedly compared with the surge seen in late 2025 and early 2026, holdings remain near record levels and year-to-date flows are still positive, suggesting investors have largely moved to the sidelines rather than abandoned the metal altogether. As a result, many analysts continue to view the recent pullback as a consolidation within a longer-term bull market rather than a fundamental reversal of the factors that drove gold’s historic rise.

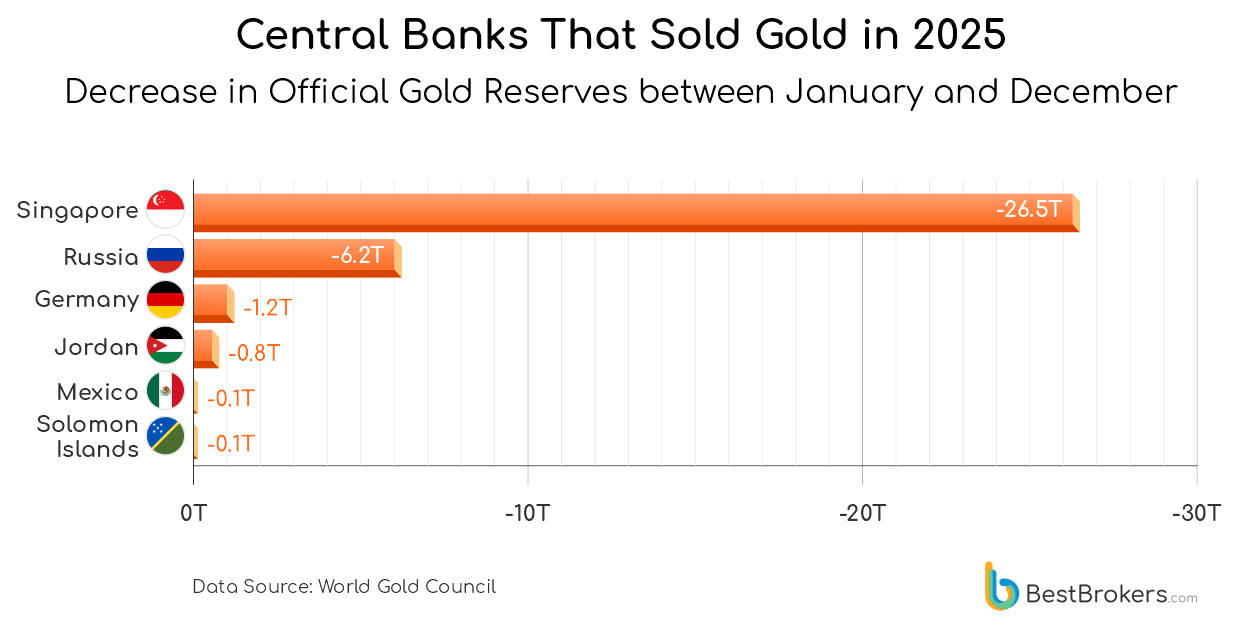

Countries Where Gold Reserves Dropped

In an unexpected trend, several central banks reduced their gold reserves in 2025, with Singapore at the forefront. Data indicates that multiple countries opted to sell portions of their holdings, likely in response to economic pressures, portfolio rebalancing, or to maintain liquidity in volatile markets. Another factor driving these sales was the historically strong gold rally: after prices surged sharply in 2025, some central banks took advantage of elevated valuations to realise gains, adjusting their reserve strategies while maintaining exposure to the precious metal.

Singapore consistently pared back its gold reserves throughout 2025, beginning in March with a sale of 4.85 tonnes and bringing total disposals for the year to 26.5 tonnes. This marks a clear reversal from its earlier accumulation strategy: after decades of relative inactivity, the country acquired 26.3 tonnes in 2021 and 76.3 tonnes in 2023, before initiating modest sales of 10.1 tonnes in 2024. The 2025 reductions reflect a deliberate portfolio adjustment, likely aimed at capitalising on elevated gold prices while maintaining a balanced reserve composition.

Despite these official sales, the city-state has emerged as a major hub for private gold storage, attracting the ultra-wealthy seeking a safe jurisdiction amid global economic and geopolitical uncertainty. Facilities such as The Reserve have seen soaring demand, with orders to store physical gold and silver increasing sharply in early 2025, reflecting Singapore’s reputation as the ‘Geneva of the East’ and a preferred destination for investors seeking secure, non-bank storage.

Russia reduced its gold holdings by 6.22 tonnes in 2025, ending a long period of accumulation that had seen 17 consecutive years of purchases until 2023, followed by two years of stable reserves. The country’s official gold stock now stands at 2,298.53 tonnes, representing 47% of its total reserves and securing its position as the world’s fifth-largest official gold holder.

Germany holds one of the world’s largest gold reserves, second only to the United States. In 2025, it reduced this amount by 1.28 tonnes, bringing its total holdings to 3,350.25 tonnes. The country has been drawing from its gold reserves consistently for decades; WGC data show Germany has lowered its holdings every year since at least 2002 (the latest available data), often through regular exports to the UK. 2024’s sale of 1.1 tonnes was the smallest annual reduction on record.

Other countries that reduced their gold reserves in 2025 include Jordan, Mexico, and the Solomon Islands, although their net sales remained modest, each under a tonne. After four consecutive years of accumulation, Jordan pared back its holdings by 800 kilograms. Mexico sold 100 kilograms in April, while the Solomon Islands both bought and sold gold throughout the year, ultimately closing 2025 with a net reduction of 100 kilograms, as well.

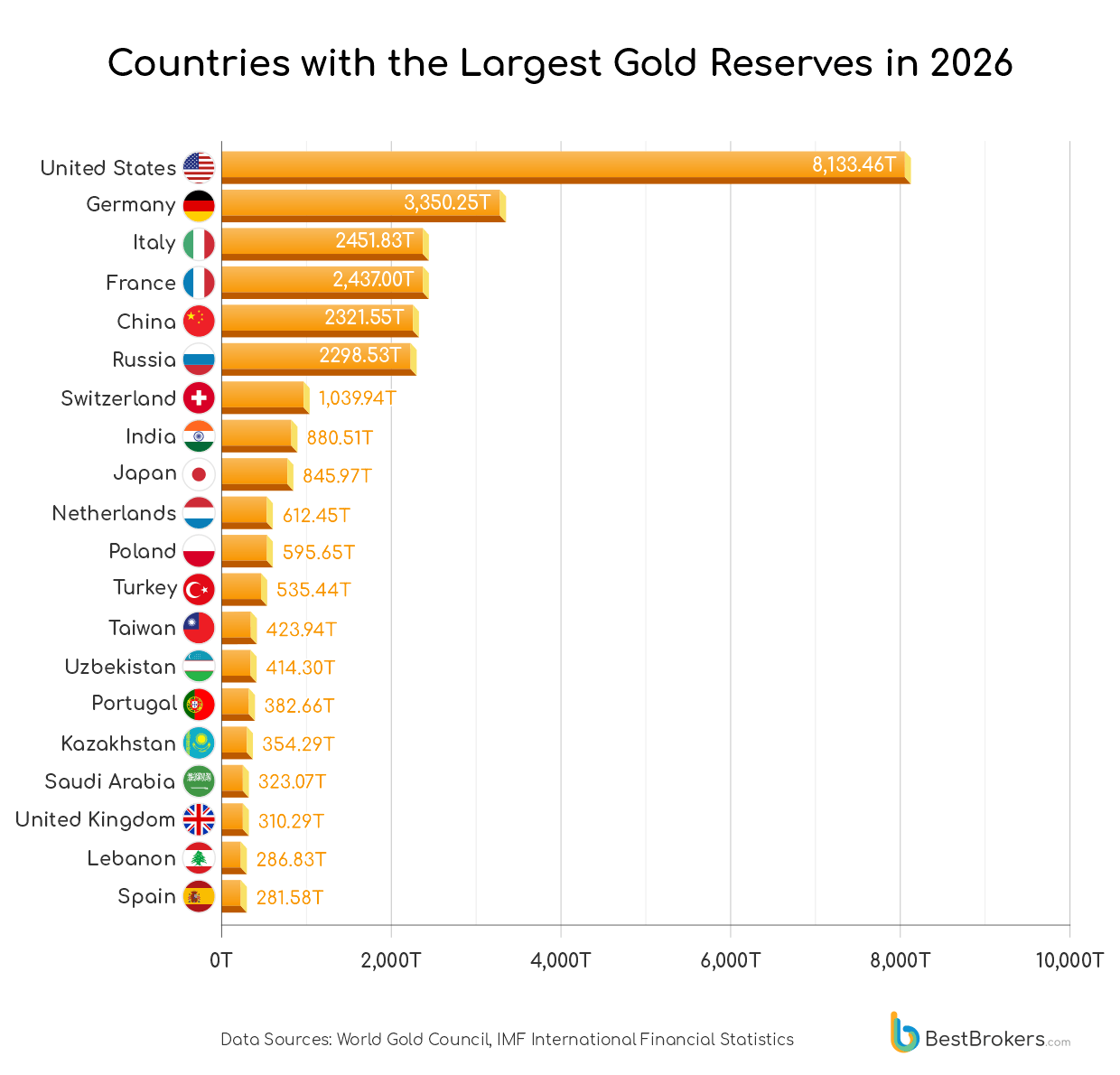

Central Banks with the Largest Gold Reserves in 2026

Gold has experienced one of its most volatile years on record. The story of 2026 can be divided into three phases: a historic surge in January, a broad correction from February through May, and a stabilisation attempt in June. Gold reached a record high of around $5,590 per ounce in late January, the highest level ever recorded. At that point, investor positioning had become extremely crowded, setting the stage for a reversal. The surprising aspect of 2026 is not that gold rose, it is that it fell despite several developments that would normally boost safe-haven demand, including geopolitical tensions and heightened uncertainty in global markets. Instead, concerns about persistent inflation, higher-for-longer interest rates, and a stronger U.S. dollar proved to be more influential drivers of price movements.

During June, gold showed signs of stabilising but remained highly sensitive to interest-rate expectations, inflation data, and developments in the Middle East. As a result, price movements were often driven more by shifts in monetary policy expectations than by geopolitical developments alone.

Gold’s importance, of course, extends beyond private investors, serving as a key reserve asset held by central banks to diversify holdings, support financial stability, and strengthen confidence in national currencies. The nation holding the largest official gold reserve remains the United States, with 8,133.46 tonnes, representing 83.30% of its total foreign reserves. Germany and Italy follow, with 3,350.25 tonnes and 2,451.83 tonnes, respectively. Other countries with substantial holdings include France (2,437 tonnes) and China (2,321.55 tonnes). Russia, Switzerland, India, Japan, and Turkey also maintain significant reserves, with Russia at 2,298.53 tonnes and Switzerland approaching 1,040 tonnes.

Although India, Japan, and the Netherlands each hold less than a thousand tonnes, together they account for roughly 6.4% of global official gold reserves. It should be noted that not all nations report their gold holdings to the IMF, so actual totals may vary. Collectively, the ten largest national reserves account for 66.7% of all gold held by official institutions, while the top five countries alone hold 51.14%.

Trends in 2026: Activity Slows But Broadens

Since the start of 2026, central bank gold activity has shifted away from the broad, synchronised accumulation phase that dominated 2022-2024 and into a more fragmented, two-way flow environment. Net purchases remain positive, but the pace is no longer uniform, with steady reserve diversification demand increasingly offset by intermittent, often liquidity-driven selling and balance sheet adjustments.

What has changed most is not the direction of flows, but their character: gold is being accumulated more selectively and managed more actively within reserves, rather than added consistently as a one-way strategic hedge. This has resulted in a market where underlying official-sector demand is still supportive, but less predictable and more sensitive to short-term financial and geopolitical conditions than in the previous cycle.

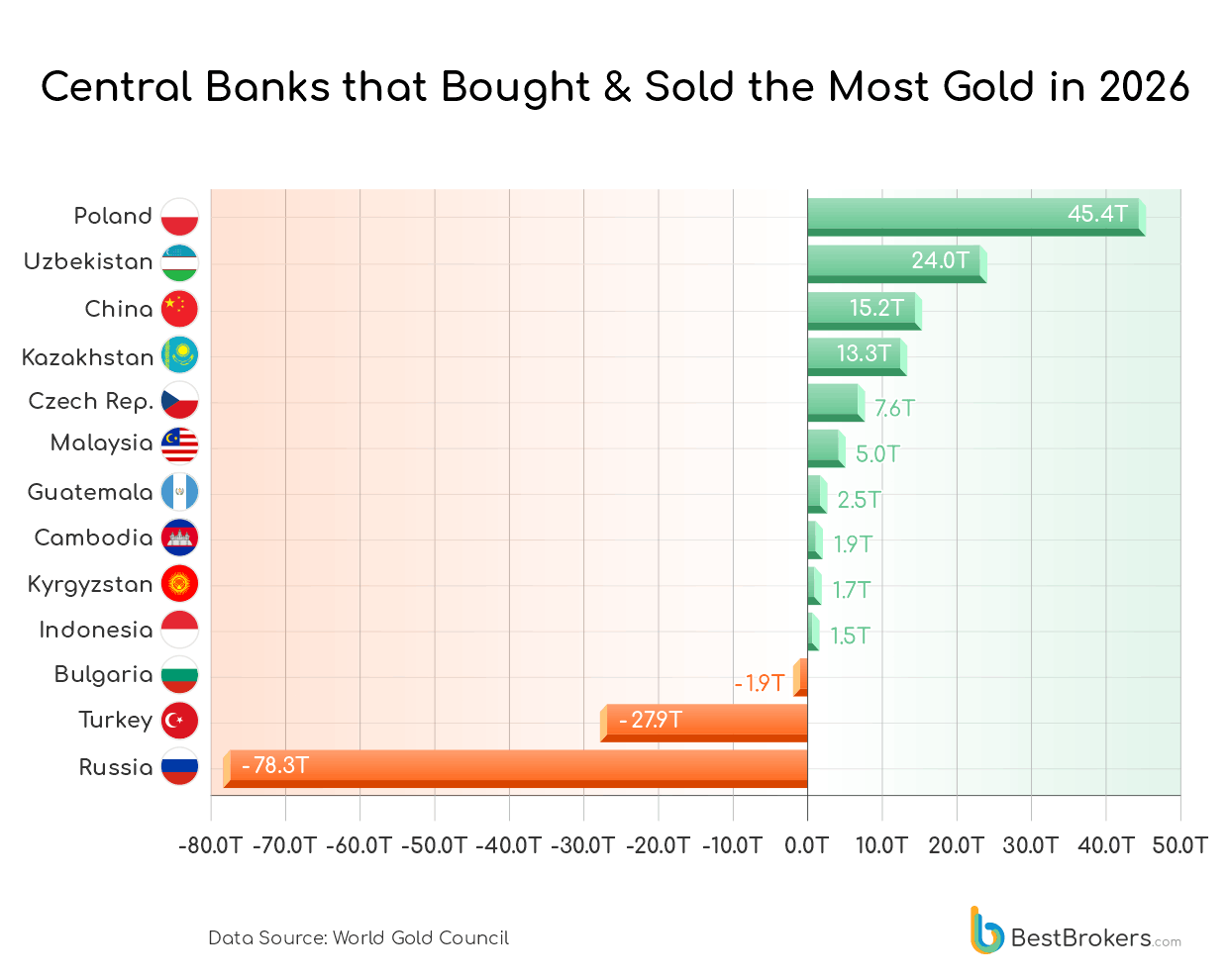

So far in 2026, Poland has continued to lead global central bank purchases, adding 20.2 tonnes in February alone, 11.2 more in March, and 14 tonnes in April, bringing the total to 45.4 and extending its rapid accumulation trend that has seen it build more than 360 tonnes since 2023. Uzbekistan follows closely with 24 tonnes, adding 25.2 in the first three months of the year, and then reducing by a little over a tonne in April, while China ranks third with a total of 15.2 tonnes, reflecting a continuation of its steady, rule-based accumulation strategy, with monthly additions extending its multi-year buying streak and reinforcing gold’s role as a gradual reserve diversifier rather than a cyclical trading asset.

Kazakhstan added 13.3 tonnes in 2026 so far, the Czech Republic also continued its steady accumulation at 7.6 tonnes, while Malaysia re-entered the market with 5 tonnes of combined purchases after an extended period of inactivity.

On the selling side, Turkey has emerged as the largest net seller, replacing Russia, by reducing its holdings by over 78 tonnes in the first three months of the year, marking a sharp reversal from its earlier net-buying stance and reflecting concentrated, large-scale disposals driven by liquidity needs, with gold being actively mobilised through both outright sales and swap operations to obtain foreign currency and stabilise the exchange rate under pressure.

Bank of the Republic of Türkiye (CBRT) has been rapidly selling gold reserves since the outbreak of conflict involving the U.S., Israel, and Iran, with the goal being to help cushion the Turkish economy and financial markets from increased volatility and mounting pressure on the Turkish lira, as investors sought safety amid heightened geopolitical uncertainty and capital outflow risks. Most of these transactions, however, have not been reported as official gold holdings but announced separately as bank operations aimed at liquidity management. If all gold trades and changes in the reserves were to be tracked, Turkey has reduced its gold holdings by more than 157.6 tonnes since January 2026.

Russia is now second with a total of 27.9 tonnes reduced in 2026, with changes primarily linked to domestic fiscal and liquidity management needs and the use of gold as a flexible buffer within a heavily constrained external financial environment. Overall, this split between broad-based accumulation and concentrated selling highlights a market still anchored in official-sector support, but increasingly shaped by tactical adjustments to price levels and domestic financial conditions.

A World Gold Council survey published on June 16 indicates that central banks are increasingly inclined to expand their gold holdings, with a record 45% of reserve managers expecting to raise their allocations over the next 12 months, up 2 percentage points year-on-year. The Bank of England remains the most commonly used vaulting location, cited by 57% of respondents, although reserve managers continue to diversify storage across multiple jurisdictions. Domestic vaulting ranks second at 49%, followed by the Bank for International Settlements at 16%, which has edged slightly higher compared with last year. In contrast, preference for the Swiss National Bank has declined notably, falling to 6% from 12% in 2025.

Who Does Not Own Any Gold?

Despite being one of the world’s top gold-mining nations, Canada is among the very few countries that hold no gold in their official reserves. The Bank of Canada fully sold off its bullion holdings over the past two decades and today reports 0 tonnes of gold as part of its international reserves. This decision reflects a longstanding policy view that U.S. Treasury securities and other highly liquid assets are better suited for reserve management than gold, which former deputy governor Timothy Lane once described as not fitting Canada’s ‘asset-matching framework’.

Norway is another notable example. During World War II, its central bank evacuated about 50 tonnes of gold to the United Kingdom and the United States to support the government-in-exile. After the war, parts of the hoard were returned, but in 2004, Norges Bank announced the sale of nearly all of its remaining bullion, keeping only seven bars and some coins for historical and exhibition purposes. Today, Norway officially reports 0 tonnes of gold in its reserves.

These cases stand in sharp contrast to most other advanced economies, where gold continues to represent a significant share of central bank reserves. They highlight that not all major economies consider the precious metal essential to reserve strategy, even countries with large mining industries like Canada or with historical stockpiles like Norway.

The article in full here

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: