Future of Banking: Neobanks Come Of Age – a report by S&P Global

S&P Global declares neobanks have „come of age,” yet most customers still won’t trust them with their paycheck. S&P looks at Revolut, Nubank, Klarna, N26, Monzo, and Starling Bank and likes what it sees. Solid business models, improved risk management, and no longer bleeding money the way they did between 2020 and 2022. That said, the biggest old problem remains: what S&P calls the „trust gap.” Neobanks still serve mostly as secondary accounts. Customers use them for travel and occasional transactions but keep their primary banking with incumbents.

„We think neobanks face a „trust gap”, largely due to reputational challenges and limited operational history. Many customers still view traditional banks as safer for complex financial services that require deeper relationships, such as mortgages, corporate and investment banking, and wealth management. In contrast, neobanks succeed in primarily transaction-driven services that do not require deep client relationships, such as payments, international transfers, deposit-taking and brokerage, and tailored small-to-midsize enterprise banking.” – according to the report.

From S&P Global Ratings: Digital-native neobanks are ready to shed their newcomer status and forge a new financial services landscape. In a diverse field, the most successful neobanks have proven their profitability and become serious competitors to incumbent banks.

The convergence of smartphones and e-commerce began to reshape customer expectations in the 2010s. Smartphone adoption transformed banking into an “always-online” experience, replacing costly, branch-based client interactions with intuitive, real-time mobile apps.

Simultaneously, the e-commerce boom drove the demand for fast, frictionless digital payments. Consumer preference shifted toward convenience and transparency, exposing the limitations of traditional banks. With their mobile-first, low-cost, app-based models, neobanks and adjacent fintech offerings began to flourish.

Key Takeaways

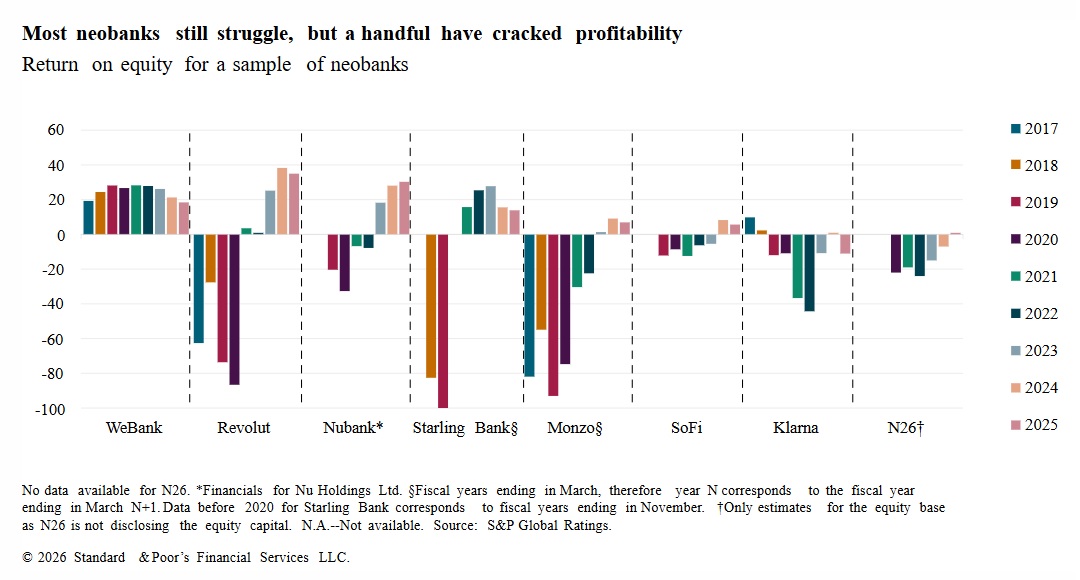

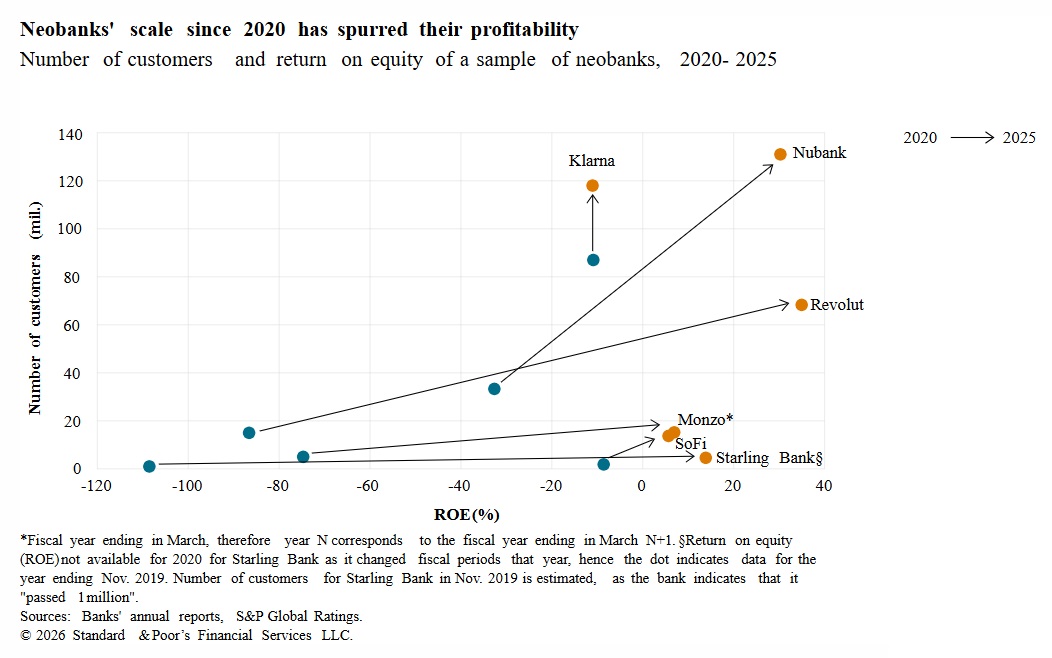

. Long-term success for neobanks depends on achieving the scale and maturity required to generate sustainable earnings and meet shareholder expectations.

. Neobanks are a diverse cohort, but the most successful have now “come of age”, demonstrating sustainable business models, proven risk-management effectiveness, and the ability to reshape market practices.

. Meanwhile, incumbent European banks have made significant digitalization gains, and are now using emerging technology such as AI to counter the competitive threat posed by neobanks and fintechs.

. To mitigate volatility and customer churn, neobanks are using all-in-one digital platforms and expanding into lending and wealth management to build stable, franchise-based services.

Neobanks Are Well-Positioned To Capitalize On Macro And Market Trends

We believe four trends are worth watching in the coming years. Neobanks are well-positioned to take advantage of these shifts, because their agility allows them to capture rapidly evolving markets where technological adoption often determines the winners and losers.

Trend 1: The upcoming large wealth transfer can bring more money to neobanks

Neobanks are maturing at the time as the post-war generation – with its substantial wealth of about $83 trillion at year-end 2024 (51%) – begins transferring assets. Over the next 20 to 25 years, about $74 trillion of these funds will be vertically transferred from that cohort (born 1946-1964) to the following generations, according to UBS’ 2025 Global Wealth Report.

About $36 trillion of these assets sit outside the U.S., Brazil, and China, the top-three nations where intergenerational wealth transfers will happen. In Europe, Germany, Italy, France, and the U.K. should see generational transfers of about $2 trillion, according to UBS, which is a substantial redistribution within the next two decades.

While traditional, incumbent banks and wealth managers manage most of those funds, we think some of this wealth could flow to neobanks’ savings and investment products for management or custody. However, this will require product extension, and could increase competition with neobrokers that similarly seek to extend their proposition toward banking and other investment services.

Trend 2: As neobanks mature, international expansion may increase diversification

Some neobanks are expanding beyond their domestic market, partly thanks to regulators’ openness toward innovation. In the EU, “passporting” rules allow them to operate cross-border without establishing local entities. N26, for example, operates digitally in 24 European countries using its German banking license and EU passporting, while Revolut serves customers across the European Economic Area with its licensed bank in Lithuania. It also received a U.K.-specific license in March 2026.

However, access is not seamless. Cross-border banks need access to local payment systems to process wage and tax payments, which can require local IBANs, requiring a local presence through branches. The U.K. being outside the EU adds further complication; for example, Monzo gained an Irish license in 2025 to maintain EU access.

Expanding as fully licensed institutions beyond Europe will likely prove more complex. The U.S., where Revolut recently applied for a bank charter after Nubank’s conditional approval in January 2026, will be the target for very few European neobanks, in our view. The size and wealth of the U.S. market is attractive, but Monzo’s decision in early 2026 to abandon transatlantic ambitions demonstrates the difficulties of achieving profitable scale.

Trend 3: Some neobanks are moving toward longer-term funding, making investor trust a vital requirement

Maturing business models and difficult funding conditions in 2022-2024 have prompted some neobanks to seek more stable, long-term capital. To support their evolution into full-scale banks, some neobanks are transitioning from venture capital toward debt capital markets, using bonds and securitizations. While this move offers more scalable funding, limited track records remain a potential barrier to market access.

Trend 4: Neobanks are deep in the generative AI innovation race

A 2025 World Economic Forum (WEF) survey found that 80% of fintechs, including neobanks, have implemented or plan to implement generative AI in customer service and process automation, while 30% plan to use it for risk management by 2027.

Leveraging generative AI for data analytics and advanced risk modeling can improve credit risk accuracy and fraud detection, and enhance asset quality, enabling profitable growth. Key use cases of AI-powered solutions at neobanks (and equally at banks) include:

. Pricing: Risk-based pricing for lending products (for example, unsecured loans and buy now, pay later) and deposit offerings;

. Customer experience: Personalized product offerings with high conversion rates; and

. Risk management: Origination (credit risk scoring), loan monitoring (early warning signals and predictability power), and collection (recovery models), along with better fraud detection for all products.

Some neobanks are deploying AI agents to increase productivity and efficiency, with applications such as automated language translation supporting international expansion plans, for example. However, it’s too early to draw conclusions, particularly on agentic AI, because the technology is rapidly evolving and models continue to improve.

Conclusions: neobanks push incumbents toward higher-quality digital banking

„In our view, neobanks have pushed traditional banks to innovate and upgrade digital offerings over the past decade. This competition has resulted in new financial products that provide cheaper and higher-quality access to financial services with 24/7 availability for everyone.

We believe neobanks lack a competitive advantage in traditional lending. Technology offers little differentiation. Neobanks lack the internal credit models of established banks, and in some European countries a human touch is often preferred when it comes to important decisions where reputation and tradition matter. Low-yielding mortgage business and neobanks’ typical high funding costs also hinder scale, with long-dated products that are capital-consumptive and dilute the return on invested equity.

Nevertheless, we think neobanks will continue to grow and challenge incumbents by disrupting traditional business models and trying to expand into core banking products such as mortgages. With increasing client trust, strong corporate governance, and smart business decisions, neobanks could experience substantial growth in the next five to 10 years and become mature in selected market segments.„

Read more: https://okt.to/O9Pb4s

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: