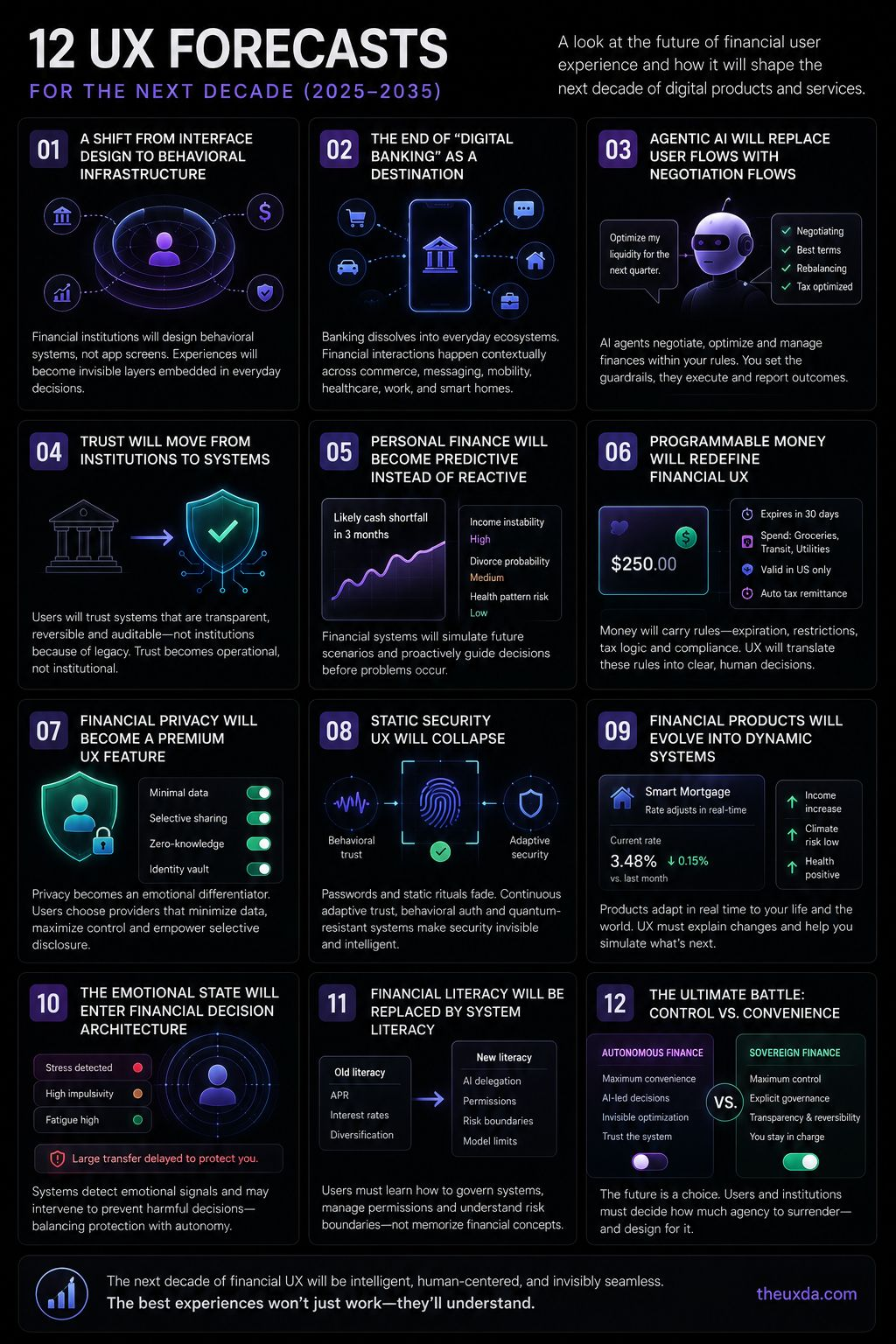

12 digital banking predictions for 2035

By 2035, customers may no longer judge digital banking only by how smoothly they move through screens. They will judge it by how well AI understands their financial life before they even open the app. This creates a new challenge for banks. If money starts moving on autopilot, UX can no longer be designed only around buttons, dashboards and journeys, it must be designed around trust, control, prediction and permission. Because the next banking interface may not be something customers use, it may be something they allow to act on their behalf.

an article by Alex Kreger, Founder and CEO UXDA Financial UX Agency

By 2035, financial UX will no longer revolve around designing apps, dashboards or onboarding flows. The industry is entering an era where financial experiences become autonomous, predictive, invisible and deeply integrated into human behavior.

This transition will force banks, Fintechs and regulators to rethink not only products—but the very relationship between humans and digital financial systems. Banking apps will not disappear by 2035. Their function will change. They will move from places where customers manually manage money and transactions to control and insights centers where customers manage the AI acting on their behalf — setting strategies, permissions, boundaries, trust levels and automation rules.

The Twelve Radical Shifts Coming to Digital Banking by 2035

Today, “customer-centricity,” journey orchestration and experience transformation have become strategic priorities across the global banking industry. But this shift is still only beginning. The next decade could change everything, including:

1. A Shift from Interface Design to Behavioral Infrastructure

By 2035, financial institutions will no longer design functional app screens. They will design behavioral systems in which apps will only play a small part.

Today’s financial UX is still rooted in a desktop-era assumption that customers intentionally use digital banking services. They open an app, complete a task and leave. By 2035, this assumption will be gone.

Traditional flows—onboarding, payments, savings, investments—will become invisible layers embedded into everyday decisions. The interface will nearly disappear. What remains is the behavioral architecture underneath.

UX implication: Financial UX becomes complex, distributed experience governance, not just app redesign. We will not focus on making the interface more usable. We’ll make the system’s recommendations more valuable, trustworthy and its behavioral interventions less intrusive.

2. The End of „Digital Banking” as a Destination

Mobile banking apps will lose their central role in routine activity, not because they will disappear, but because they will stop being where financial decisions happen.

Banking dissolves into commerce, messaging, mobility, healthcare, work platforms and smart homes. Financial interactions occur contextually—at the moment of decision, embedded in the environment where that decision lives.

By 2035, most users will no longer consciously “use” banking. Banking will simply happen around them.

What changes: financial UX transitions from „basic functions range” to „ecosystem experience governance.” Banks will no longer optimize onboarding and transaction flows. They will design how financial logic appears and disappears across dozens of integration touchpoints, providing users with an app interface that allows them to analyze performance, orchestrate AI execution and manage rules.

3. Agentic AI Will Replace User Flows with Negotiation Flows

Today, customers manually compare loans, cards and investments. By 2035, users will increasingly delegate financial decision-making to autonomous AI agents: „Optimize my liquidity for the next quarter while preserving tax efficiency. Here are my constraints.”

AI agents will automatically negotiate products, rebalance assets, optimize taxes and manage financial operations across institutions. It doesn’t ask the user’s permission for every micro-decision. It operates within boundaries users have set and reports outcomes.

UX challenge: The interface becomes less about data interactions and more about calibrating trust to AI. How do you help users understand what they’re delegating? How do you make transparency feel less burdensome than control?

4. Trust Will Move from Institutions to Systems

Historically, people trusted financial institutions. But by 2035, users may trust systems, protocols and AI agents more than the institutions themselves.

Trust will become operational, not institutional. People will trust institutions if their AI systems are transparent, reversible and auditable—not because their 100-year legacy fosters a feeling of customer safety. Banks with a legendary legacy but opaque UX systems will lose.

UX implication: Functional financial services alone will no longer create trust. The competitive advantage will move to transparency architecture. How clearly can we show what the system does? How easily can users understand and calibrate its recommendations? Transparency, controllability, explainability and reversibility will become core UX requirements.

5. Personal Finance Will Become Predictive Instead of Reactive

Today’s users typically manage finances or check balances after financial events occur. By 2035, financial systems will continuously simulate future scenarios before potential problems occur.

UX implication: Financial interfaces will turn into predictive dashboards, not account summaries. The value isn’t in historical accuracy; it’s in temporal foresight, and the competitive moat is predictive accuracy. A machine will be much better than a human at plotting possible future vectors based on historical data and correlations.

6. Programmable Money Will Redefine Financial UX

As programmable money, tokenized assets and CBDCs evolve, money itself may begin carrying embedded behavioral logic. Sooner or later money will gain rules. This is a UX crisis and opportunity.

The crisis – Users must suddenly understand not just how much money they have, but what their money is allowed to do, exploding cognitive complexity.

The opportunity – New experience layers create competitive differentiation:

. Visualization of money permissions that makes constraints visible without overwhelming the user

. Rule transparency that explains why this money has those conditions

. Spending eligibility indicators that prevent failed transactions before they happen

Financial UX becomes the language layer that translates programmable money into human decision-making.

7. Financial Privacy Will Become a Premium UX Feature

As AI systems and programmable finance increase traceability, privacy may become one of the most emotionally valuable financial features in 2035.

By 2035, users may actively choose financial providers based on data minimization, selective disclosure and zero-knowledge architectures. Privacy will stop being a regulatory checkbox and become a global product differentiator instead.

UX opportunity: Privacy will evolve from a technical infrastructure into emotional reassurance. The future competitive advantage may not be “more personalization” but controlled personalization with clear human boundaries. The question is, how does the financial interface of the future reassure customers that they are being seen less, not better?

8. Static Security UX Will Collapse

Quantum breakthroughs will make traditional cryptographic assumptions obsolete. This forces a fundamental shift from:

. Password-based mental models („set a strong password”)

. Static authentication rituals („enter your PIN”)

Toward:

. Continuous adaptive trust systems (AI systems that know you better than any password)

. Behavioral authentication (what you do is more identifying than what you memorize)

. Dynamic identity verification (AI-powered identity will become fluid, contextual and probabilistic)

UX changes:

. Security becomes invisible (users authenticated without conscious effort)

. Post-quantum trust indicators appear (showing users are in a secured quantum-resistant environment)

. Cryptographic migration journeys help users transition without understanding the cryptography

Quantum-safe and AI-secure dynamic security UX will become a separate strategic experience layer, not a friction point.

9. Financial Products Will Evolve Into Dynamic Systems

Today’s financial products are mostly fixed contracts. In 2035, products like loans, insurance, mortgages, investments and credit lines will be able to continuously adapt in real time based on live behavioral and environmental data.

Example: Users’ mortgage terms adjust dynamically to income changes, health indicators, climate exposure, location risks, energy behavior or macroeconomic volatility.

Financial customers will no longer buy static products; they will enter an adaptive relationship.

UX challenge: users will struggle to understand constantly evolving agreements.

Financial UX will become the interface between humans and adaptive products that don’t stay still.

10. The Emotional State Will Enter Financial Decision Architecture

AI systems will increasingly detect emotional and cognitive conditions, such as: impulsivity detection, stress signals, fatigue patterns, decision quality degradation, panic or emotional vulnerability.

Financial systems may intervene, delaying or altering high-risk decisions:

. blocking impulsive investment decisions

. delaying large transfers during high-stress periods

. changing risk recommendations based on emotional states

This introduces one of the biggest ethical tensions in future finance: where is the boundary between protection and control?

Autonomy vs. protection:

Do customers want the system protecting them from themselves, or do they want to make their own (potentially harmful) choices? This dilemma is similar to what happens in the car industry—safe AI drive or enjoying it on your own with manual driving?

UX challenge: How do we intervene in someone’s decision without triggering reactance? How do we protect without infantilizing? The financial interface becomes a negotiation between human independence and algorithmic protection. Financial UX will need to carefully balance autonomy, emotional safety, behavioral intervention and human dignity.

11. Financial Literacy Will Be Replaced by System Literacy

For decades, financial education has focused on helping users understand financial products. By 2035, users may no longer need extensive financial knowledge. This is similar to music, art and other industries in which AI-generated creativity compensates for users’ lack of knowledge.

UX education shifts from product explanation to autonomy management. The interface becomes a tutoring system that teaches governance, not finance.

12. The Ultimate Battle: Control vs. Convenience

By 2035, the biggest differentiators in finance won’t be features, speed or cost. It will be a philosophical choice: how much agency should users surrender?

Two competing paradigms then emerge:

Autonomous Finance

. Maximum convenience

. AI-led decisions

. Invisible optimization

. Users trust the system and let it work

Sovereign Finance

. Maximum user control

. Explicit governance

. Transparency and reversibility

. Users stay in charge, and the system advises

The future of financial services won’t simply optimize usability and functionality. It will design new human-machine financial relationships. They will have to choose a paradigm, commit to it, and execute it perfectly.

The institutions that succeed by 2035 will not be those that simply digitize banking better. They will be the ones capable of designing trustworthy relationships between humans, AI and digital money itself, potentially becoming the most important design challenge of the next decade.

The article in full here: 12 Digital Banking Predictions for 2035: The Rise of Robotic Money Experiences

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: