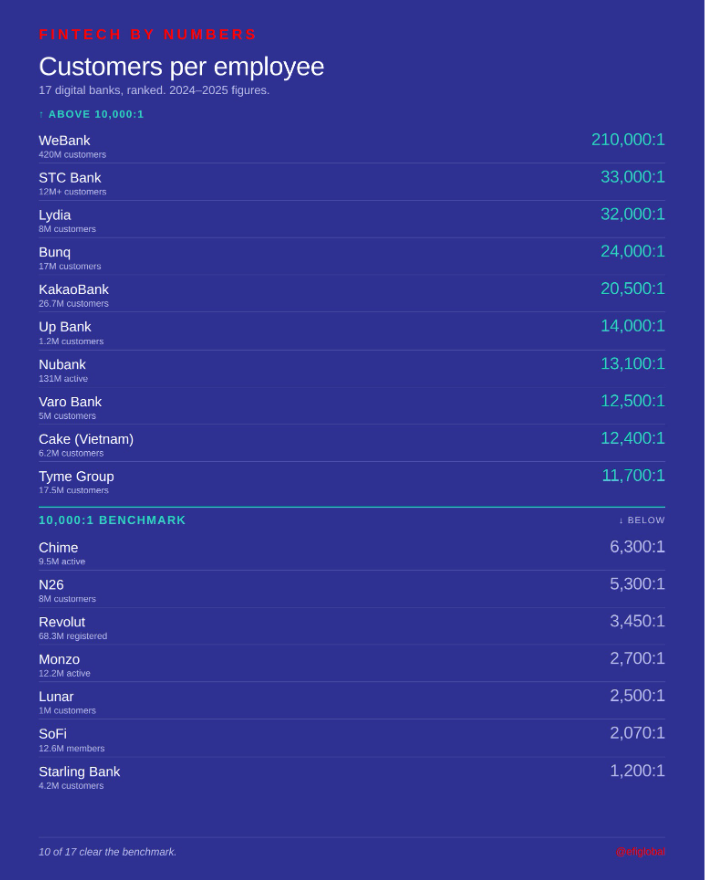

The 10,000:1 customer-to-employee lean banking benchmark

What should the average Customer-to-Employee ratio be in an AI-native banking industry? 10 million customers served by 1,000 bank employees only. A 10,000:1 customer-to-employee ratio could become the new benchmark for what a lean AI-native bank.

An article by Dr. Efi Pylarinou – top global fintech & tech influencer and advisor

This isnt a moonshot. Eleven digital banking providers I analyzed have already crossed this level.

I pulled the data on 17 digital banking players across nine markets to test the claim. From WeBank in China, Cake in Vietnam, STC Bank in Saudi Arabia, Tyme across South Africa and the Philippines, KakaoBank in South Korea, Lydia in France, Bunq in the Netherlands, Nubank across Latin America, Varo in the US, and Up in Australia. Each one cleared the 10,000:1 benchmark.

Most Western challengers, especially the ones built with full licences and broad product stacks, did not.

N26, Revolut, Monzo, Lunar, SoFi, Chime, and Starling all sit below the benchmark, and the trend is moving the wrong way. Revolut added roughly 4,000 employees in 2025 alone to reach 19,800 staff. Headcount grew about as fast as the customer base, which is not the way AI is supposed to impact operational scale (evidently, too early for AI to show up in the bottom line).

The customer-to-employee ratio worsens as licences expand and the compliance, lending, and SME machinery scales.

𝗥𝗲𝗴𝗶𝘀𝘁𝗲𝗿𝗲𝗱 𝘃𝗲𝗿𝘀𝘂𝘀 𝗮𝗰𝘁𝗶𝘃𝗲 𝗶𝘀 𝘁𝗵𝗲 𝗳𝗶𝗿𝘀𝘁 𝘁𝗵𝗶𝗻𝗴 𝘁𝗼 𝗮𝗱𝗷𝘂𝘀𝘁 𝗳𝗼𝗿. Nubank, Chime, Monzo report active customers. WeBank, KakaoBank, Bunq, Revolut report total registered, dormant accounts included. The gap between the two bases is typically 2-5x. Many challenger banks stay deliberately vague about actives because the gap is unflattering. Monzo and Chime disclose because they look good on it. Revolut and N26 do not.

So is 10,000:1 a north star or should it be the new Lean AI-enabled industry standard?

WeBank is past it by a factor of 21. KakaoBank is past it on a fully licensed retail bank serving 26 million Koreans. Nubank is past it serving 131 million Latin Americans on the more demanding active basis. The question is no longer whether the ratio is achievable. It is how long it takes the rest of the industry to make it the floor rather than the ceiling. Five years? Ten years?

The 10-million-customer, 1,000-person bank already exists. In Saudi Arabia, in Vietnam, in South Africa, in South Korea, in Brazil. Western challengers sit below the benchmark not because of legacy infrastructure.

So can agentic banking compress that operating model enough to make 10,000:1 the industry average? Or will the gap stay structural? I will run this same analysis in twelve months. We will see who moved.

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: