Druid is launching the AI Adoption Benchmark as an annual series. The 2026 edition, the first installment, draws on 15 months of anonymized, aggregated production telemetry from Druid customers across Healthcare, Higher Education, Financial Services, and HR & IT. The data was collected through Druid Analytics & Insights and shows how AI is actually used once agents are live inside customer, student, patient, and employee service journeys.

Most published „State of AI” content captures executive sentiment, budget intent, and pilot plans. Druid’s benchmark adds a different signal: production behavior. It shows where demand concentrates, which channels users choose, when conversations arrive, and how often AI resolves work before a human joins.

AI Adoption in Financial Services Benchmark

Most financial services AI reports show what leaders plan to do. Druid’s AI adoption in financial services benchmark shows what actually happens once AI is live in customer-facing service journeys: where usage lands, which experiences dominate volume, and what financial services leaders should expect from real-world deployments.

INSIGHT 01

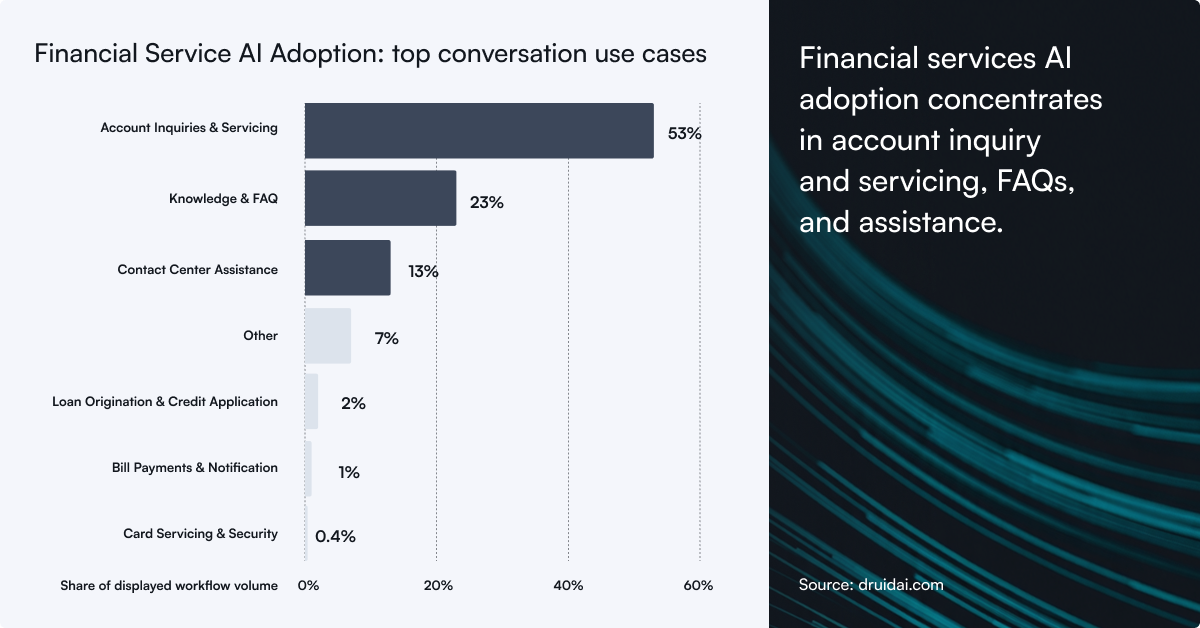

AI adoption in financial services starts with account inquiry and servicing, FAQs, and assistance

Account Inquiry & Servicing makes up 53% of the financial services CX workflow mix, Knowledge & FAQ contributes 23%, and Contact Center Assistance adds 13%. Together, those three categories represent 90% of the published mix. The pattern shows that production AI agent demand concentrates first in secure access to my account for inquiry and servicing, high-frequency knowledge delivery, and assistance journeys before it spreads across narrower service cases.

The remaining 10% sits in lower-volume specialist workflows such as loan origination, bill payment, and card security. Those use cases matter, but they are clearly secondary to the account, knowledge, and assistance core.

The first production wave of AI agents in financial services is not exotic. It is operational. Customers want help with the questions and tasks they already bring to digital banking every day: account details, statements, transactions, payments, FAQs, and guided assistance. That makes account servicing the natural land use case for AI agents because it combines high volume, repeatability, and direct pressure on service capacity.

INSIGHT 02

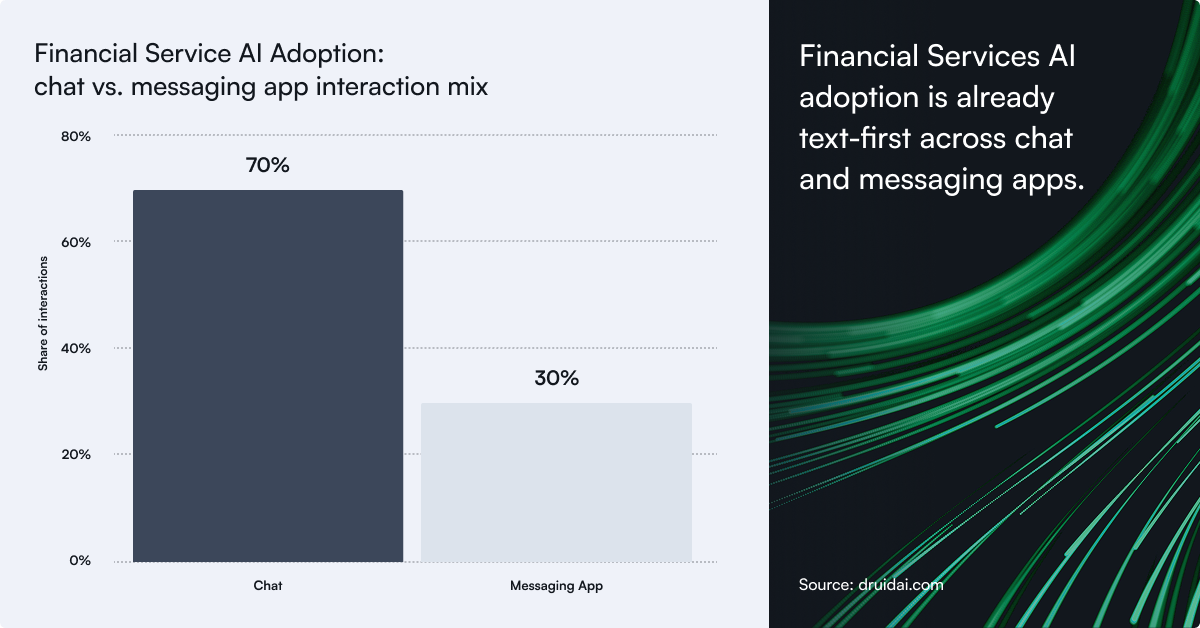

AI adoption in financial services is already text-first across chat and messaging apps

Chat accounts for 70% of engaged financial services CX interactions, while messaging apps account for 30%. In this benchmark, “chat” includes both website chat and chat experiences embedded inside mobile apps, such as mobile banking apps. The production benchmark is clear: financial services AI agent usage is overwhelmingly text-based, but the text surface is not limited to a single web-chat entry point. Customers are already bringing material demand through messaging app channels, so leaders should plan for a broader digital messaging layer.

The benchmark points to a text-first service model. Chat leads, but messaging apps are already large enough to matter. In regions such as EMEA, where messaging apps like WhatsApp are widely used for banking and business transactions, this behavior is already part of the customer-service fabric—and similar expectations may expand to North America over time. For financial services, the implication is clear: AI should not be deployed as a single web-chat widget. It should be treated as a governed digital messaging layer that can follow the customer across mobile, online banking, messaging apps, and assisted-service journeys.

INSIGHT 03

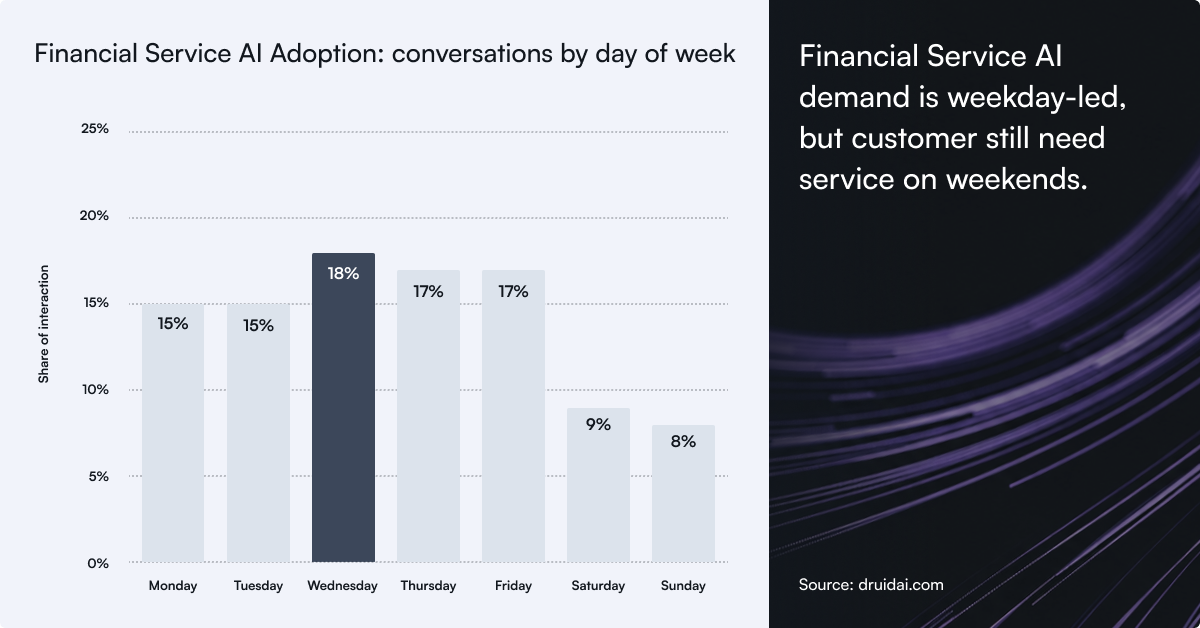

Financial Services AI demand is weekday-led, but customer still need service on weekends

Wednesday accounts for 18% of total financial services CX interactions. Monday through Friday contributes 83%, while the weekend still contributes 17%. That pattern is useful for planning: financial services AI demand follows the business week, but customer service expectations do not disappear on Saturday and Sunday.

The weekday concentration confirms that AI should be planned as part of the operating model, not as an experimental digital overlay. But the weekend share is equally important: customers still need help when staffing is thinner. For banks, AI agents create a continuity layer that keeps routine service available even when branches and contact centers are operating with reduced coverage.

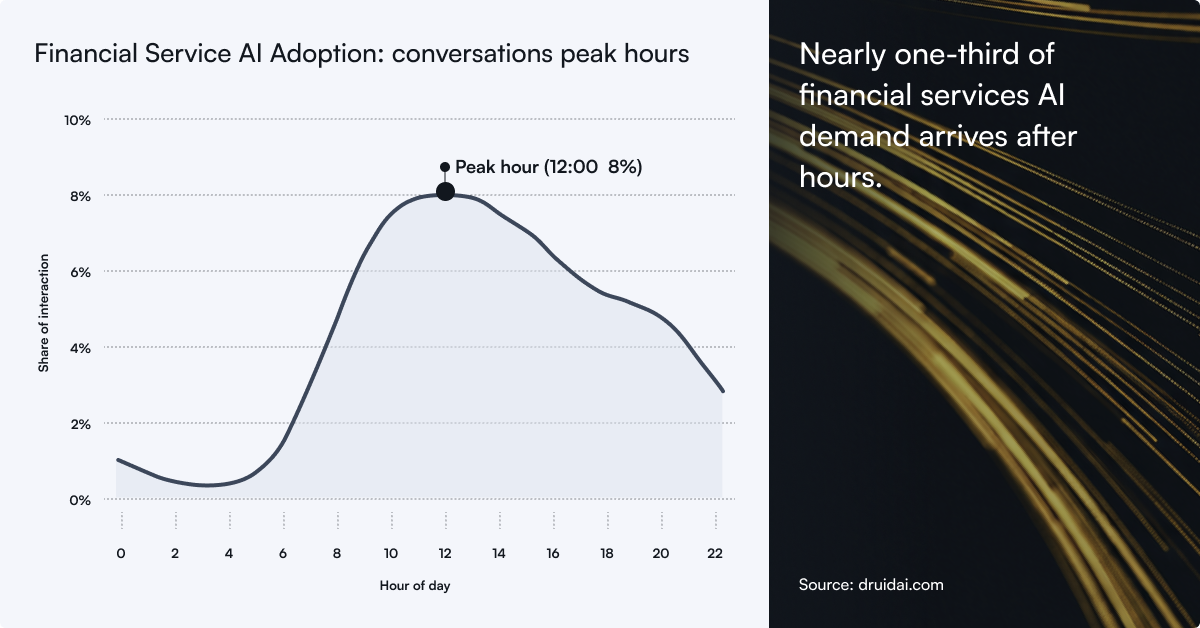

INSIGHT 04

Nearly one-third of Financial Services AI demand arrives after hours

69% of Financial Services CX interactions land between 8 AM and 5 PM, with the single highest hourly share appearing at 12 PM at 8%. Another 31% arrives outside that window. For financial services leaders, that makes AI less like a web widget and more like an always-available service layer that supports customers when staffed coverage is thinner.

The after-hours share changes the business case. If nearly one-third of demand arrives outside traditional service hours, then AI is not just a containment tool for the contact center. It is an always-available operating layer that helps banks serve customers when live coverage is limited, while still escalating sensitive or exception-based journeys when required.

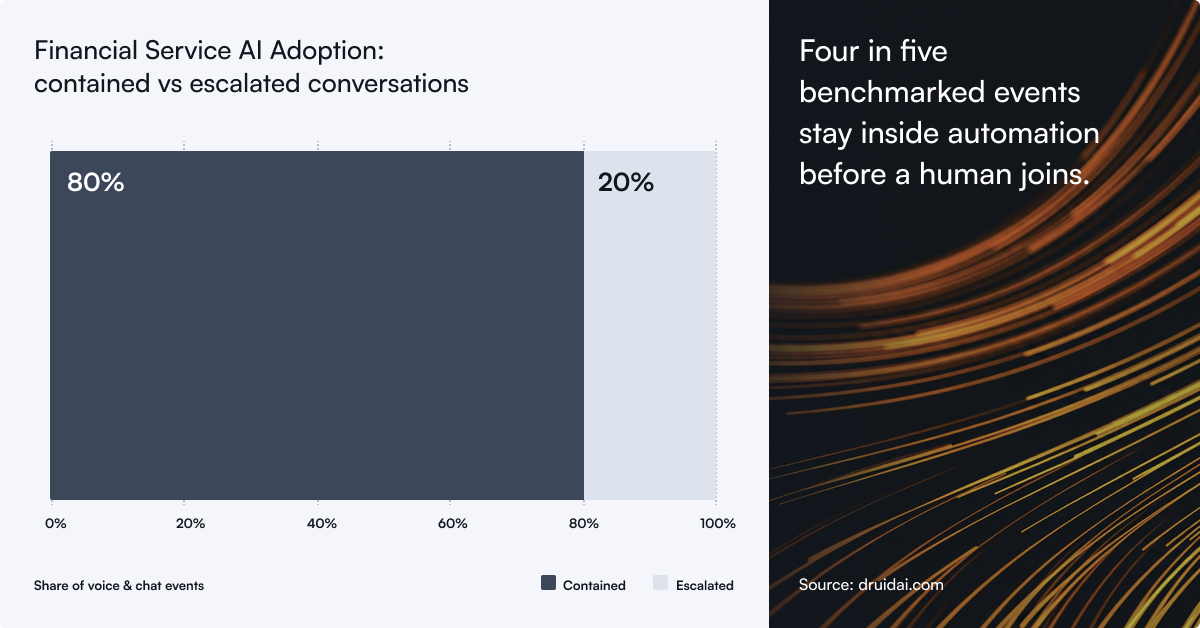

INSIGHT 05

Most Financial Services AI conversations stay contained, but escalation is part of the design

Contained events account for 80% of aggregate voice and chat events, while escalations account for 20%. In financial services, an escalation is not automatically a failed automation event. Some handoffs are intentional and important because the journey requires risk review, policy treatment, exception handling, identity-sensitive work, or live staff involvement. Many banks also want human agents focused on higher-value advisory and revenue opportunities, such as mortgage refinancing, card upgrades, lending conversations, or other product discussions where human judgment and relationship context matter.

For financial services journeys, the right measure is not whether every interaction avoids a human, but whether the AI agent resolves routine work safely, operates within approved policies, identifies exceptions correctly, and hands off with context when policy, risk, identity, compliance, or customer sensitivity requires a banker or service agent.

That is why human-in-the-loop design matters: AI can automate low-value, repeatable service journeys while maintaining auditability, supporting defensible escalation, reducing the risk of drift, bias, or non-compliant responses, and freeing human agents to handle regulated decisions, complaints, fraud signals, lending conversations, sensitive customer needs, and qualified opportunities for deeper financial engagement.

More details here: AI Adoption in Financial Services Benchmark: What 15 months of production data actually reveals

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: