![]()

![]()

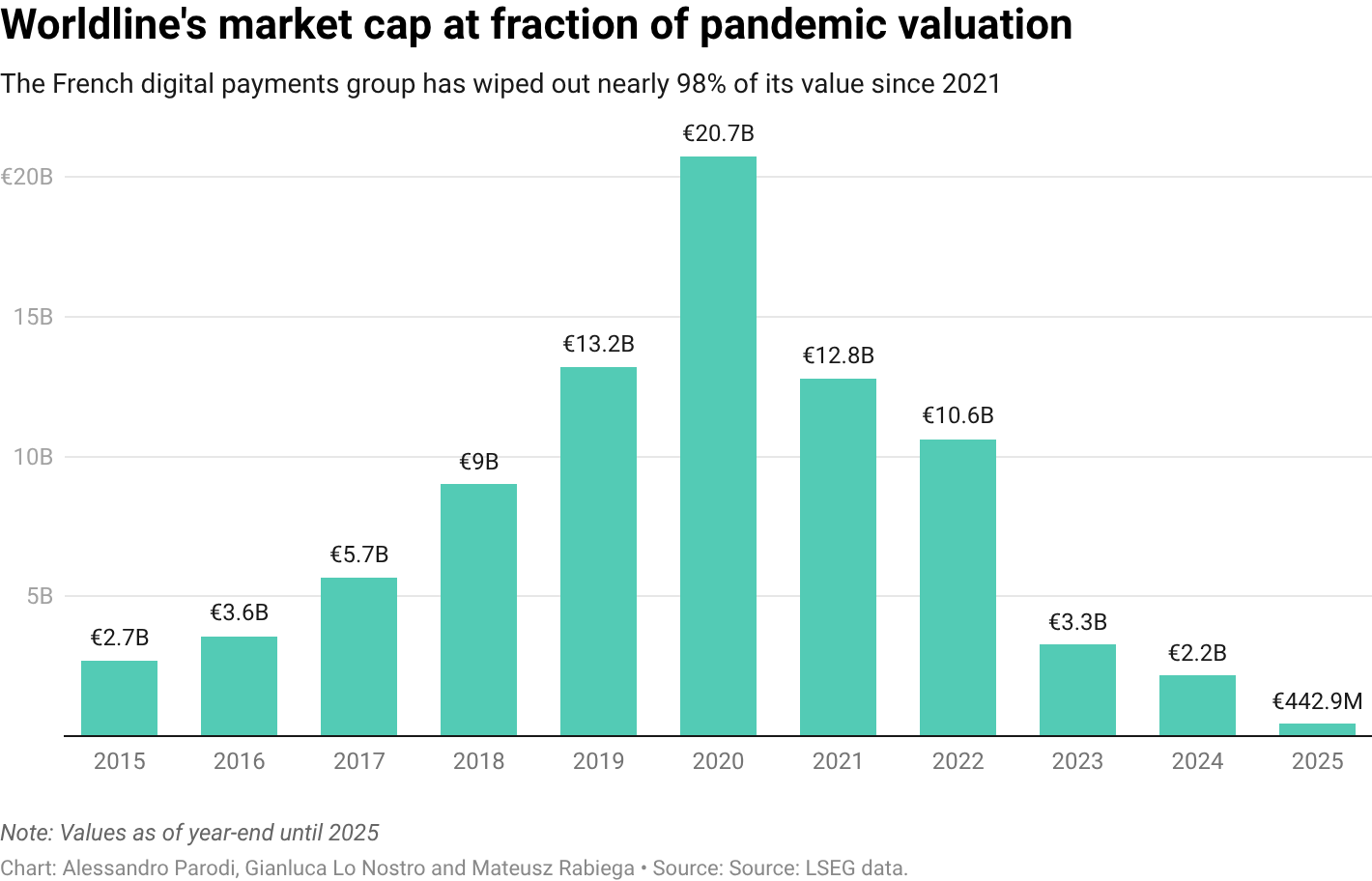

Digital payment service group Worldline’s disposal of non-core parts of the business is near completion, the company said as it reported annual results in line with guidance after a transformational year under its new CEO, according to Reuters.

Strategic reshaping of the portfolio is nearing the end

With the announced disposal of Worldline’s merchant services business in India and the progress reached in the remaining processes, the execution of the pruning program is nearing the end. Worldline North America, Cetrel and Payment IQ expected to close in Q1 2026 while MeTS is on track for Q2 2026.

The entire perimeter under the pruning program (including those still in process) are presented as “assets held for sale” according to IFRS 5. For reference, the 2025 revenue, adjusted EBITDA and FCF deconsolidation impact of the perimeter on the Group are respectively estimated at c.€900M, €200M and €55M on a full year basis.

„Considering this progress, the company has implemented a streamlined operating model, focused on the execution of its European strategy. The more focused scope enables the organization to strengthen its position as a leading European operator of major payments infrastructure. As a result of the contemplated pruning, Worldline’s headcount is expected to decline by around 30%.” – the company said in a press release.

The Paris-listed company reported a 2.4% decline in annual revenue to 4.5 billion euros ($5.3 billion), including the digital services business that is due to be sold as part of the disposal programme. Adjusted core profit, meanwhile, stood at 841 million euros, within the forecast range of 830 million to 855 million euros.

Main business lines contribution to 2025 results

Worldline’s FY 2025 revenue reached €4,030 million, 2.7% below 2024.

Merchant Services 2025 revenue reached €3,238 million, -1.4% year-on-year and -4.4% on a net net basis). The performance was impacted by the off boarding of the remaining high brand risk (HBR) portfolio in H1 and by challenges in POS terminal deliveries, which were mostly resolved by year-end. While the SMB was impacted by net churn in core geographies, churn improved as from Q4 2025, and the segment recorded solid growth in several markets where it holds challenger positions, notably in Southern and Central Europe. Adjusted EBITDA totalled €624 million, representing 19.3% of revenue (versus 23.3% in FY2024), and was impacted by lower revenue and a less favorable client mix. Despite the positive impact of Power24, OPEX remained stable due to actions taken on inventory, compliance audits and FCC remediation.

Financial Services’ 2025 revenue came to €792 million, representing a 7.7% organic decline, impacted by the termination of specific contracts, while the issuing processing activity was stable. Adjusted EBITDA reached €172 million, or 21.7% of revenue, vs 27.4% in 2024, cost reduction being insufficient to offset the decline of revenue in the period.

Despite the positive impact of Power 2024, corporate costs amounted to €59 million in 2025 (€54 million in 2024) notably as a result of non recurring expenses (transition, audits, strategic review).

The Group’s adjusted EBITDA therefore reached €737 million in 2025 (18.3% of revenue) and the EBITDA €585M, vs €661M millions in 2024, benefiting from lower restructuring costs than in the previous year.

2026 expectations

The Company’s outlook for 2026, under IFRS 5 and excluding the contribution of all divestments, as assets held for sale, is :

. Low single digit organic revenue growth ;

. Adjusted EBITDA of around €630m to €650m ;

. Free cash flow of €(80)m to €(70)m, which includes investment in remediation measures of €30m-€40m, and investment in North Star initiatives of €40m-€50m.

As of December 31, 2025, the Group maintained its strong liquidity profile with a total cash position of €0.9bn (and an additional €186m cash in the divested entities’ scope) and an undrawn revolving credit facility of €1,125 million maturing in 2030.

By the end of H1 2026, Worldline expects to have significantly strengthened its balance sheet and liquidity profile, thanks to the proceeds of divestments (c.€540m to €590M) and the planned €500 million capital increase. Combined with strict capital discipline, these actions underpin a clear deleveraging trajectory, targeting net debt below 2.0x adjusted EBITDA by 2026.

The available liquidity will cover debt maturities for 2026 and 2027 before the rights issue, positioning the Group for improved financial resilience.

2030 outlook confirmed and adjusted to the new scope

. Organic revenue growth of ~4% CAGR between 2027 and 2030 ;

. Adjusted EBITDA target of €900m+(versus €1bn+ previously announced), reflecting the impact of the fully pruned scope ;

. Free cash flow expected at €300m–€350m annually, unchanged versus prior guidance, demonstrating resilient cash flow generation despite a streamlined scope.

CEO Pierre-Antoine Vacheron said that the fourth quarter marked a „decisive turning point” for Worldline and that he believes the earnings report and a 500 million euro capital increase in March will draw a line under two years of crisis at the French payments group.

Vacheron commented: “Q4 marked a decisive turning point for Worldline. Our operational turnaround is firmly underway, our pruning program is nearing completion. The foundations of a stronger, more focused Company are now in place. Thanks to these tangible advances, we confidently reaffirm our 2026 outlook, fully aligned with the North Star 2030 trajectory.

With the upcoming capital increase, we will accelerate our commitment to customer excellence, resilience, and innovation. By executing our transformation roadmap with discipline and intensity, we are positioning Worldline to become the leading European operator of critical payments infrastructure — delivering sustainable value for our clients, our employees, and all our stakeholders.”

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: