U.S. Credit-Card Debt Surpasses Record Set at Brink of Crisis

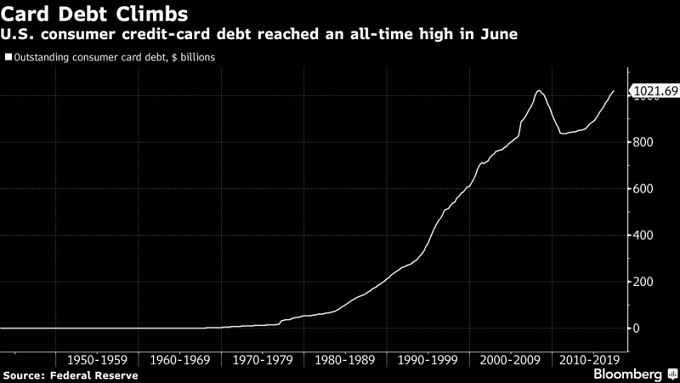

U.S. consumer credit-card debt just passed an ominous milestone, beating a record set just before the global financial system almost collapsed in 2008.

Outstanding card loans reached $1.02 trillion in June, data from the Federal Reserve show, as lenders including Citigroup Inc. and JPMorgan Chase & Co. compete to sign up cardholders who may carry balances – a relatively lucrative business in a prolonged period of low interest rates.

The bet is that this time it won’t end so badly. In 2008, a drop in home prices spiraled into a global financial meltdown, and after the jobless rate surged toward 10 percent, banks wrote off more than $100 billion in credit-card loans over the next two years.

Investors have been skittish over the potential for defaults to rise ever since card balances eclipsed $1 trillion in February. Credit-card issuers Capital One Financial Corp., Synchrony Financial and Discover Financial Services said write-off rates ticked up in the second quarter from the previous three months.

Source: Bloomberg

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: