![]()

![]()

International card schemes MasterCard and Visa now account for 86% of all payment cards in Europe, as domestic and private label schemes continue their decline. RBR’s study Global Payment Cards Data and Forecasts to 2020 shows that €9 out of €10 spent using a payment card in Europe was made on a Visa or MasterCard-branded card – the highest share of any region.

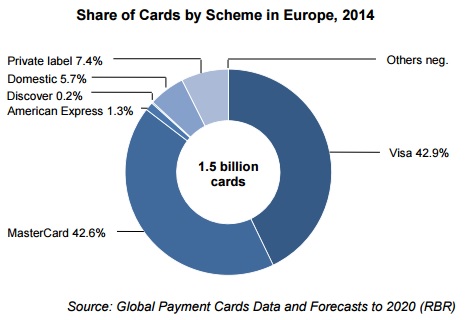

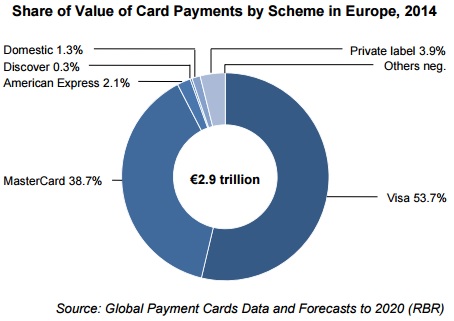

There were 1.5 billion payment cards in circulation in Europe at the end of 2014 which were used for payments worth €2.9 trillion during the year. Competition between the two leading schemes is fierce, with very little difference between Visa and MasterCard in terms of card numbers. With regard to payment value, however, Visa is by far the larger scheme, and gained a percentage point of value share in 2014, while MasterCard lost a percentage point.

Visa and MasterCard have almost the same share of card numbers

With 42.9% of payment cards in issue in Europe, Visa is slightly ahead of MasterCard (42.6%). MasterCard’s share rose from 41.9% in 2013, as a result of a strong performance in a number of markets including Russia and Ukraine, as well as the Nordic and Baltic countries, while Visa’s share remained largely unchanged. RBR’s figures show that Visa is the largest scheme in 19 countries in the region, while MasterCard is the largest in the remaining 14.

The other international schemes (American Express, Discover, JCB and UnionPay), account for less than 2% of the regional card base, unchanged since 2013. A significant, though declining, proportion of cards are domestic bank card schemes or private label cards. The former are numerous in Russia and to a lesser extent Ukraine, which together account for more than 80% of such cards in the region. Meanwhile, the largest European markets for private label cards are France, Spain, Germany and the UK, which make up three quarters of the region’s private label sector. Such cards are, however, being progressively replaced by those carrying an international brand.

Visa leads in terms of value of card payments

Visa accounts for 54% of card expenditure, and holds a greater lead over MasterCard than for card numbers. Payment cards are used frequently in several of the markets where Visa cards are predominant, for example France and the UK. Furthermore, Visa has a high share of debit cards in the region, which typically receive greater usage than pay-later cards.

The markets where the RBR report showed MasterCard to have gained share of card numbers include Russia and Ukraine where cards are used for fewer than 25 payments per year on average – one of the reasons why MasterCard’s rise in share in card numbers does not translate into an increase in value share.

American Express and Discover both account for a somewhat higher share of value than of cards because they are typically used for relatively high-value payments. In contrast, domestic and private label cards account for a lower share, and their share of value declined in 2014. This is because domestic cards, such as those issued in Russia, are used infrequently. The same applies to private label cards whose limited acceptance network generally restricts their usage even though they are often used for high-value payments.

Card schemes will no longer be able to compete, to the extent they have in the past, on interchange fees, with the new EU caps of 0.2% for debit cards and 0.3% for pay-later cards. RBR believes that portfolio gains will instead be based on factors such as service levels and scheme fees, meaning that competition between the card schemes in the region will be as intense as ever.

These figures and insights are based on RBR’s Global Payment Cards Data and Forecasts to 2020 report. RBR is a strategic research and consulting firm with three decades of experience in retail banking, banking automation and payment systems.

Source: RBR’s study Global Payment Cards Data and Forecasts to 2020

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: