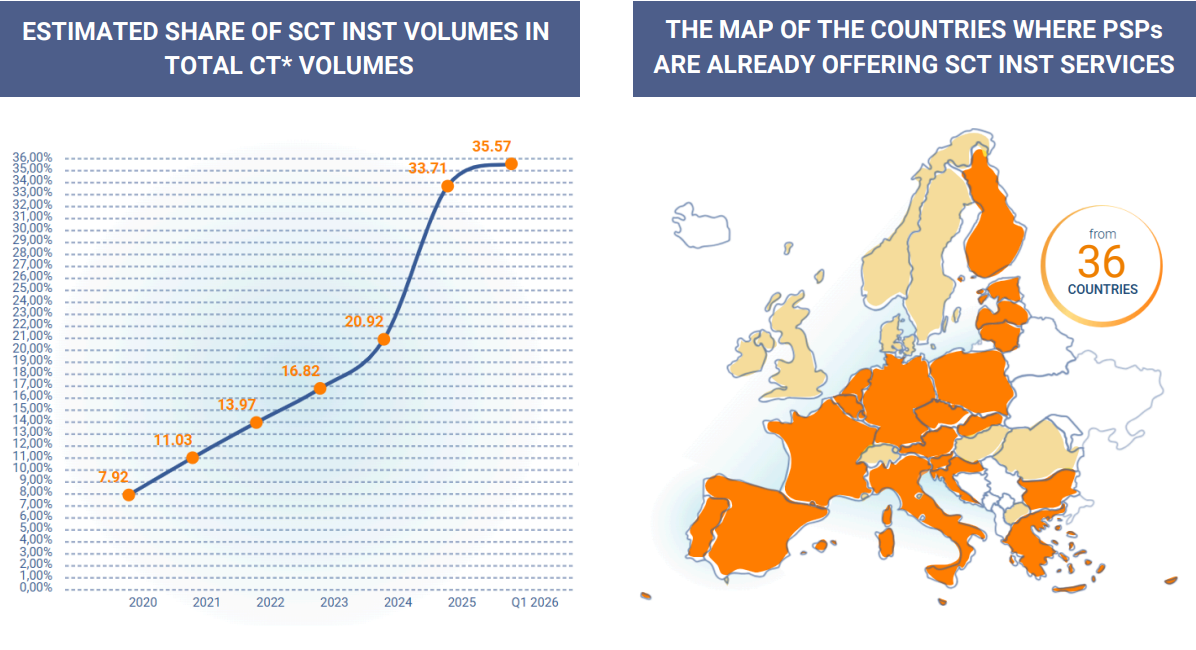

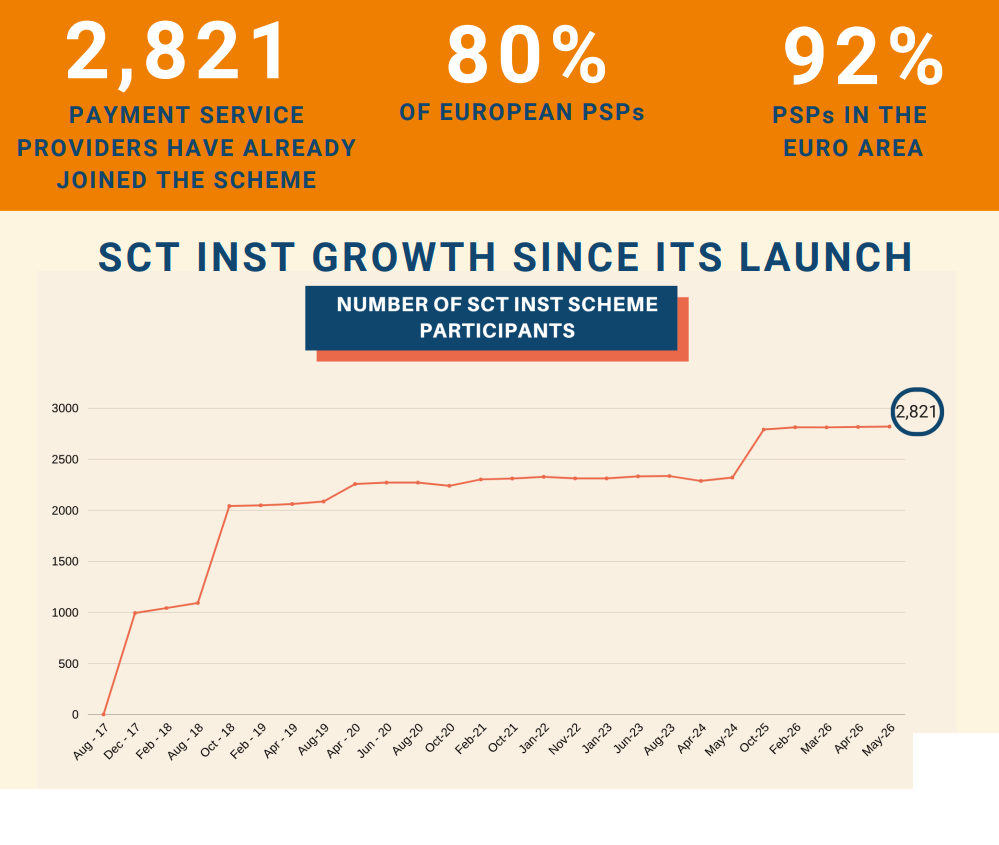

European Payments Council revealed the latest figures for the SEPA Instant Credit Transfer Scheme adoption. As of May 2026, there are 2,800 Payment Service Provider from 35 European countries that are already offering SCT INST services.

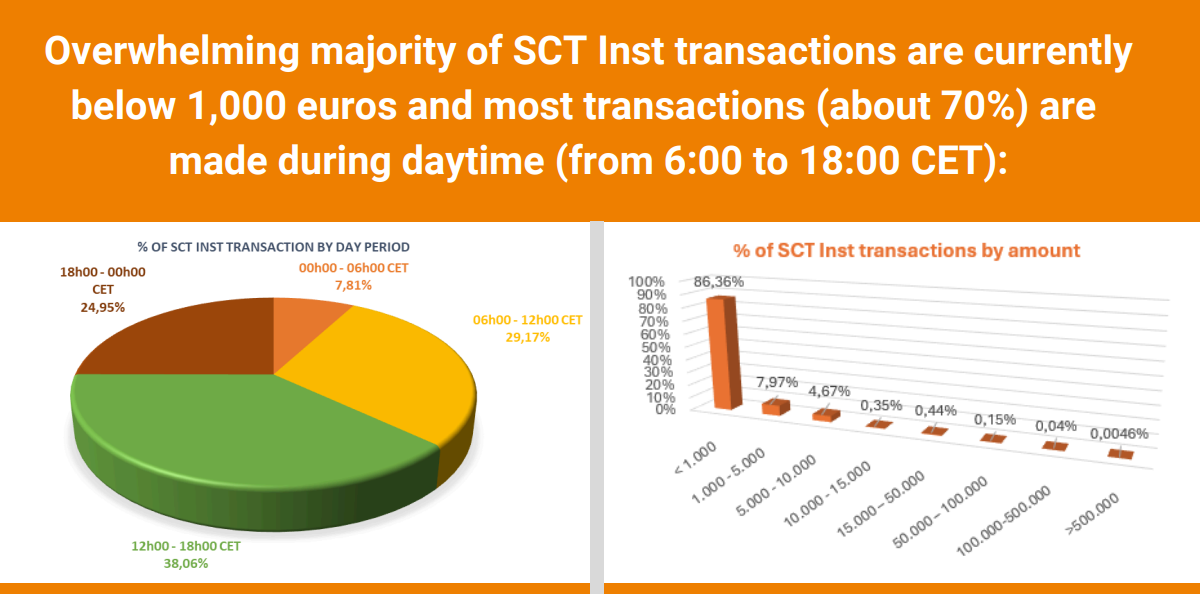

Overwhelming majority of SCT Inst transactions are currently below 1,000 euros and most transactions (about 70%) are made during daytime (from 6:00 to 18:00 CET). About 99% of transactions are completed in less than five seconds.

SCT Inst is a pan-European instant payment scheme that allows domestic and cross-border payments in euro to be made to and received from participating payment service providers (PSPs) anywhere in the Single Euro Payments Area (SEPA).

text

There is no longer a maximum amount at SCT Inst scheme level. This is very convenient for

Business-to-Business payments!

The SEPA Instant Credit Transfer (SCT Inst) scheme was launched in 2017 to provide a single set of rules, practices and standards and increase harmonisation of instant payments in euro.

In September 2021, the ECB published an overview of the general benefits of instant payments. In October 2022, the European Commission adopted a legislative proposal to make instant payments in euro affordable, secure and available to all citizens and businesses holding a bank account in

the EU or the European Economic Area.

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: