![]()

![]()

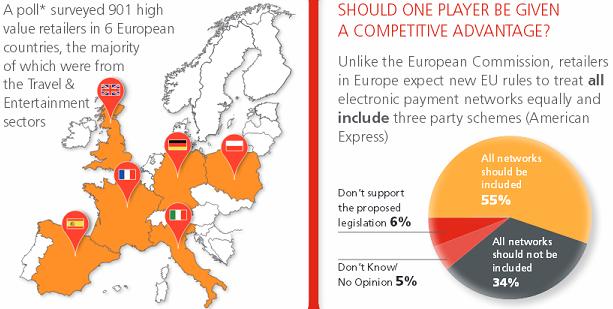

The majority of high value retailers support EU legislation only if it includes all electronic payment networks. A new MasterCard survey shows that the majority of high value retailers in Europe believe that draft EU rules to cap fees for electronic payments should only go ahead if they apply to all electronic payment network.

The survey was conducted by Ipsos MORI on behalf of MasterCard, interviewing 901 high value retailers across six European countries to investigate their views on proposed EU payments legislation.

So called three party card schemes, such as American Express and Diners Club, are currently largely excluded from the scope of the draft rules. This is despite the fact that the European Commission acknowledges that they operate an implicit interchange fee model – similar to that applied by four-party models, such as MasterCard.

Around two in three (63%) high value retailers across 6 European countries accept American Express cards. American Express is rated as having the highest payment charge fees overall; 69% rate American Express’ fees as ‘very or fairly high’ followed by 47% rating MasterCard’s fees as high and 46% rating Visa’s fees as high.

The majority (55%) of retailers surveyed would only support the proposed legislation to cap fees for electronic payments if all card network operators, including American Express and Diners Club, were covered. Only 34% would support EU legislation that excludes specific card brands. In the six countries surveyed, more than two in three retailers (69%) rate Amex fees higher with little difference in satisfaction of the services provided.

Support for the proposed legislation to include all payment cards is highest in Germany (66%) followed by Spain (65%), Italy (59%), France (53%), Poland (44%) and Great Britain (42%).

When asked how they would use any money saved from a cap on interchange fees, 59% of high value retailers across all countries surveyed claim that it would be used to innovate or invest in their business rather than to reduce retail prices for their customers (an option favored by 15%).

Countries where retailers are most likely to use the money saved to innovate their business, in ranked order are France (69%), Spain (64%), Germany (61%), Poland (61%), Italy (51%) and Great Britain (50%).

Only a relatively small number of high value retailers in each country claim that they would reduce retail prices for their customers, in ranked order, Spain is the most likely to do so (20%), followed by Italy (19%), Poland (17%), Great Britain (16%), France (8%) and Germany (8%).

“Although we appreciate the Commission’s and Parliament’s efforts so far to treat all players in the same way, we believe that the proposals could be improved. As they currently stand, they risk playing directly into the hands of the most expensive market players. Consumers and retailers would end up paying the price. This is hardly what the legislation was intended to achieve.” said Javier Perez, President, MasterCard Europe.

The convenience of electronic payments while travelling is just one example of why consumers increasingly favour cards over cash. According to research carried out by MasterCard in the summer of 2013, over 90% of Europeans carry cards while on holiday versus 60% at home.

“At MasterCard, we support the European Commission’s goal of promoting the use of electronic payments. The draft regulation should be amended to cover implicit interchange fees operated by three party schemes. This can be achieved fairly simply through the introduction of rules on accounting separation already applied in other areas of EU legislation, such as telecommunications or energy”, Mr Perez concluded.

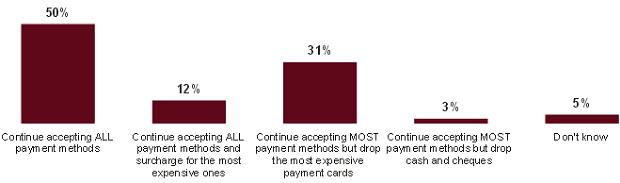

Knowing that the cost to the business varies depending on the payment methods the business accepts, and knowing that there might be caps on costs for some payment cards and not others would you:

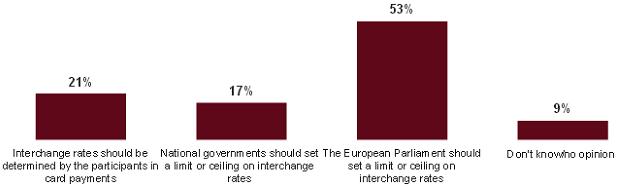

Which of the following best describes your point of view regarding capping or setting limits on interchange rates?

The research was conducted by global research company Ipsos MORI on behalf of MasterCard. 901 retailers participated on a country by country basis via telephone interviews. The following countries took part: France, Germany, Great Britain, Italy, Poland, and Spain. Sectors were selected based on likelihood for having relatively high value and volume of credit card transactions and include: airline ticket sales, car rental agencies, department stores, hotel and resorts, jewellery shops, petrol stations, restaurants, theatres, museums or galleries, travel management companies/travel agencies and other high value stores. Fieldwork was conducted between 15th April and 9th May.

In each market a broad spread of interviews were conducted across these sectors and with different sizes of business. Respondents were screened via the questionnaire based on their familiarity with day-to-day transactions in their branch or outlet, as well as their knowledge of card payment fee processes.

The sample of retailers surveyed showed a relatively high understanding of interchange rates; more than three in four (79%) reported that they know “a lot” or “a fair amount” about the different fees charged for different payment methods.

The full results of the research can be found here.

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: