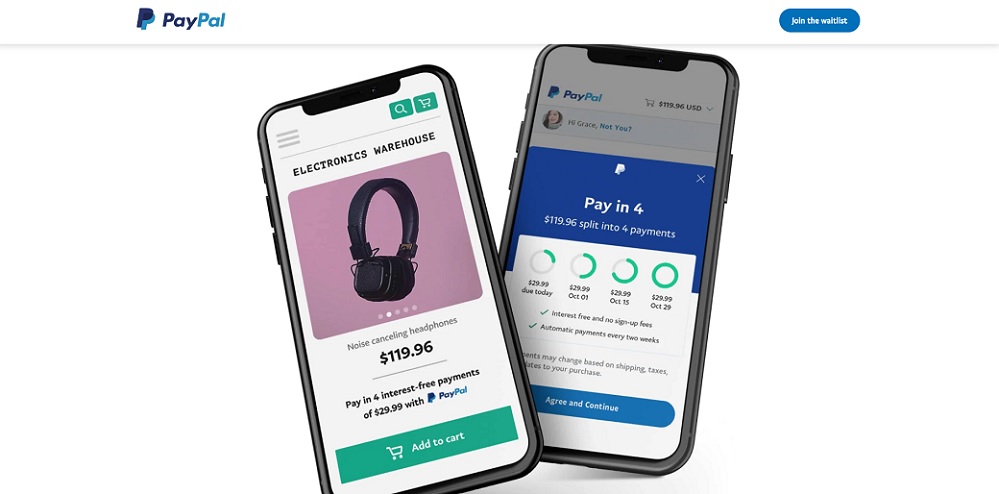

PayPal Holdings, Inc. today announced „Pay in 4,” a short-term installment offering for customers in the U.S. Pay in 4 can help merchants drive conversion, revenue and customer loyalty without taking on additional risk or paying any additional fees, while enabling consumers to make a purchase and pay over four, interest-free installments.

Pay in 4, which is part of PayPal’s growing suite of Pay Later solutions, enables merchants and partners to get paid upfront while enabling customers to pay for purchases between $30 and $600 over a six-week period. Pay in 4 is included in the merchant’s existing PayPal pricing, so merchants don’t pay any additional fees to enable it for their customers. Consumers pay no fees1 or interest, and payments are seamless with automatic re-payments. Pay in 4 will also appear in the customer’s PayPal wallet, so they can manage their payments in the PayPal app.

The PayPal platform – used by over 80 percent of 100 leading U.S. retailers surveyed – enables merchants to access all their payment and commerce needs within one trusted platform, while driving increased conversion. PayPal Checkout converts 82 percent higher2 on average than a checkout without PayPal, and PayPal’s Pay Later products are helping connect merchants with new customers every day. Businesses that promoted PayPal Credit on their site saw a 21 percent increase3 in sales versus those who did not, and merchants with pay over time messaging on their site saw a 56 percent increase4 in overall PayPal average order values. Merchants can now also add dynamic messaging to deliver relevant, in-context pay later options early in the shopping journey, from the homepage, to product pages, to checkout.

PayPal is focused on enabling choice in how and when customers can pay, including via credit and debit cards, PayPal, Venmo, alternative payment methods, rewards points, PayPal Credit, and other flexible financing options. Consumers are 54 percent more willing to buy when a business accepts PayPal, and 25 percent of people have abandoned a transaction because their preferred payments provider wasn’t available. In addition, with a two-sided platform of 346 million global active merchant and consumer accounts, PayPal can help connect merchants with new customers.

Along with Pay in 4, PayPal offers several other financing options. PayPal Credit, a reusable line of credit with various promotional offers built in like 6 months special financing and Easy Payments, available in the U.S. and U.K., is the most commonly used buy now pay later service. PayPal also offers PayPal Ratenzahlung and Paiement en 4X – installment products in the German and French markets and Pay After Delivery, a buy now, pay later offering in Australia, Canada, France, Germany, Spain, the Netherlands and UK.

Pay in 4 will be available to consumers on qualifying purchases in early Q4 2020.

###

1. Consumers pay no interest and no origination fees. A late fee may be applied if the payment isn’t received on time.

2. Checkout conversion is measured from the point when a consumer selects a payment type to completion of purchase within the same browsing session.

3. Average annual incremental sales based on PayPal’s analysis of internal data among 210 small and middle market merchants with annual online sales up to $37M with messaging and buttons against a broader group of merchants that did not, with 24 months of continuous DCC volume between January 2016 and November 2019.

4. Average lift in overall PayPal AOV for merchants with PayPal Credit messaging versus those without, 2019 PayPal internal data.

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: