NOCASH conferences: „The European payments landscape is changing. Be ready!”

European authorities and Romanian key institutions in charge with the implementation of the new Payment Services Directive will discuss in Bucharest about how the new business environment is about to change, pretty soon.

European Banking Authority – EBA, Ecommerce-Europe, National Bank of Romania – BNR, Romanian Banking Association – ARB, the National Authority for Consumer Protection – ANPC, will join together to make a very comprehensive analyse of the threats and opportunities from the every player’s perspective.

WHERE: Romanian Banking Institute, Aula – WHEN: April 12, 2017 – EVENT AGENDA

Be sure you won’t miss this exceptionally event! Reserve your place HERE!

MAIN PARTNER

BUSINESS PARTNERS

STRATEGIC PARTNERS

MEDIA PARTNERS

SPEAKERS

__________________________________________________________________________________________

LARISA ŢUGUI is a policy expert in retail payments at the European Banking Authority (EBA), London. Larisa joined the EBA in November 2016 and is part of the EBA’s Consumer Protection, Financial Innovation and Payments Unit, contributing mainly to the development of the mandates conferred on the EBA under the EU legislation on payment services and to the EBA’s work on the monitoring of financial innovation (covering aspects like crowdfunding, automation in financial advice, ‘big data’ and ‘fintech’ more widely).

LARISA ŢUGUI is a policy expert in retail payments at the European Banking Authority (EBA), London. Larisa joined the EBA in November 2016 and is part of the EBA’s Consumer Protection, Financial Innovation and Payments Unit, contributing mainly to the development of the mandates conferred on the EBA under the EU legislation on payment services and to the EBA’s work on the monitoring of financial innovation (covering aspects like crowdfunding, automation in financial advice, ‘big data’ and ‘fintech’ more widely).

Before joining the EBA, Larisa worked as a lawyer for 8 years at a top-tier Romanian law firm in Bucharest, where she specialised in finance transactions and financial services regulatory aspects.

Larisa is a member of the Bucharest Bar and holds two Degrees in Law from the University of Bucharest and from Paris I Panthéon Sorbonne University, and two Master Degrees from Paris I Panthéon Sorbonne University in Business and Tax law and in European Law.

___________________________________________________________________________________________

JUST HASSELAAR – The co-Chair of the e-Payments Working Committee – Ecommerce Europe (Thuiswinkel.org<https://www.thuiswinkel.org/>, The Netherlands).

JUST HASSELAAR – The co-Chair of the e-Payments Working Committee – Ecommerce Europe (Thuiswinkel.org<https://www.thuiswinkel.org/>, The Netherlands).

Besides his role with Ecommerce Europe, Just Hasselaar is a technical expert on the Euro Retail

Payments Board, chaired by the European Central Bank, and a member of the Scheme End-User Forum of the European Payments Council. Next to this, Just Hasselaar is an advisor for Payments at Thuiswinkel.org, the association for the B2C e-commerce industry in The Netherlands. In this role, Just Hasselaar is secretary of the payments working committee of Thuiswinkel.org.

The Working Committees are issue-based bodies that determine the overall public affairs strategy on legislative issues at European level. During the meetings and in continuous liaison with the Ecommerce Europe team in Brussels, the members determine and execute public affairs strategies on key lobbying dossiers. Working Committee members are policy experts from the National Associations and Company Members.

The Ecommerce Europe e-Payments Working Committee deals with different topics related to the landscape of online and mobile payments from new legislation and technical standards coming from the European policy makers tothe latest innovations in the payments market in Europe. Current policy priorities of the e-Payments Working Committee include mobile and innovation in payments and payment systems, e-identification and trust services and card payments.

___________________________________________________________________________________________

ANTONELLA VANARA – Account Manager Expert, International Division – SIA

ANTONELLA VANARA – Account Manager Expert, International Division – SIA

After graduating in Economical studies from University of Turin, she began her professional carrier at former San Paolo Torino Bank (now Banca Intesa Sanpaolo) within the IT department. In 1990 she joined SIA, where she worked as project specialist on interbank procedures automation.

Since the beginning of 2000, she has been working on the development and marketing of electronic and mobile payments projects, advancing her career positions in the company managing the launch of SEPA initiatives, online banking epayment services as MyBank and digitalization programs for major financial institutions. Currently Antonella Vanara works within the International Division, focusing on business development of new electronic payments solutions at European level.

___________________________________________________________________________________________

DIMITRIOS GORANITIS – Dimitrios is Financial Services Industry Risk and Regulatory Advisory Partner in Deloitte Romania. Dimitrios is leading Deloitte’s risk service offering in Central Europe focusing on banking regulatory strategy and supervision and credit risk transformation. Dimitrios held leading banking risk advisory positions with Deloitte and other Big 4 companies in South and East Europe. Prior to that Dimitrios held senior positions with UBS and JP Morgan in New York.

DIMITRIOS GORANITIS – Dimitrios is Financial Services Industry Risk and Regulatory Advisory Partner in Deloitte Romania. Dimitrios is leading Deloitte’s risk service offering in Central Europe focusing on banking regulatory strategy and supervision and credit risk transformation. Dimitrios held leading banking risk advisory positions with Deloitte and other Big 4 companies in South and East Europe. Prior to that Dimitrios held senior positions with UBS and JP Morgan in New York.

He has had extensive experience with national and supranational regulators including US Federal Bank, ECB, SSM, ESM, ESMA, EBRD and local regulators in UK, Belgium, Greece, Cyprus, Ireland, Portugal, Malta, Bulgaria, Slovenia, Romania, UAE, Kazakhstan etc. Dimitrios has supported a number of lenders in regulatory strategy and transformation initiatives as expressed not only in European Law (CRD/CRR) but also in suggested guidelines by EBA/ESMA in the Banking Union and in the greater EU. Indicative banking clients include Erste, Eurobank, Bawag, Banif, HSBC, Deutsche Bank etc.

Dimitrios is a member of Deloitte’s Banking Union Center in Frankfurt and member of Deloitte’s European Center of Regulatory Strategy. Both teams of senior professionals facilitate the ongoing regulatory discussion that Deloitte maintains with ECB, EBA and Basel and enable all members to identify best practices across Europe. Dimitrios holds a BA in Banking and Finance from University of Piraeus (Greece) and an MBA from Pace University New York (USA).

__________________________________________________________________________________________

Mr. BOGDAN PANDELICA – president of National Authority for Consumer Protection

Mr. BOGDAN PANDELICA – president of National Authority for Consumer Protection

He graduated from the Polytechnic Institute of Bucharest in 1992, where he majored in engineering, and the University of Pitesti in 2004 – economist with bachelor’s degree and master in management consulting. Between 2001 – 2009 he held management positions in several private companies (commercial director at Romlux Targoviste, Management Consultant at Trading Mentor-Pitesti and CEO of Erste Automobile Pitesti).

Between 2013 and 2015 he was employed in the Ministry of Economy where he held the positions of deputy secretary of state and later Secretary of State with responsibility for Foreign Trade and International Relations. From November 2015 to the second mandate as head of NACP, first led this institution between January and September 2009.

___________________________________________________________________________________________

Mr BOGDAN CHIRITOIU – president of Competition Council

Mr BOGDAN CHIRITOIU – president of Competition Council

Graduated from the Faculty of Medicine Carol Davila 1995, has accumulated a wealth of experience both as a professor and as an economic analyst. Mr Chiritoiu graduated of the Academy of Economic Studies in 2008 with a major in international public relations.

It has nine years of teaching activity in higher education, 11 years advising public policy and 10 years in the field of economic analysis.

Between 2005 and 2008, it was – State Counselor – Presidential Administration, Department of Economic and Social Policies. Also, for almost five years (2005-2009) served as Head of the Romanian delegation – Economic Policy Committee of the European Union. He has been serving as president of the Competition Council since May 2009.

___________________________________________________________________________________________

Mrs RUXANDRA AVRAM was born and educated in Bucharest. She has a degree in Finance and Accounting from Bucharest University of Economic Studies. She is a long standing professional with almost three decades in the Central Bank, especially in payments area, currently focusing on a new core function of a modern central bank, namely oversight activity.

For nine years Mrs Avram worked as coordinator of the Division of Regulation, Authorization and Oversight of Payment and Securities Settlement Systems.

At present, Mrs Avram is the Head of Market Infrastructures Oversight Department at National Bank of Romania. In this new role, Mrs Avram is mainly responsible for: Implementation of the relevant European Directives applicable in the payments field ; Regulations on payment instruments; Authorization of payment systems and securities settlement systems; Ongoing oversight of payment systems and securities settlement systems; Collecting information and statistical data regarding payments and payment instruments; Monitoring business continuity planning of payment service providers and payment system operators.

As representative of Central Bank, Mrs Avram is also an active participant/member within some structures developed at European Central Banks (ECB) level relevant for the payments field.

__________________________________________________________________________________________

Mr. FLORIN DANESCU graduated from the Executive MBA (EMBA) at the WU Executive Academy – The Vienna University of Economics and Business.

Mr. FLORIN DANESCU graduated from the Executive MBA (EMBA) at the WU Executive Academy – The Vienna University of Economics and Business.

He became a member of the Romanian International Bank S.A. team in January 2000, holding the position of Head of Treasury Division. Later his career at a steady rate, it successively occupying positions of Executive Vice President, First Executive Vice President and in 2008 was appointed CEO and chairman.

Since December 2011 he has been serving as Executive President of the Romanian Banking Association.

_________________________________________________________________________________________

CLAUDIA CHIPER is a counsel with Wolf Theiss and specialized in banking, finance, and capital markets. With more than 13 yaers of experience in the legal field, Claudia is the coordinator of the banking and finance practice at Wolf Theiss Bucharest office.

CLAUDIA CHIPER is a counsel with Wolf Theiss and specialized in banking, finance, and capital markets. With more than 13 yaers of experience in the legal field, Claudia is the coordinator of the banking and finance practice at Wolf Theiss Bucharest office.

Highly praised by clients, Claudia has extensive experience in dealing with and coordinating finance transactions as well as advising international and domestic credit institutions, financial companies and corporations in relation to regulatory aspects of Romanian law, and capital markets law.

Claudia is a member of the Bucharest Bar Association and, in addition to a Romanian law degree, she holds an LLM degree awarded by Queen Mary University of London.

__________________________________________________________________________________________

MARTEN NELSON is co-founder and VP of Marketing at Token, a Silicon Valley based technology company, focused on building a global open banking platform that addresses PSD2 and helps bank generate new revenues. Marten is a technology entrepreneur/executive who has been getting things done in startups and Fortune 100 software companies for over 20 years.

MARTEN NELSON is co-founder and VP of Marketing at Token, a Silicon Valley based technology company, focused on building a global open banking platform that addresses PSD2 and helps bank generate new revenues. Marten is a technology entrepreneur/executive who has been getting things done in startups and Fortune 100 software companies for over 20 years.

His experience spans Product Development, Business Strategy, Business Development and Marketing. Token is his third company to found. Abaca, a leading email security company was sold to Proofpoint and the edtech LearnCentral was sold to Blackboard.

„I’ve built focused and dedicated teams, created new markets and penetrated competitive ones. I’m skilled in entrepreneurship, business planning, product development, product management, product marketing, business development and customer engagement.

I am an expert at developing ideas and converting them into successful products and businesses. I have learned to manage cross-functional teams, build partnerships, develop and implement business processes and develop high quality employees. Best of all – I’m getting better at all this every day. Learning never ends.”

__________________________________________________________________________________________

Mr. ANDREI BURZ PINZARU is the Global Leader of Deloitte Legal Banking & Securities group and Central Europe Leader of Deloitte Legal. He has overall 18 years multidisciplinary advisory experience in Banking, Capital Markets and M&A and prior to becoming a lawyer he was for several years a licensed securities broker and advisor on capital markets, banking and M&A transactions.

Mr. ANDREI BURZ PINZARU is the Global Leader of Deloitte Legal Banking & Securities group and Central Europe Leader of Deloitte Legal. He has overall 18 years multidisciplinary advisory experience in Banking, Capital Markets and M&A and prior to becoming a lawyer he was for several years a licensed securities broker and advisor on capital markets, banking and M&A transactions.

Andrei worked on loan and security documentation in bilateral / syndicated loans, LMBOs, debt restructuring & loan workouts, loan transfers (local and cross-border, true sale and synthetic, performing and NPLs) and advised on several securitization structures. He also assisted in relation to the cross-border application of banking resolution laws.

He assisted in M&A deals in various industries. In FSI assisted in acquisitions of banks, insurance companies, non-banking financial institutions. In terms of regulations, he assisted banks, non-banking financial institutions, insurance companies, fund management companies, publicly traded companies on various financial / securities regulatory matters.

Andrei contributed to the drafting of Romanian Mortgage Lending Law, Mortgage Bonds and Securitization laws and coordinated the international team, which assisted Romanian Securities Commission (CNVM) in drafting the securities regulations for securitization instruments and mortgage bonds.

_________________________________________________________________________________________

WORKSHOPS

TOKEN – Founded in 2015, Token is a technology company headquartered in San Francisco with offices in London. Token’s open banking platform helps banks quickly and cost effectively meet the PSD2 compliance requirements and generate new revenue. It raises security and reduces disintermediation. Token has developed an open banking platform with rich functionality that allows banks to quickly and cost-effectively comply with PSD2 before the deadline. Unlike in-house developed solutions, Token supports the same API across all banks. Banks that use Token will have access to the most third-parties’ applications. This in turn means greater revenue for those banks.

SIA S.p.A. – SIA is European leader in the design, creation and management of technology infrastructures and services for Financial Institutions, Central Banks, Corporates and Public Administration bodies, in the areas of payments, cards, network services and capital markets. SIA Group provides its services in over 40 countries, and also operates through its subsidiaries in Austria, Germany, Romania, Hungary and South Africa.

The company also has branches in Belgium and the Netherlands, and representation offices in the UK and Poland. In 2015, SIA managed 9.9 billion clearing transactions, 3.3 billion card transactions, 2.8 billion payments, 41.7 billion financial transactions and carried 358 terabytes of data on the network. The Group is made up of nine companies: the parent SIA, the Italian companies Emmecom (innovative network applications), P4cards (card processing), Pi4Pay (advanced collection and payment services), TSP (front-end services), and Ubiq (innovative technology solutions for marketing), Perago in South Africa, PforCards in Austria and SIA Central Europe in Hungary. The Group, which currently has over 2,000 employees, closed 2015 with revenues of €449.4 million.

SIA has always been behind the European Financial Institutions and constantly been committed to delivering secure, reliable payment services based on its technology infrastructures (EBA STEP2 platform, TARGET2-Securities, 4-CentralBank-Network). Last but not least the EBA Pan-European IP Infrastructure.

The SIA Instant Payments service (https://www.sia.eu/en/

Be sure you won’t miss this exceptionally event! Reserve your place HERE!

CONTEXT

Revised by the European Parliament in October 2015, the new Directive on Payment Services (PSD2) is the latest in a series of legislation by the EU to enable modern, efficient, and inexpensive payment services. As European legislation, PSD2 is a requirement for all banks that operate in the European Economic Area and enforces an implementation deadline of January 2018. For those banks already progressing in their digital transformation, this is a reasonable timeframe to incorporate the necessary technology and business change. For those that have yet to embrace digital, key components of a digital infrastructure are needed and time is short.

The main impacts of PSD2

PSD2 has numerous new requirements, some impacting banks more than others, depending on the specific institution’s service portfolio and strategy. Three with the most significant impact include:

1. Strong authentification & secure communications

Strong Customer Authentification (SCA) is required in three situations: 1) online acces to the payment account, 2) initiation of electronic payment transactions, or 3) actions carried out via a remote channel that may imply a risk of fraud or other abuse. Exemptions might be considered based on the amount and/or recurrence of the transaction, the level of risk involved in the service provided and the channel used for executing the transaction. SCA is a two-factor authentification that requires independency and dynamic linking.

2. Third party provider regulation

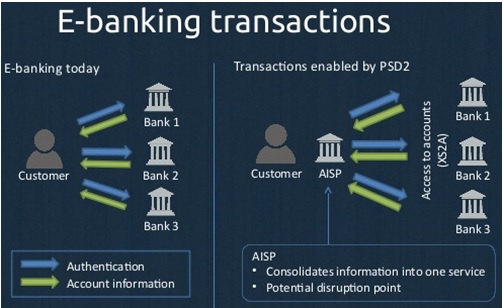

PSD2 extends the definition of Payment Institution by introducing new types of Payment Services Providers (PSPs). Credit institutions and electronic money institutions are considered Account Servicing Payment Service Providers (ASPSPs) that provide and maintain payment accounts. Third-party providers (TPP) that are also considered payment-services providers under the regulation include Payment Initiation Service Providers (PISPs) and Accoun Information Service Providers (AISPs) that act as aggregators of customers payment accounts information. PSD2 brings AISPs and PISPs in the scope of regulated entities.

3. Acces to payment account (XS2A)

Under PSD2 all registered PISPs and AISPs and alllicensed PSPs are to have access to payment accounts held at ASPSPs under explicit consent of the client. ASPSP must share all data enabling the AISP or PISP to perform the service requested by the client. PISP/AISP may not use, access or store any data for other purposes than provision of the requested service.

Be sure you won’t miss this exceptionally event! Reserve your place HERE!

The business risk PSD2 presents

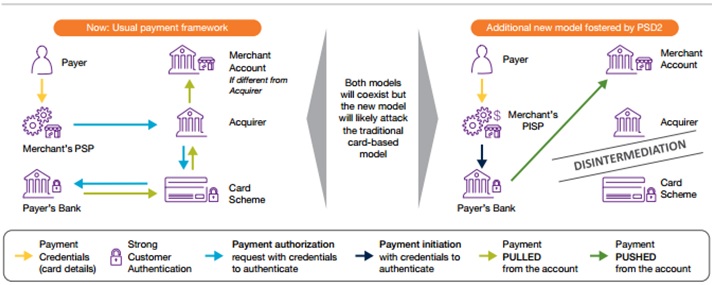

A main difference between PSD2 and PSD lies in the new requirements to provide third parties with “access to the account”. After PSD2 implementation, third parties can obtain access to customer accounts for account information and payment initiation services provided the consumer provides consent. This poses a security concern for banks to ensure that account access is controlled and authorized. It also poses a liability concern that, if something goes wrong in the customer’s service from the third party, the consumer may hold the bank liable. While these are important considerations as banks plan their PSD2 compliance, perhaps the biggest risk for banks is disintermediation.

Allowing third parties to access a customer account enables them to come between the bank and its customer, and strain the bank’s customer relationship. It also lowers the barriers to entry for third parties with new ideas for value-added services.

Today, third parties with innovative ideas are often unable to execute because they don’t have captive customers and banks are not willing to or even allowed to provide access to account information. PSD2 will make it easier for third parties to provide value-added services and grow viable businesses as banks will be required to provide access to customer data with permission.

PSD2 – How payments model will change (cards-based exampled)

FINAL CONSIDERATIONS

FINAL CONSIDERATIONS

Banks have no choice but to ensure they comply with PSD2. But, to help them remain relevant into the future, banks should look at PSD2 compliance as not only a requirement, but as an opportunity for value creation. Banks’ strategic options are plentiful if they think more broadly than just complying with PSD2. Through different collaboration models, banks can offer advanced payment and account information services, expand to services in other areas of banking and explicitly expand their service portfolio beyond traditional banking – all of which can lead to differentiation and new sources of revenues.

An open API platform strategy could be very helpfull, builds on the banks’ core strengths of trust and brand recognition and customer information assets. It also allows the bank to build on the stregths of non-banks innovators that are often more agile and fast-paced in innovation.

Be sure you won’t miss this exceptionally event! Reserve your place HERE!

MAIN PARTNER

BUSINESS PARTNERS

STRATEGIC PARTNERS

MEDIA PARTNERS

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: