![]()

![]()

Sweden may be about to take its world-beating cashlessness to the next level, as the pandemic threatens to push its notes and coins close to extinction, according to Bloomberg.

Stefan Ingves, the governor of the Riksbank, recently remarked that some young Swedes “have no idea” what real money looks like anymore. It’s a future that has Ingves and others worried, and he says lawmakers may need to step in before it’s too late.

It wasn’t always obvious that cashlessness could become a risk. Moving to digital transactions comes with plenty of benefits, including the kind of transparency that makes things like money laundering and tax evasion much harder to do. But Sweden seems to have crossed a crucial tipping point. If there’s no cash at all to fall back on, what happens if digital networks fail? And what about cyberattacks? Such events can do a lot more damage than old-fashioned bank robberies.

“If the lights go out, we need to have enough physical cash in this country, way, way out in the woods, so that we can revert to using physical cash if there’s a serious problem,” Ingves said.

Sweden is now trying to address the issue of cashlessness in the middle of a pandemic that’s made contact with cash a perceived health risk and, as a result, less popular than ever. The preferred method of payment these days is completely contactless, for maximum health safety.

Klarna AB, a Swedish bank, estimates that 73% of card payments by its customers are now contactless, up from 63% before the pandemic. “People don’t want to touch coins and bills” or “to press buttons,” said Viveka Soderback, consumer insights manager at Klarna. The coronavirus “has accelerated that trend.”

Sweden has less cash in circulation than anywhere else in the world, at around 1% of gross domestic product, according to the latest available data. That compares with 8% in the U.S. and more than 10% in the euro area. Of Swedes aged 18-34, roughly three-quarters never or rarely use cash, according to a July survey commissioned by Bankomat.

Ingves says the issue also raises “practical” questions about the role of a central bank. That’s why Sweden’s Riksbank has done more advanced planning than most of its peers to figure out how to stay relevant and how to ensure citizens don’t suddenly find themselves without access to real money.

“We need a definition of legal tender suited for the digital age,” he said in a recent speech, adding that the government will also need to draft legislation that requires banks and businesses “to maintain some form of a minimum capacity” to handle physical cash.

In 2017, the Riksbank started looking into the feasibility of issuing a digital currency. Earlier this year, it launched a pilot project to figure out what sort of technology is needed to enable a so-called e-krona.

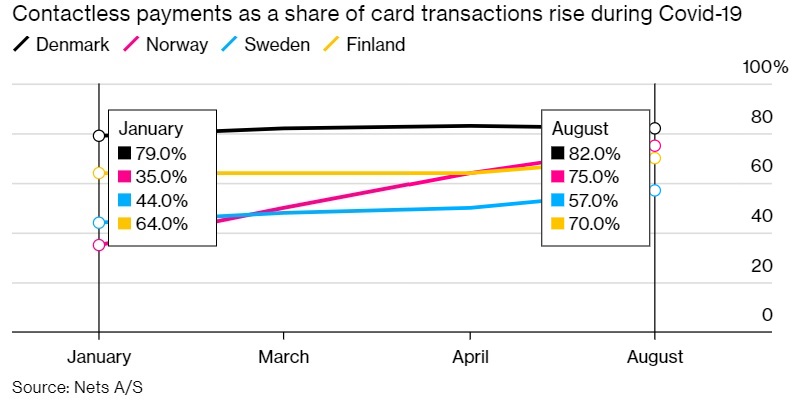

Contactless card payments have soared in the Nordic region, with tap-to-pay transactions up by 30% in Sweden and 114% in Norway from January to August, according to data compiled by card-service provider Nets A/S.

The trend can be seen worldwide. Globally, nearly 60% of Visa transactions outside the U.S. are done with a screen tap, according to the card company. In contrast, contactless transactions, including the near-field communication chips used by mobile payments services such as Apple Pay, have been little used in the U.S., Federal Reserve Bank of Philadelphia said in a report.

Meanwhile, one of the last bastions of cash – kids’ pocket money – is also dying out in Sweden. Only 16% of Swedish children get regular allowances in the form of actual bank notes and coins, a poll by Sifo found in June.

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: