article written by Marius Galdikas, CEO at ConnectPay

This year has been a rollercoaster for the payments industry, as it had to adapt to new challenges posed not only by the ever-changing needs of the consumer but by the pandemic as well. What trends and solutions are likely to thrive in 2021?

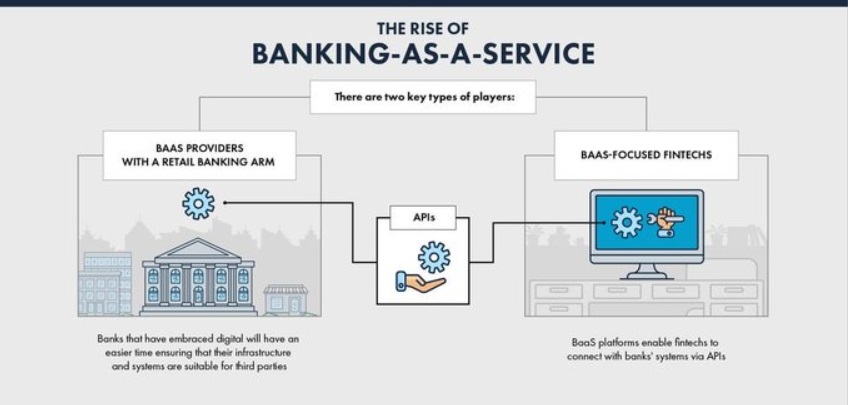

BaaS will continue gaining traction

Banking-as-a-service, or BaaS, offers the provision of banking processes, meaning, it allows to embed financial services into any company. Using BaaS enables to focus on product innovation, rather than infrastructure development, as the required banking stack can be integrated via API-driven platforms. Sometimes referred to as „embedded finance„, the service creates an opportunity for any tech company to become a fintech in a shortened timeframe.

Embedded finance paves the way for creating financial products, as companies do not have to start the process from scratch: build a banking infrastructure and only then start innovating. For some, BaaS is the only way they could start developing products in the first place, as laying the groundwork before that requires a solid investment. In both cases, BaaS allows to delegate a lot more resources towards product innovation. The interest in BaaS will continue to grow, as it could help tech companies to gain a significant advantage against their competitors.

Market players in-pursue of more regulation

Companies operating in under-regulated sectors have started to appeal to policy makers for increased regulation. A good example of the phenomena in the payments market is the crypto industry, which has voiced its concerns, hoping to receive clear and unified standards that would help them mitigate some of the market resistance.

Having a clearly defined regulatory framework would help industries, currently viewed as more ambiguous, to position themselves as reliable allies and pave the way for stronger partnerships with other market players. Not to mention it would help to diminish associations with fraudulent activities, reassuring current and potential clients.

He also noted that the drive towards stricter regulation is likely to arise from other industry players as well, which is a quite welcome change, as it could bring more harmony into the entire payments’ ecosystem.

Decreasing third-party reliance

Data breaches due to external vendor vulnerability, as well as a few widely escalated incidents that called into question their reliability in general, are forcing companies to re-think the risks of having third-party suppliers. This has encouraged payment providers to search for solutions that would help take matters into their own hands, e.g. move more operations in-house, and lessen dependency on any intermediaries.

Such incidents give an incentive to reconsider having third-party suppliers. Setting up capable in-house solutions allows to retain more transactional control and increase overall fund security, as fewer parties are involved in the payment process.

Enhanced use of biometrics

Using biometrics to confirm the buyer’s identity and approve transactions are among the rising trends in the market that are expected to evolve throughout the coming year.

For consumers, the option to approve purchases by face, palm, or fingerprints would allow avoiding password overload, as all payment services in-use could be secured by a single personal feature. It would make the entire process faster, too. Moreover, this provides an extra layer of security, as personal features are harder to replicate by scammers.

In addition, a recent study revealed that 56% of shoppers would prefer using a biometric sensor on their payment card instead of a PIN, hinting at the increasing appeal of such solutions for consumers as well.

Increasing payments flexibility

As consumers are unsure about what the future holds, market players are bending over backwards to mitigate their pandemic-related concerns, thus offering flexible solutions to better accommodate their expectations. This has led major market players, such as PayPal and Chase, to step into the new „buy now, pay later” market, which gives customers the option to pay off a purchase over a period of time with zero-interest and fixed-rate monthly installments.

The concept of flexibility encompasses not only delayed payment options but the rise of new payment platforms as well. For instance, WhatsApp, commonly known as a messaging app, is working on launching a payments service in India to increase inclusion in the digital economy, while Google is laying the groundwork for Plex – a mobile-first bank account integrated into GooglePay.

There is no doubt that consumer needs are constantly evolving. That said, the pandemic has greatly influenced which aspects have grown in importance throughout the past few months. Going cashless acted as a springboard for novel payment platforms, while future income worries encouraged providers to introduce pay-by-month model. With a fair amount of uncertainty expected to carry over to next year, this is only the beginning of novel solutions, designed to adapt to consumers’ changing habits.

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: