In a recent in-depth report on global stablecoins, the European Central Bank, or ECB, pushed for clear regulatory parameters for stablecoins, citing risks as well as gaps in current regulations.

„In order to reap the potential benefits of global stablecoins, a robust regulatory framework needs to be put in place in order to address these risks before such arrangements are allowed to operate,” the ECB wrote in its May 5 report.

One of the conclusions of the report is that „If a stablecoin arrangement reaches a global scale, its malfunctioning could pose risks to the financial system. In this context, the ECB studied Facebook’s Libra in its report, relating various numbers and metrics to different scenarios.

This section seeks to quantify the potential size of global stablecoin arrangements, using the Libra initiative as an example. Libra has been chosen as an example as it has the potential to grow quickly, due to network effects stemming from its global user base and the fact that Facebook and the other Libra sponsors are able to make significant resources available in order to support the launch of the stablecoin.

In order to quantify the potential size of the Libra ecosystem, we need to ascertain both the potential number of users and the average holdings per user. For the purposes of this analysis, the potential user base is considered to be the 2.4 billion users in the Facebook ecosystem (which also includes Instagram and WhatsApp, in addition to Facebook itself). Approximately 10% of those users (240 million) are located in the euro area.

In order to approximate the average holdings per Libra account, three different scenarios are considered. The first scenario represents a situation where Libra becomes a widespread means of payment. That scenario uses data on PayPal, as a well-established widely used electronic payment service provider. The PayPal user base currently consists of around 286 million active accounts with average holdings per account of €64.[13]

The two other scenarios aim to reflect a situation where Libra is also used as a store of value. These scenarios are based on data for Yu’E Bao (the MMF operated by Chinese company Ant Financial, which is part of the Alibaba Group), which had 588 million users in China in December 2018. According to Bloomberg (2019), assets under management in Yu’E Bao totalled CNY 1,030 billion in the first half of 2019, corresponding to €135 billion at market exchange rates and making Yu’E Bao one of the world’s largest MMFs.[14] This results in average holdings per capita of around €231, which is the second scenario under consideration (hereafter referred to as the “store of value A” scenario). In order to construct an extreme-case scenario, the peak value for Yu’E Bao’s assets under management (€254 billion in March 2018) is used. To take account of the difference between the income levels seen in China and Europe, purchasing power parity‑adjusted exchange rates are used. This produces average per capita holdings of around €1,220, which forms the basis for the third scenario under consideration (hereafter referred to as the “store of value B” scenario). Bloomberg (2019) notes that one important driver of the strong outflows from Yu’E Bao over the last two years has been increased regulatory pressure and scrutiny. The “store of value B” scenario may therefore be regarded as reflecting a situation where a global stablecoin arrangement remains largely unregulated. It is worth noting, in this regard, that Yu’E Bao has grown rapidly, taking just five years to establish its sizeable user base.

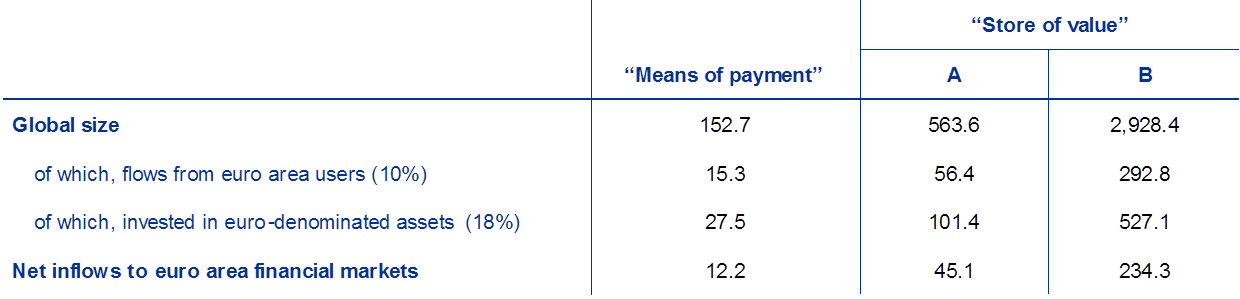

In the extreme-case scenario, the global size of the Libra Reserve could reach almost €3 trillion of assets under management. Table 1 shows the estimated global size of the Libra Reserve in each of the three scenarios. As the table indicates, the Libra Reserve’s total assets under management could range from €152.7 billion in the “means of payment” scenario to around €3 trillion if the currency becomes a widely adopted store of value. On the basis of the number of Facebook users in the euro area, around 10% of these total assets could stem from users in the euro area.

Table 1

The Libra Association’s potential global size and importance for the euro area

(EUR billions)

Source: ECB calculations.

The currency composition of the Libra Reserve could result in inflows to euro area short-term funding markets. The Libra Association has announced that funds collected will be invested in a currency basket comprising US dollars (50%), euro (18%), yen (14%), pounds sterling (11%) and Singapore dollars (7%). The euro’s share of Libra’s currency basket is thus larger than the euro area’s share of total Facebook users (18% versus 10%). Assuming that the average holdings per user are distributed roughly equally across geographical areas, this implies a currency mismatch between flows from European users to the Libra Reserve in euro and euro‑denominated assets held by the Reserve. In the three scenarios under consideration, this would result in additional inflows to euro area short-term funding markets from the rest of the world totalling €12.2 billion, €45.1 billion and €234.3 billion respectively (see Table 1). Depending on the scale and speed of adoption, these inflows could potentially have a limited impact on euro exchange rates. If there are additional versions of Libra, each backed by only one fiat currency (EUR-Libra backed by euro only, USD-Libra backed by US dollars only, etc.), flows between euro area short-term funding markets and the rest of the world would be determined by the relative usage of the different versions of Libra inside and outside the euro area.[15]

Libra could potentially become one of Europe’s largest MMFs. According to the Libra Association, assets under management will be invested in high‑quality highly liquid assets, such as top-rated short-term government bonds, bank deposits and cash. Thus, there are a number of similarities with MMFs. Euro area MMFs held euro‑denominated assets totalling around €600 billion in the third quarter of 2019. The Libra Reserve has the potential, therefore, to become one of the largest MMFs in the euro area. Chart 1 looks at the size of the Libra Reserve in the three scenarios under consideration, comparing it with Europe’s three largest MMFs.

Chart 1

Potential size of the Libra Reserve relative to the largest European MMFs in terms of euro-denominated assets

(EUR billions)

Sources: Fitch (2019) and ECB calculations.

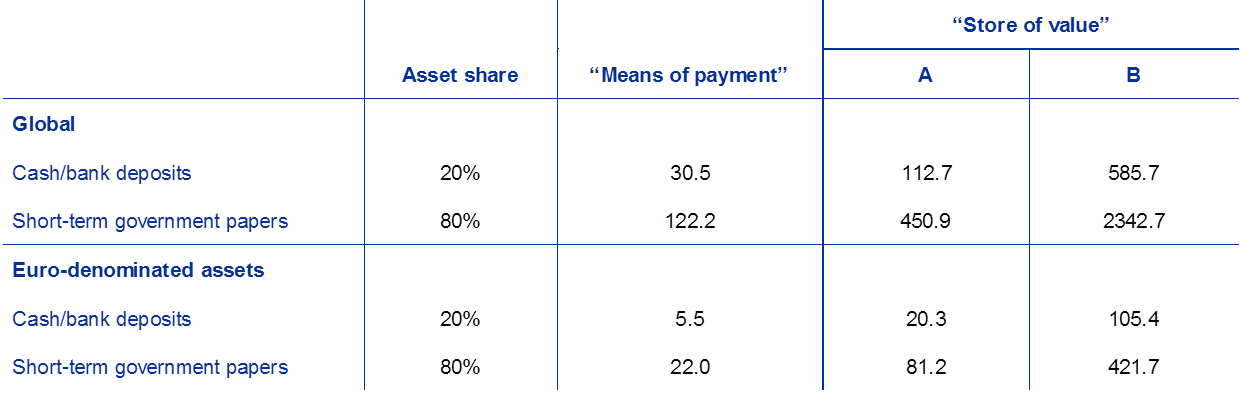

The Libra Reserve could become an important investor in highly rated short-term government papers, thereby potentially contributing to the scarcity of safe assets in the euro area. The Libra Association (2020) declared that at least 80% of the Libra Reserve shall be invested in short-term government debt securities with a residual maturity of less than three months and high credit ratings. The latter was defined as a rating equal to or above A+ from S&P. The remaining up to 20% of the reserve were announced to be held in cash or invested in money market funds. Table 2 shows the size of the Libra Reserve’s investment into the different asset classes for the three scenarios. At year-end 2019, the total value of general government debt of euro area countries rated A+ or above with a maturity of less than three months stood at €268.8 billion. In the “store of value A” scenario, the Libra Reserve would, accordingly, hold around 30% of these short-term government papers by value, while the total amount invested under the “store of value B” scenario would exceed the total value of the entire market segment. Consequently, the scarcity of safe assets (e.g. for collateral purposes) could increase significantly in the euro area.[16] Depending on the growth of the Libra Reserve, the credit quality requirements may need to be weakened. Alternatively, the asset composition may need to be shifted towards other asset classes, typically to be found in the portfolios of constant net asset value (CNAV) money market funds, such as commercial papers, term deposits or certificates of deposits.

Table 2

Potential composition of the Libra Reserve’s asset holdings

(EUR billions)

Notes: Asset composition as proposed by Libra Association (2020).

Sources: ECB and ECB calculations.

The investment policy of the Libra Association could lead to some stable retail deposits being transformed to less stable wholesale financing in the euro area banking system. Up to 20% of the reserve will be held in cash or invested in money market funds according to the Libra Association. In this way, these reserves are likely to provide financing for the banking system. Total bank deposits held with euro area monetary financial institutions stood at €13.2 trillion in November 2019. Of that, €7.7 trillion stemmed from the household sector, and €4.3 trillion was held in current accounts or took the form of overnight deposits. Most inflows to the Libra Reserve are expected to stem from retail depositors, who can be approximated by the household sector. Compared to these numbers, the impact of Libra is likely to remain limited, though. Under the extreme-case “store of value B” scenario in Table 2, 2.4% of euro area households’ current account and overnight bank deposits would be replaced with wholesale funding. This number could be seen as a lower bound given the considerations above that short-term government debt markets may not be able to absorb 80% of the Libra Reserve under this scenario. As retail deposits are considered to be the most stable form of bank financing, this could affect the stability of the funding profiles of individual banks. It could also result in a redistribution of deposits across the euro area banking system. While outflows of retail deposits could affect all banks relatively equally, higher-rated banks could profit more strongly, as the Libra Association has announced that it will only invest in assets of highly rated institutions.

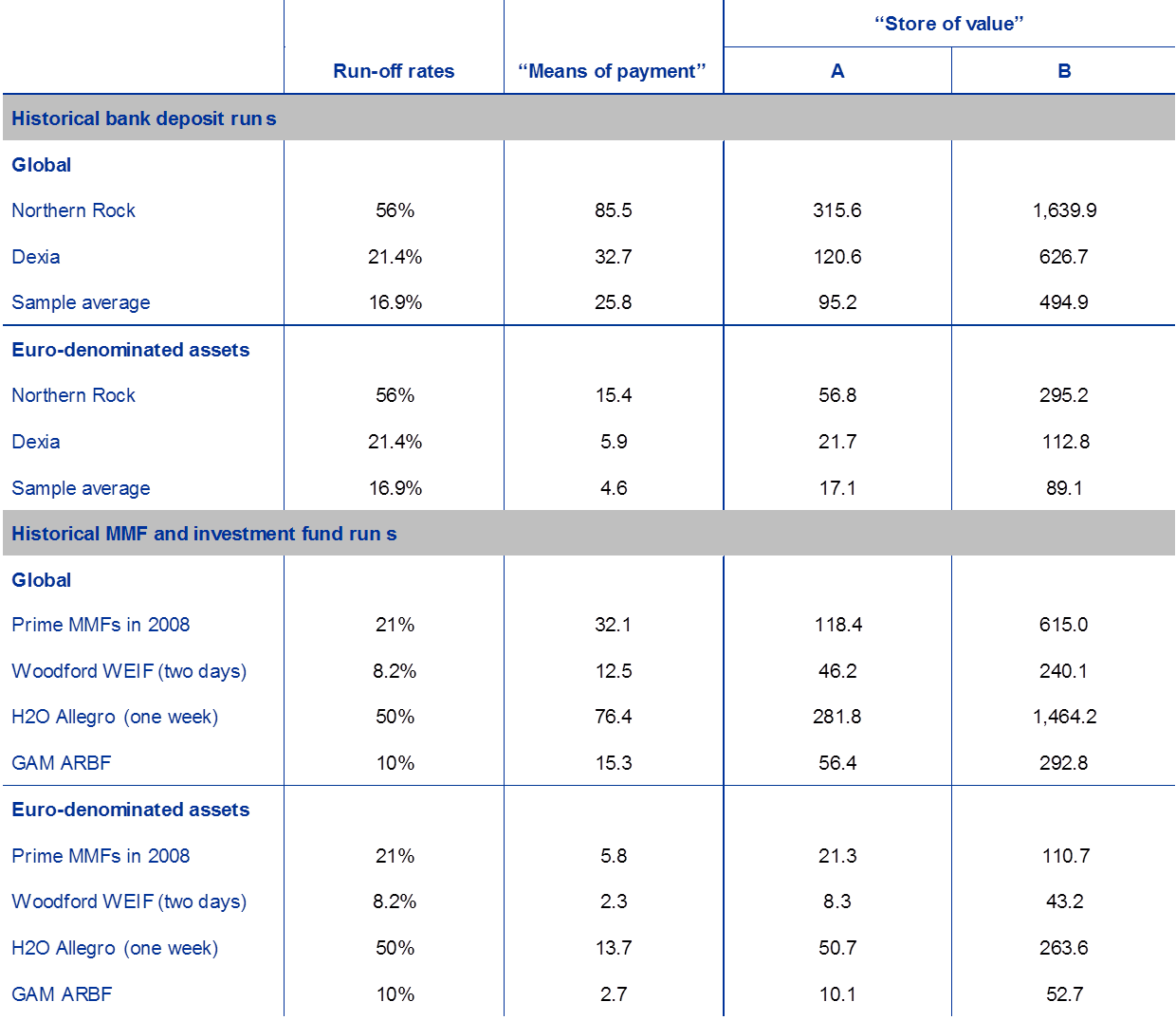

Table 3

Potential Libra outflows under historical bank deposit, MMF and investment fund run scenarios

(EUR billions)

Notes: All bank run-off rates were realised over a period of one month. The sample average for bank runs relates to a sample of ten recent deposit runs in Europe and North America. All investment fund runs took place in the first half of 2019.

Sources: HM Treasury (2009), McCabe (2010), FCA, Bloomberg, Morningstar and ECB calculations.

The implications that abrupt outflows from the Libra Reserve would have for euro area short-term funding markets can be assessed on the basis of historical bank and fund runs. Table 3 shows potential outflows from the Libra Reserve under various shock scenarios, which are based on bank deposit, MMF and investment fund runs observed in the recent past. In order to gauge the potential financial stability implications of widespread use of Libra, these possible outflows need to be considered in the context of the size of short-term funding markets and potential regulatory requirements.

The significant amounts of highly liquid assets that the Libra Reserve would have to hold if it was subject to European regulation on MMFs would increase its resilience in stressed outflow scenarios. Rules on CNAV funds require European MMFs to hold significant liquidity reserves for the case of abrupt outflow shocks. Specifically, MMFs’ liquidity reserves must be sufficient to cater for overnight outflows totalling 10% of their assets and outflows totalling 30% of their assets over the course of a week. Eligible reserves include cash holdings, reverse repo transactions, and sovereign, supranational and agency debt with a residual maturity of up to 190 days. Such liquidity buffers would place restrictions on the types of asset that the Libra Reserve could hold. At the same time, these buffers would allow the Libra Reserve to withstand the majority of the outflow scenarios shown in Table 3, showing the added value that MMF regulation have for global stablecoins in such scenarios.

An outflow shock affecting the Libra Reserve could pose challenges and risks to global and euro area financial markets. The results in Table 3 show that outflows from the Libra Reserve could be significant in the presence of the kinds of run scenarios that have been seen in the banking and fund sectors. If it was governed by the MMF Regulation (MMFR), the Libra Reserve might be able to cover all redemptions by liquidating its most liquid assets. The sudden offloading of such large amounts of assets would, however, have ramifications that could affect market liquidity and asset prices, potentially resulting in funding difficulties for governments and banks that the Libra Reserve had invested in. The Libra Reserve could also react by suspending redemptions of Libra coins.[17] The consequences of a global fund and payment system adopting such a course of action fall outside the scope of this article, but will need to be investigated carefully.

[13]See Wall Street Journal (2016) for a discussion of PayPal’s role in the financial system.

[14]See Fitch (2017) for a detailed description of the Yu’E Bao money market fund.

[15]The second version of Libra’s white paper (see the Libra Association, 2020) proposes the introduction of single-currency Libra stablecoins in addition to the multi-currency stablecoin that was announced previously. It is proposed that the multi-currency coins shall constitute an aggregation of separate single-currency coins with fixed nominal weights of, among others, 50% for a USD-backed coin and 18% of a euro-backed coin.

[16]A significant share of this sovereign debt market segment currently trades at negative yields, making it challenging to maintain a full backing of all outstanding Libra coins by the reserve without the collection of further revenues, for example in the form of fees from users.

[17]In fact, in response to its interactions with central banks and supervisory authorities, the Libra Association (2020) proposed policy tools that are commonly used to contain runs on investment funds, such as redemption notice periods and early redemption haircuts.

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: