European Central Bank investigates use of distributed ledger but warns of far-reaching consequences

The European Central Bank is looking into the use of distributed ledger technology (DLT) for the Eurosystem’s market infrastructure but is wary of the far-reaching consequences for the role of central bank money, says executive board member Yves Mersch.

The Eurosystem’s financial market infrastructure for payments and securities is undergoing a major overhaul. The Target2 (T2) real-time gross settlement system for the euro, developed in the 1990s, is set for a revamp thanks to a shared gateway with the newer Target2-Securities (T2S) platform, new services and instant retail payments.

In a speech, Mersch says that DLT is one of „several possibilities” being explored for these projects but adds that „even if, ultimately, DLT emerged as technically superior in terms of safety and efficiency, we will also have to reflect on the wider implications of the use of this technology for the role of central bank money”.

This is because if T2 and T2S are moved to DLT a decision will have to be made on who and what can access central bank money on the ledger. Access to the ledger for payments and securities settlement could be restricted to banks, or to banks and market infrastructure providers such as central securities depositories, or perhaps extended to central counterparties and automated clearing houses.

„But why stop here?” asks Mersch, suggesting that payment service providers and even individuals could access central bank digital currency on the ledger via their bank accounts. More ambitious still, individuals could decide to cut out their banks and hold their digital money at the ECB.

This could have a huge impact on the commercial banking sector. Asks Mersch: „How would this affect the bank’s ability to give loans? How will the monetary transmission mechanism work and the economy at large if the basic business model of many banks could be impaired?”

And the potential impacts would not only be on banks: „What is the impact of central bank digital currency on physical cash? What would be the impact on central bank seigniorage? How would market participants change their investment strategies and business models? Would there be any implication on the integration of the European capital market, financial inclusion, and economic growth?”

Mersch is steering an organisational structure for analytical work on technological innovation in the financial sector and says that this will look not only at the practical aspects of using DLT but also things such as the implications of the issuance of central bank digital money.

„We have a lot of more thinking to do,” he says.

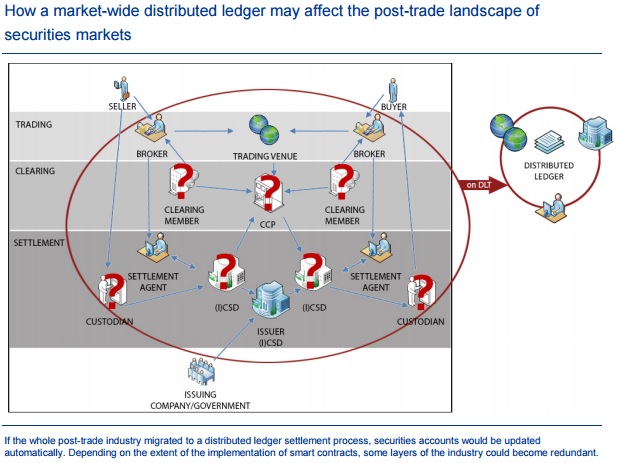

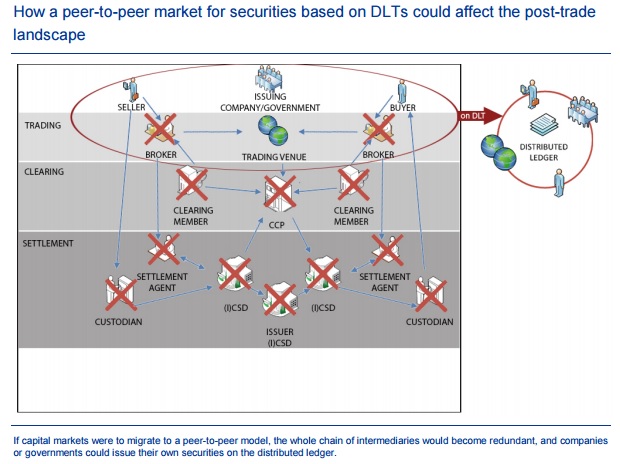

As part of its work, Mersch’s team has just published a paper on distributed ledger technologies in securities post-trading. Written by economists Andrea Pinna and Wiebe Ruttenberg, the paper concludes that while DLT has „potential” it faces a number of potential barriers: the technology is not mature; legal and governance issues have yet to be clarified; and even were DLTs to be adopted widely, certain post-trade functions will continue to be necessary.

„It is not yet, therefore, clear whether DLTs will cause a major change in mainstream financial markets or whether their use will remain limited to particular niches. It is possible that a DLT may find its way into the mainstream market, but should this happen, it is more likely to cause a gradual change in processes, rather than a revolution in the market.”

Read the full paper: Distributed ledger technologies in securities post-trading (1.5 mb – pdf file)

Source: finextra.com

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: