Digital banking report: „Banks must be prepared to meet the 24/7 needs of digital banking customers and may risk their reputation if they are not”

New research from Fiserv looks at changing trends in the U.K. banking sector and the ways in which digitalisation is set to impact consumers’ banking behaviour over the next five years. The total value being moved through mobile banking apps is expected to double by 2020, increasing from £1.7 billion to £3.4 billion a week. The amount of money being sent per week via online banking is forecast to increase from £6.4 billion in 2014 to £9.4 billion by 2020

The number of mobile banking users is set to almost double from 17.8 million to 32.6 million by 2020, whilst the number of U.K. adults using online banking will increase from 27.7 million to over 35 million, according to a report commissioned by Fiserv, Inc., a leading global provider of financial services technology solutions. Future Trends in U.K. Banking, compiled by the Centre for Economics and Business Research (Cebr), also forecasts that this combined growth will see more money being transferred through digital channels, rising to £3.4 billion a week via mobile banking apps and £9.4 billion a week via online banking, totalling £12.8 billion a week.

Mobile Banking

Currently, just over a third (34 percent) of U.K. adults are estimated to be banking on their mobile. With the increasingly widespread ownership of smartphones and a growing appetite amongst U.K. adults to access their finances on-the-go, this figure is expected to almost double to 60 percent by 2020. This projected increase of 14.8 million more mobile banking users over the next half-decade represents a significant opportunity for challenger banks to bring their innovative business models to the market and for existing banks to add digital services to cater to this future majority.

With the emergence of more high-tech features such as remote cheque capture and apps such as PayM, a wide range of mobile banking functions like checking your balance or conducting transfers are all expected to grow in popularity over the next five years. The total value of transactions being moved through mobile banking apps is expected to double by 2020 to £3.4 billion a week.

„The technological developments allowing for the recent surge in digital banking are also enabling banks and new entrants to reach potential customers more quickly and cost effectively than ever before,” said Travers Clarke-Walker, Chief Marketing Officer, International Group, Fiserv. „Banks must be prepared to meet the 24/7 needs of digital banking customers and may risk their reputation if they are not. Still, the advantages for banks to increase their digital capabilities are clear. There’s more and better engagement with customers, which in the long term can lead to greater customer loyalty and uptake of products. Most banks would recognise that engagement is born out of the quality of the customer experience. So if you give customers great experiences, particularly in their mobile banking services, their engagement tends to be higher.”

Online Banking

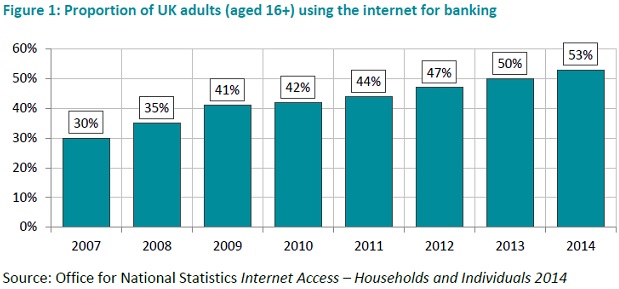

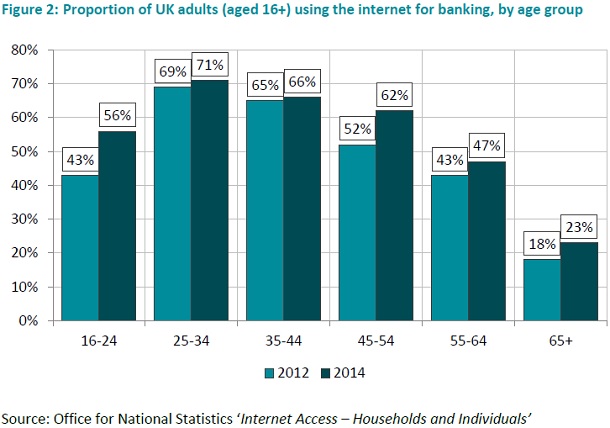

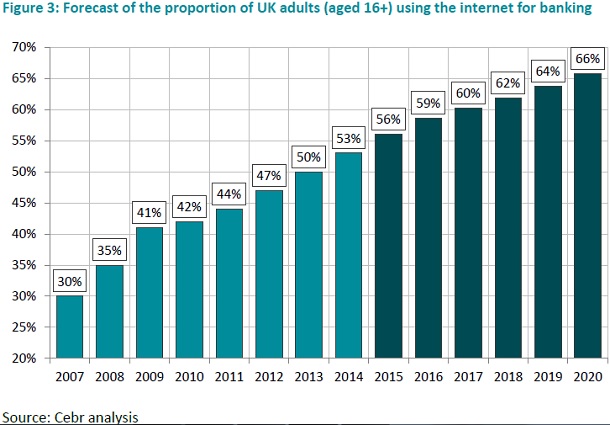

U.K. online banking use is projected to rise significantly by the end of the decade, from 53 percent of Brits in 2014 to 66 percent by 2020. While younger age groups, particularly those between the ages of 25 and 34, are currently more likely to bank online, all age groups have seen a rise in the prevalence of online banking over the past two years. These increases have been driven by a consumer need to access information faster and on-the-go. Looking ahead, this upward trend is forecast to continue as younger users who are already doing online banking enter a new age bracket by 2020.

The number of U.K. adults using online banking is forecast to increase to over 35 million by 2020, up from 27.7 million in 2014.

This upward trend in online banking usage, combined with inflation and a stronger economy, suggests that by 2020, as much as £9.4 billion could be moved through online banking per week.

Clarke-Walker added, „Bank’s digital offerings have become increasingly important for consumers, and with footfall in branches falling by roughly 10 percent a year, this trend looks set to continue through 2020. There are a number of companies, especially in different sectors such as retail, which use more advanced digital services to differentiate themselves. The banking industry lags behind when it comes to using such customer- centric technology, but it doesn’t need to be this way. Banks have the ability to transform the future financial services experience with online and mobile offerings. Capabilities like mobile alerts, instant payments, and location-based services, coupled with data and analytics used with customers’ permission, offer a significant advantage if used effectively.”

Research conducted by the Cebr from 12 – 29 November 2014, using a combination of desk research and external research conducted by Opinium Research from 2 – 3 September 2014, amongst 2,003 U.K. adults (aged 18 and over) via an online omnibus survey. Results have been weighted to nationally representative criteria.

Pentru mai multe detalii dscarcati raportul Cebr aici: Future trends in UK_Banking

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: