Confidence in service providers critical to open banking adoption – study

Survey confirms that banks are preferred suppliers of open banking services, but must fight to maintain position as TPPs evolve the category.

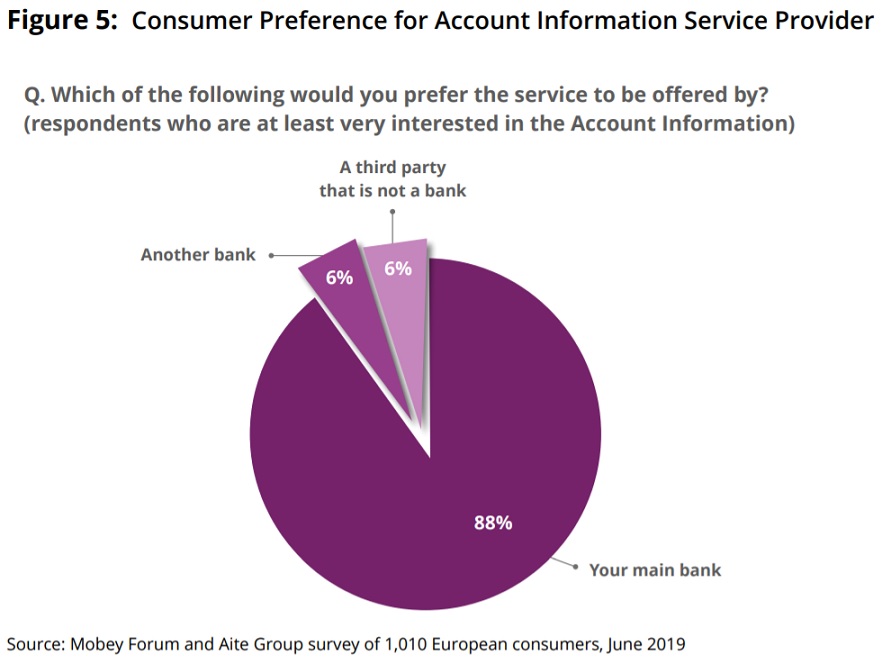

The overwhelming majority of consumers would prefer their main bank, as opposed to other banks or third-party providers (TPPs), to be their primary source of open banking services, a new pan-European study from Mobey Forum and Aite Group has revealed.

The report, entitled ‘Open Banking: Open Minds? Consumer appetites for open banking services’, draws on a online quantitative survey of over 1000 consumers in Finland, France, Germany, Spain, and the United Kingdom. Conducted in June 2019 by Aite Group, the survey highlights the opportunity for banks to create new open banking services and emphasises that the window during which consumers are hesitant to share account data with other banks and TPPs will close as the category quickly evolves.

“It’s crucial that banks act on their short-term advantage quickly to avoid disintermediation by TPPs as the open banking market evolves,” comments Elina Mattila, Executive Director, Mobey Forum.

“Consumers trust their banks because no-one else does data security and privacy like they do – it’s a cornerstone of their success. Consumer confidence in third party banking services, however, continues to grow. Open banking is the next chapter in the digitalisation story and a new generation of agile, specialist TPPs is forming to capitalise on API-based payment and data services. If banks want to protect their place at the forefront of the industry they need to act now, either to offer TPP services under their own brands, or to create their own. Either way, they need to move before the TPPs can establish an independent base.”

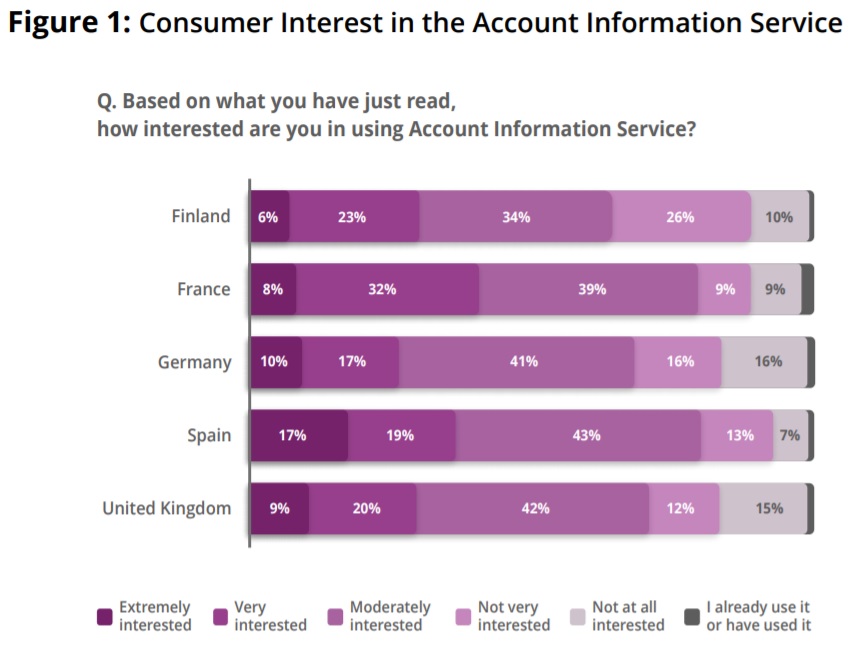

Despite open banking’s infancy, the study reveals that already approximately one third of consumers are either ‘very interested’ or ‘extremely interested’ in five open banking enabled use-cases: account information services (32%), pay by bank (33%), purchase financing (25%), product comparison (35%), and identity check (35%).

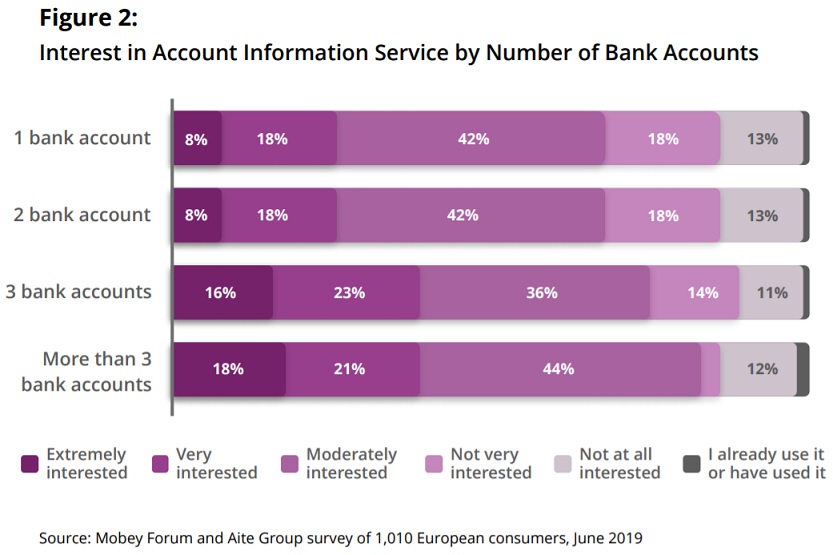

These results were largely consistent across all the five countries surveyed, with some small differences: in Spain and France those with more banking relationships were slightly more interested in account aggregation, while those in Germany and Finland with more banking relationships were slightly less interested in account aggregation that the average for all countries.

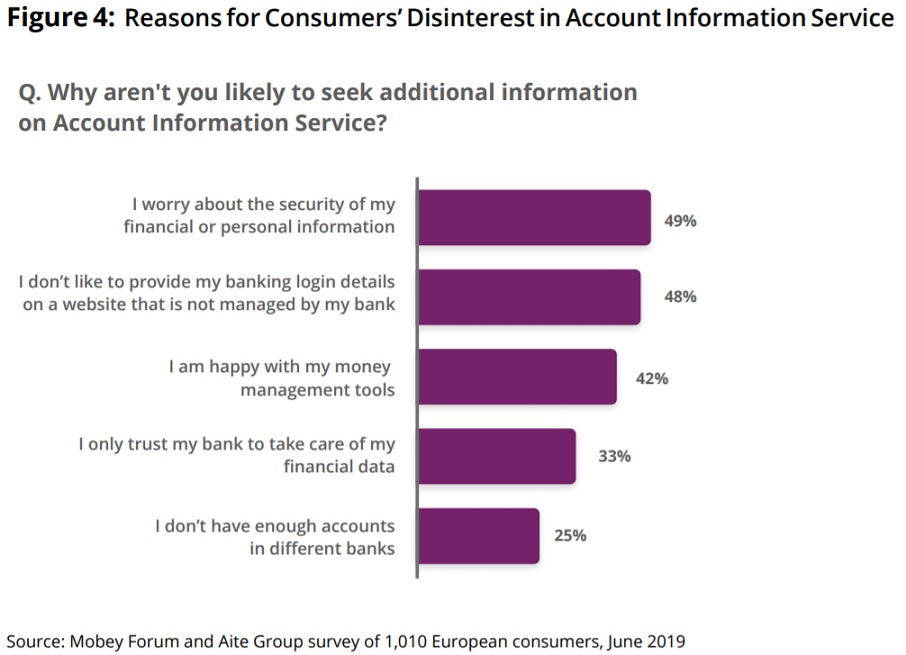

Security and privacy, however, are cited as the main factors inhibiting adoption among those consumers expressing concerns. The report contends that banks should pay strong attention to these differentiating factors when launching open banking services, as competition for consumer trust increases.

The report also explores under which circumstances consumers might be willing to deprioritise trust and, instead, favour convenience and usability. When questioned over their willingness to adopt a new payment method, for example, 91% respondents indicated that they could be tempted to switch either by financial incentives or the promise of greater convenience.

“Trust alone is not enough,” adds Mario Brkic, co-chair of Mobey Forum’s Open Banking Expert Group, George Labs. “Banks must also focus on developing services with convenience and usability in mind. People are already willing to give huge amounts of their personal and financial information to brands like Google, Amazon, Facebook and Apple. When the services deliver real value, they are ready to share data. Many open banking TPPs can respond to consumer demand faster than traditional banks can, so the race is on. The real winners in open banking will be those that can provide superior customer experiences under a trusted brand.”

Open Banking: Open Minds? Consumer appetites for open banking services provides banks and other financial services stakeholders with a market view on consumer appetites toward new open banking services and explores the possible roadblocks to consumer adoption.

Mobey Forum is the global industry association empowering banks and other financial institutions to shape the future of digital financial services.

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: