Driven by changing user demands and technological advancements, digital payments, and fast payments in particular, have been on the rise for years. Yet cash has continued to play an important role as a means of payment.

„While cash in circulation continued to decrease in many jurisdictions in 2023, the demand for cash withdrawals generally remained stable compared with previous years. This suggests that there is still a considerable demand for cash in making payments.” – according to a BIS Working Paper called „And so we pay: more digital and faster, with cash still in play”.

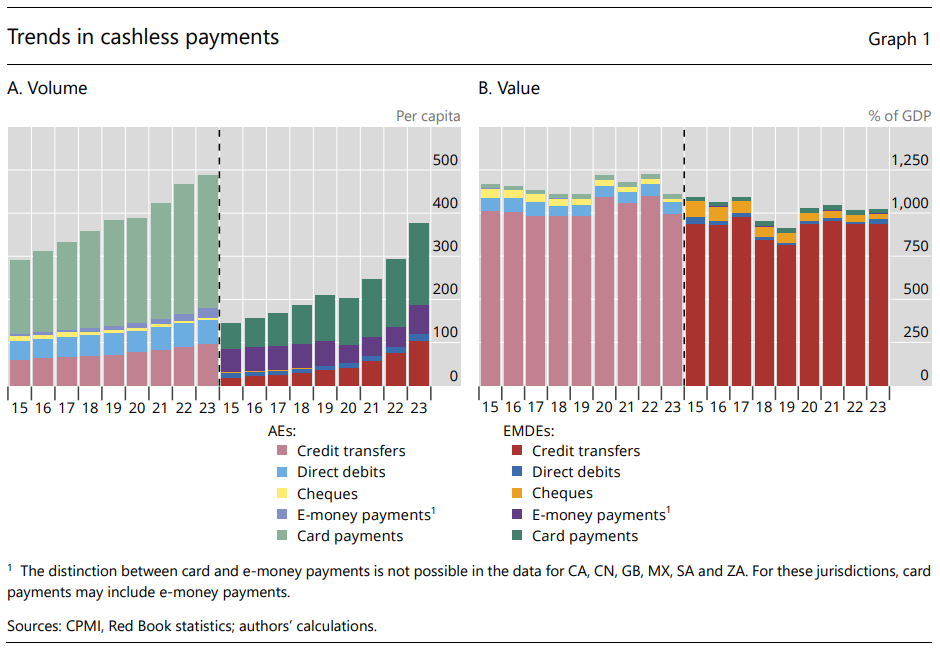

Cashless payments gained further ground

The volume of cashless payments continued to rise in 2023. The growth was especially strong in emerging market and developing economies (EMDEs) (Graph 1.A). On average, the number of annual cashless payments per capita in EMDEs grew 29%, from 293 to 377, compared with 4% (from 468 to 487) in advanced economies (AEs). In particular, the use of credit transfers (+35%) and e-money (+48%) grew strongly in EMDEs. In many EMDEs, the rise in credit transfers was primarily driven by growing use of fast payments.

On average, the per capita annual number of both credit transfers and e-money payments was higher in EMDEs (104 and 68, respectively) than in advanced economies (98 and 22, respectively). One additional noticeable difference between the two groups of jurisdictions is the use of payment cards. On average, in AEs, cards were used 306 times per person in 2023, as opposed to 188 times in EMDEs.

The value of cashless payments as a percentage of GDP generally declined or plateaued (Graph 1.B). In AEs, it fell 9%, returning to pre-pandemic levels, mainly driven by a drop in the total value of credit transfers. In EMDEs, it remained at the same level as in 2022. This, combined with the strong increase in number of cashless payments, suggests that digital payments are used more often for smaller amounts. For example, the average value of a credit transfer declined by 9% in AEs (from $6,808 to $6,169) and by 21% in EMDEs (from $4,051 to $3,220).

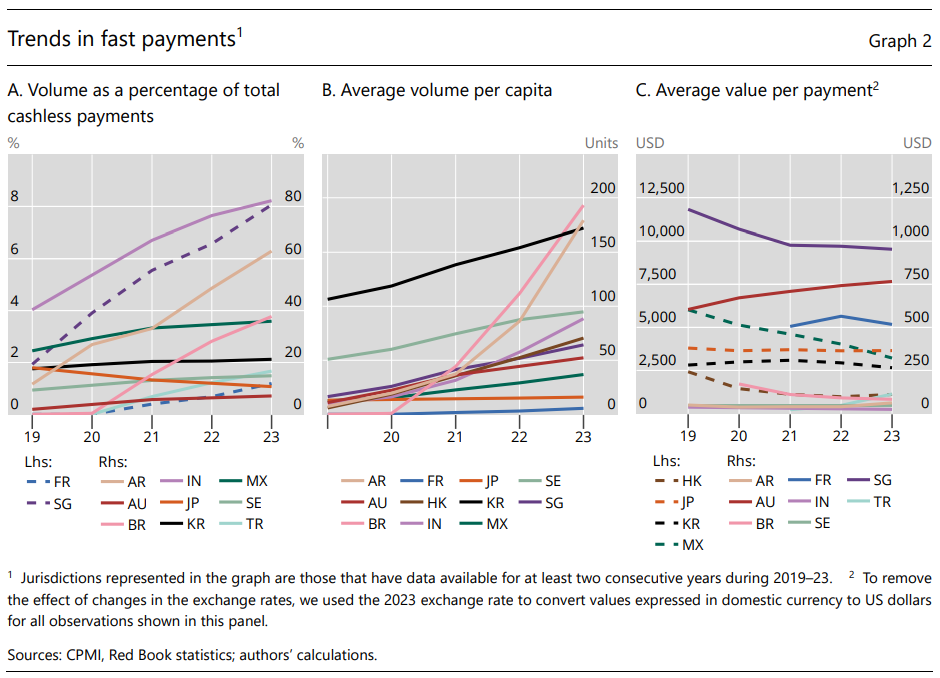

The uptake of fast payments varies between jurisdictions

Over the last decade, many jurisdictions have introduced fast payment systems and services, and more will be launched in the coming years (CPMI (2021); World Bank (2021)). While most CPMI jurisdictions have at least one fast payment system or service, the use of fast payments is more widespread in some jurisdictions than in others. In 2023, the number of fast payments as a percentage of total cashless payments ranged from 1% in France and 7% in Australia to 63% in Argentina and 82% in India (Graph 2.A).

In terms of payments per capita, Brazil and Argentina, in particular, saw significant growth in 2023 (Graph 2.B). As a result, the number of fast payments per person per year was highest in Brazil (193) and Argentina (179), followed by Korea (172) and Sweden (95).

Large jurisdictional differences exist in terms of the average size of fast payments (Graph 2.C). It was highest in Japan ($3,652), Mexico ($3,218) and Korea ($2,658), and lowest in Argentina ($62), Sweden ($47) and India ($24). Apart from differences in the cost of living, this may reflect differences in the type of transactions using a fast payment (eg person-to-business transfers or person-to-person transfers) and the existence and level of transaction limits.

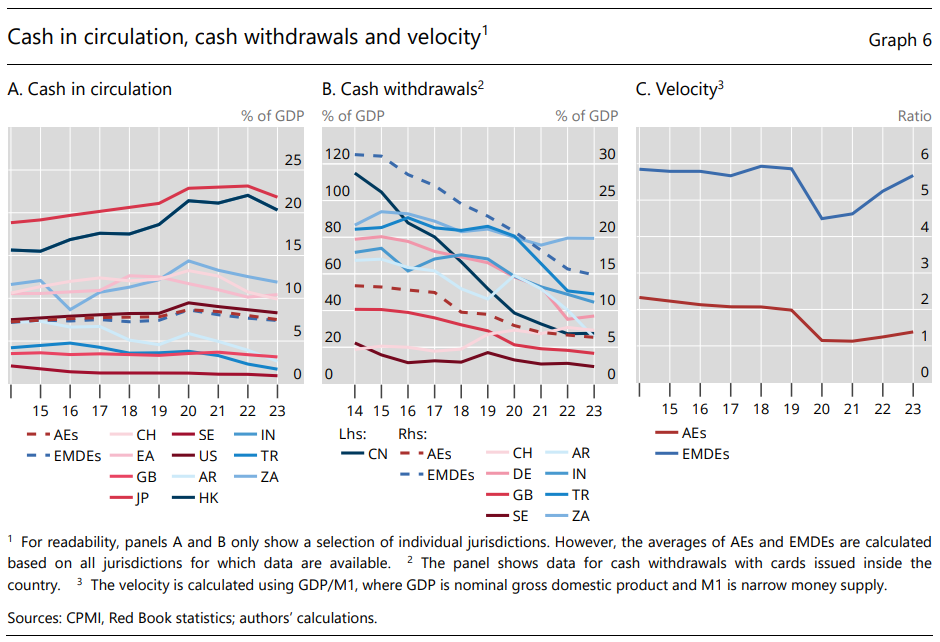

Cash in circulation steadily declined further, while cash withdrawals stabilised

In 2023, cash in circulation continued to decrease in most CPMI jurisdictions (Graph 6.A). As a percentage of GDP, it was nearly the same in AEs as in EMDEs (8% and 7%, respectively). However, there were large differences between jurisdictions. It was highest in Japan (22%) and Hong Kong SAR (20%) and lowest in Sweden (0.9%) and Türkiye (2%).

Of all outstanding cash in circulation, only the smaller denominations are generally used for payments. For that reason, cash withdrawals are often taken as a better indicator of the use of cash as a means of payment than the total value of cash in circulation. After having declined for many years, cash withdrawals as a percentage of GDP generally stabilised in 2023 (Graph 6.B).

While cash in circulation was similar in AEs and EMDEs, the value of cash withdrawals was generally lower in AEs (6% of GDP) than in EMDEs (15% of GDP). This may suggest that cash is used more as a store of value in AEs than in EMDEs, and more as a payment method in EMDEs than in AEs. This hypothesis would be consistent with the lower velocity of money in AEs (Graph 6.C), indicating that money (both cash and deposits) circulates less quickly in AEs than in EMDEs.

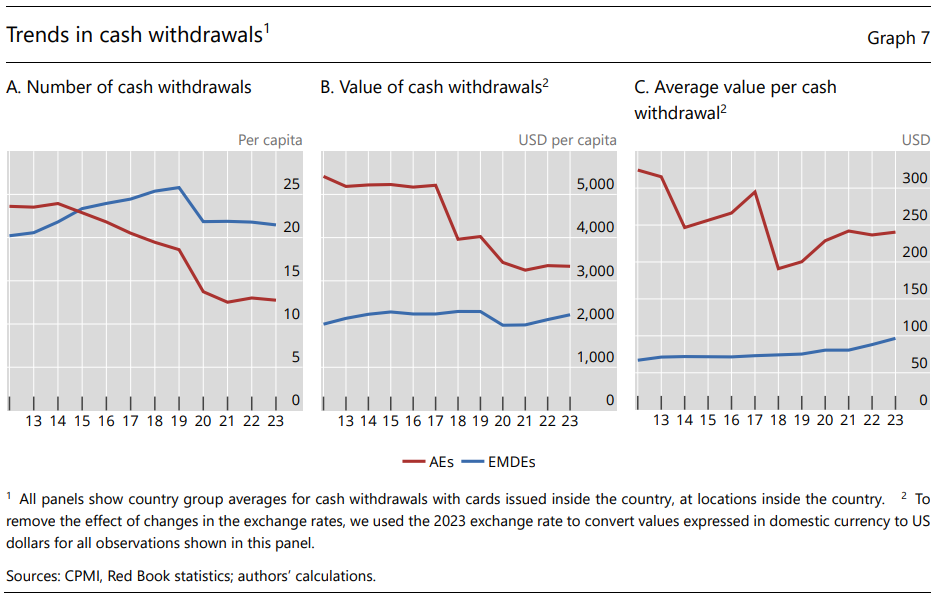

The demand for cash in terms of number of withdrawals per capita also stabilised in most jurisdictions in 2023 – across both AEs and EMDEs (Graphs 7.A). Notably, the number of withdrawals per person was roughly one and a half times higher in EMDEs (21) than in AEs (13). The average withdrawal value in AEs barely changed compared to 2022 (from $237 to $240). It increased slightly from $88 to $97 in EMDEs (Graph 7.C)

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: