BIS Bulletin – ecommerce in the pandemic and beyond

The Covid-19 pandemic has accelerated the adoption of e-commerce. The BIS Bulletin introduces novel data sources to assess these developments. It looks at conjunctural developments and how these may persist and lead to more structural changes after the pandemic has abated.

Key takeaways

• E-commerce has ramped up during the pandemic around the world. The growth has differed across sectors and over different stages of the pandemic. Novel data sources can help to follow these trends.

• The growth of e-commerce has been higher in countries where there were more stringent containment measures and where e-commerce was initially less developed.

• Some changes in consumers’ shopping habits and payment behaviour may be longer-lasting. This may have implications for structural change and the growth of the digital economy.

Data sources to assess e-commerce

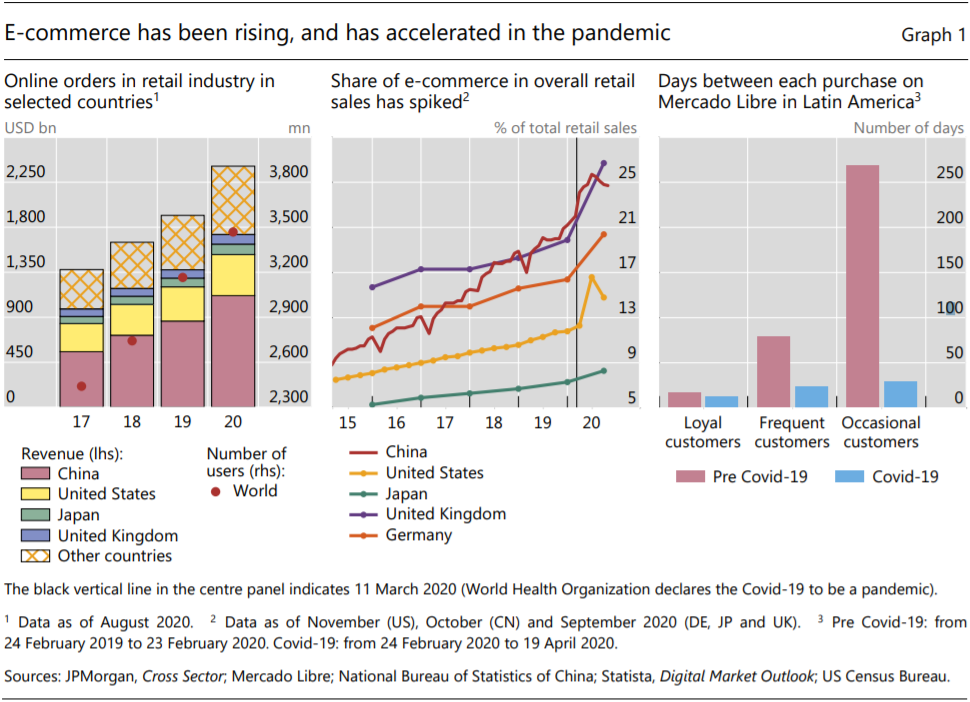

When the Covid-19 pandemic hit, the shift from bricks-and-mortar to digital shopping had been under way for some time. Since 2017, e-commerce revenues have risen from an estimated $1.4 trillion to $2.4 trillion, or about 2.7% of global output (Graph 1, left-hand panel).

Recent estimates are that 3.5 billion individuals globally (about 47% of the population) use e-commerce platforms today. China is the largest market, followed by the United States, Japan, the United Kingdom and Germany. The pandemic has accelerated this shift. The restrictions on mobility imposed to fight the spread of the virus led to a surge in online demand for many goods and services. As individuals stayed home, the online share of retail sales in China, Germany, the UK and US rose by 4–7 percentage points in 2020 (centre panel).

In China and the US, the share has recently fallen again, but remains well above its pre-pandemic level. In Latin America, one of the regions with the lowest penetration of e-commerce, in just two months consumers on the Mercado Libre platform made the number of purchases they usually did in a year. The days between online purchases have declined for both frequent and less frequent customers (right-hand panel).

A variety of data sources give insights on e-commerce. Some countries have official statistics on online retail sales (eg from the US Census Bureau and the National Bureau of Statistics of China). For a wider range of countries, there are novel sources, such as estimates from private sector market survey sources like Statista, and surveys from IBM, GlobalWebIndex, Contentsquare and others.

Finally, private sector firms collect relevant data on online sales and transactions such as card-not-present (CNP) payments. CNP transactions are remote (online) payments and payments with a smartphone app where the card is not physically presented. These are distinct from “contactless” payments, where the card is present but no signature or PIN code entry is needed (BIS (2020); Auer et al (2020)).

This Bulletin draws on the range of available data collected from these sources and in collaboration with firms like Mercado Libre and two global card networks. Table A1 in the online appendix gives descriptive statistics of selected variables. The data can also shed light on differences in e-commerce developments across countries and sectors of economic activity.

E-commerce in the Covid-19 pandemic

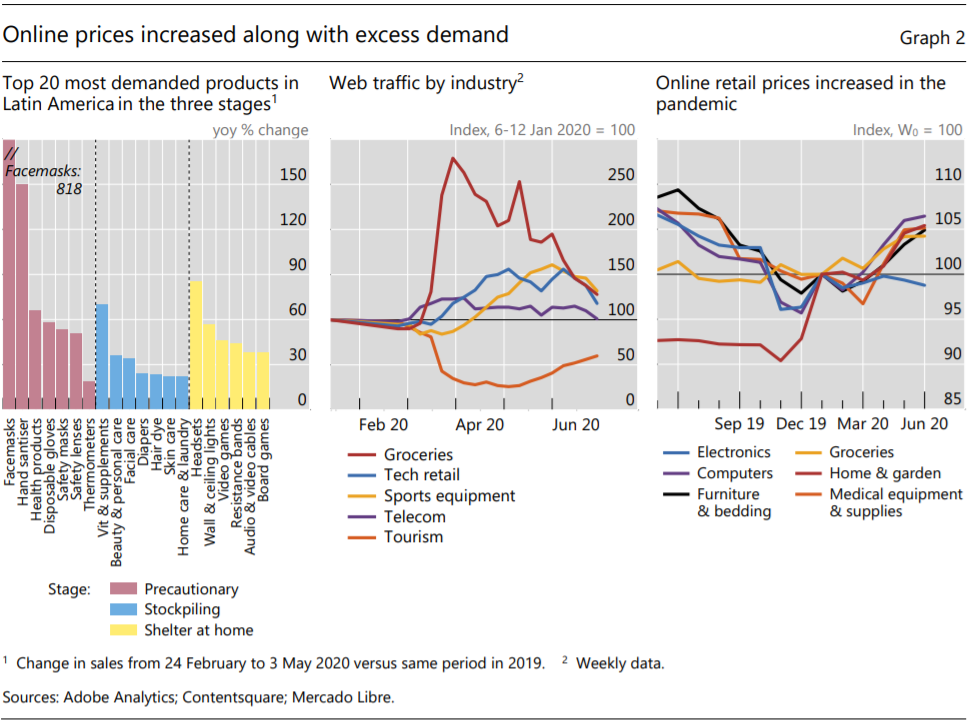

In terms of e-commerce, the pandemic unfolded in three basic stages: (i) a precautionary stage; (ii) a stockpiling stage; and (iii) a shelter at home stage. Proprietary data from Mercado Libre shed light on which products saw the highest demand in each stage (Graph 2, left-hand panel).

Initially, as the Covid-19 virus spread across Asia, Europe and the Americas, consumers made precautionary purchases of medical supplies, eg hand sanitiser, disinfectant and facemasks. In the second stage, after a pandemic was declared, consumers stockpiled household essentials such as personal care products and non-perishable foodstuffs. This is consistent with uncertainty about the length of government containment measures.

Finally, in the third stage, technological goods, exercise equipment and entertainment and education services were in high demand. This reflects the fact that more activities were being conducted at home, and teleworking and home schooling became more prevalent.

This stage was particularly important in the Americas. While in some countries in Asia and Europe lockdowns were often in place for a matter of weeks, in some parts of the US and Latin America, non-essential retailers were closed for months. In late 2020, in the light of a second wave of infections, many countries tightened containment measures again.

Different sectors of the economy were affected differently. Online orders in the retail industry rose worldwide, and the mix of goods demanded corresponded very much to the stage in the pandemic.

Data from Contentsquare indicate that traffic to supermarket web pages grew up to 270% at the peak of the lockdown (Graph 2, centre panel). Retailers of technology and sports equipment also saw a significant increase in the number of visits to their online stores. By contrast, visits to tourism pages fell by 80%.

Prices of many online products rose in the pandemic. Excess demand caused some products to go out of stock in the short term. Moreover, the cancellation of passenger flights significantly reduced transport capacity for cross-border postal shipments and other small deliveries. As a result, many customers faced delays or cancellations of their orders (WTO (2020)).

Supply chain factors, shortages and spikes in demand contributed to a sudden increase in online (including shipping) prices (Graph 2, right-hand panel). The reversal in the deflationary price trend is particularly evident for computers, home products and medical equipment sold online. Grocery prices rose slightly, especially since April. While the macroeconomic effects were limited, the change in online product prices reflects the well documented ability of e-commerce retailers to quickly adjust their prices to online competition (Cavallo (2018)).

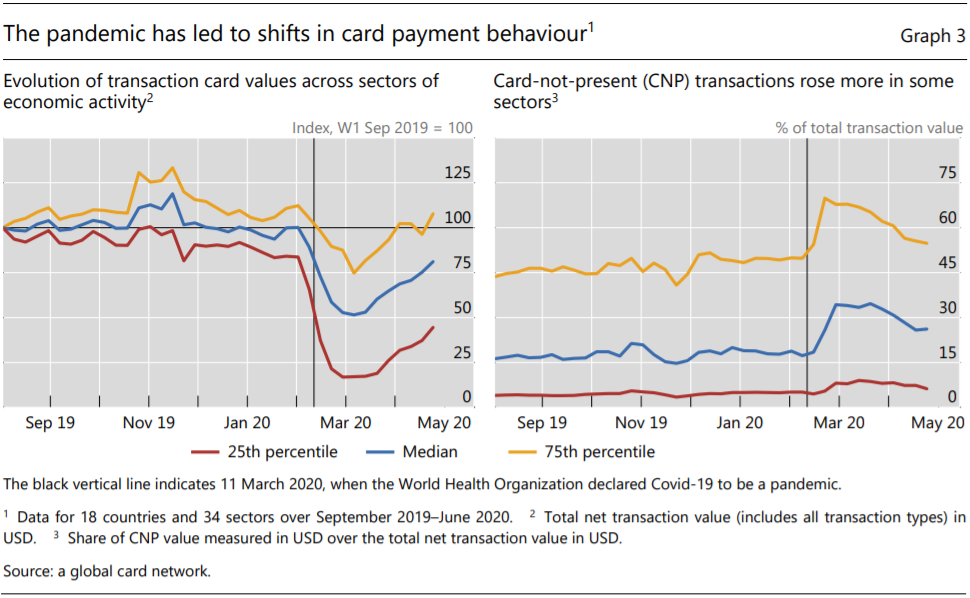

E-commerce is driving greater use of remote payments. Around the globe, overall card transactions fell during the pandemic as economic activity contracted. Again, some sectors were more heavily impacted than others, in line with the economy-wide reallocation (Graph 3, left-hand panel). Yet among card payments, CNP transactions in particular have risen. Once again, selected sectors have seen a greater increase in the CNP transaction share (Graph 3, right-hand panel).

There are indications that the shock to consumer behaviour may become structural. In particular, while the share of CNP transactions has fallen from its pandemic-period peaks, it remains higher than its pre-pandemic level in a number of economies, notably emerging market economies (EMEs). While some sector-specific shocks are probably temporary (Chen et al (2020)), others may indicate a longer-term reallocation of economic activity (Carstens (2020)).

E-commerce platforms are also adapting their product offerings and services. For instance, some have offered new products and employed automated technologies such as robots and drones for last-mile delivery. Some have used new channels for commerce such as livestreaming on social media, and introduced new services such as online education and telemedicine in their overall offerings (see online annex).

E-commerce beyond the pandemic

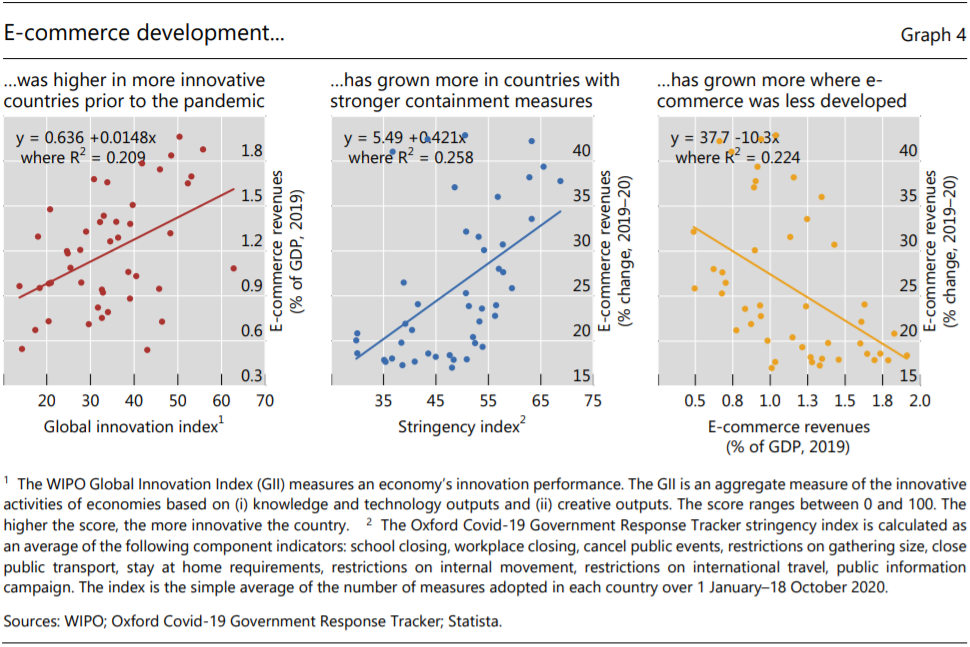

The pandemic has intensified a “catching-up” process in e-commerce growth among countries. Prior to the pandemic, there was a strong correlation between e-commerce revenues to GDP and the innovation capacity of an economy (Graph 4, left-hand panel), as measured by the WIPO Global Innovation Index (WIPO (2020)). During the pandemic, e-commerce growth has been faster where containment measures were stricter, as measured by the Oxford Covid-19 Government Response Tracker stringency index (Graph 4, centre panel).

Interestingly, the growth has been higher where e-commerce was less developed. The lower the level of e-commerce in a given country in 2019, the higher its growth rate during the Covid-19 pandemic. This implies that countries with very low e-commerce volumes have been catching up (Graph 4, right-hand panel). This is broadly confirmed in regressions analysis, also controlling for the possible presence of outliers (see online appendix).

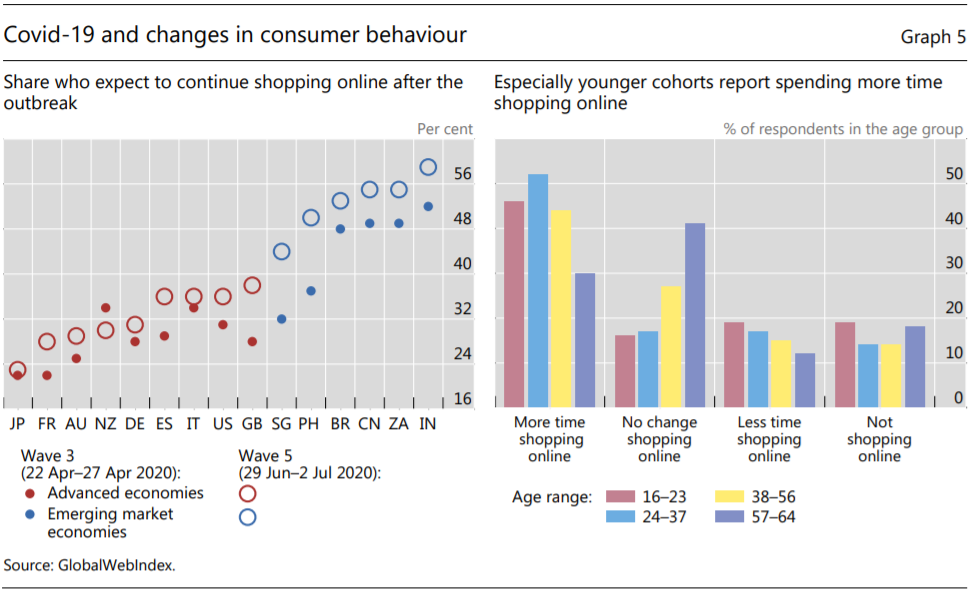

Changes in consumer behaviour may be long-lasting. For large parts of the population, the closure of physical stores has forced consumers to question deep-seated shopping habits. In a sample of 18 countries, a rising share of adults expects to shop online more frequently after the pandemic. Especially in EMEs, this share has increased since April (Graph 5, left-hand panel panel). Consumers expect both athome delivery and “buy online, pick up in-store” to rise (GlobalWebIndex (2020)).

Similarly, a survey by IBM (2020) of 3,450 executives in 20 countries finds that more than three quarters expect more shopping and customer service interactions to take place online after Covid-19. E-commerce may thus continue to thrive. That would echo the experience during the 2003 SARS epidemic, when the number of e-commerce firms in Asia rose from very low levels (South China Morning Post (2020)).

Trends in e-commerce diffusion that would have otherwise taken several years to unfold materialised in a few months. Younger users, in particular, report spending more time shopping online than before the pandemic (Graph 5, right-hand panel). As these cohorts age, these habits may have a structurally important impact on aggregate retail behaviour in coming decades.

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: