![]()

![]()

Belgium’s big four banks (Belfius, BNP Paribas Fortis, ING and KBC) are joining forces to set up an integrated network of bank-neutral ATMs that aims to accommodate changing consumer behaviour towards the use of cash.

„All four banks want to create a smart distribution of ATM devices that offer smart accessibility and which, at the same time, significantly increases the opportunity to make cash deposits. Any bank with an ATM network in Belgium can join the initiative.”, according to the press release.

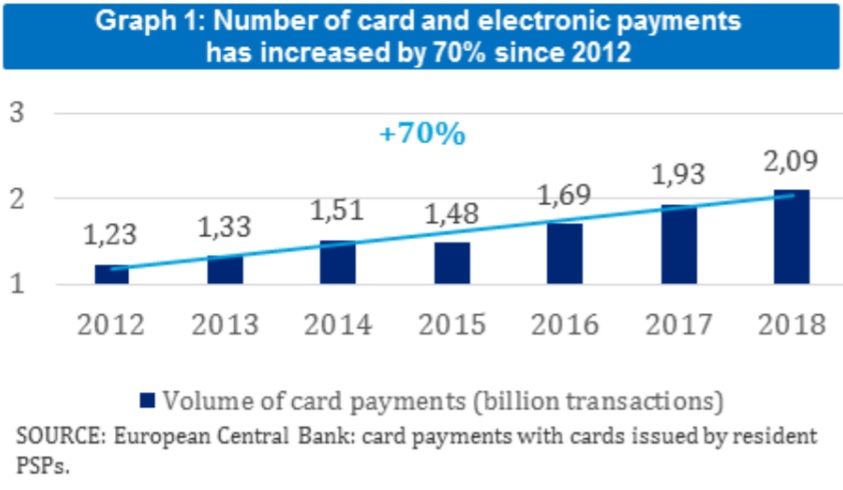

The Belgian payments landscape has changed dramatically over the past 30 years. The rapid increase in popularity of digital means of payment throughout society has been a catalyst for change. Nowadays, paying by card is standard in most retail premises and consumers are quick to pick up on new developments (including contactless payments, mobile payments with Payconiq and payments made by alternative means such as smartwatches, wearables, Apple Pay, Google Pay, etc. – see Graph 1).

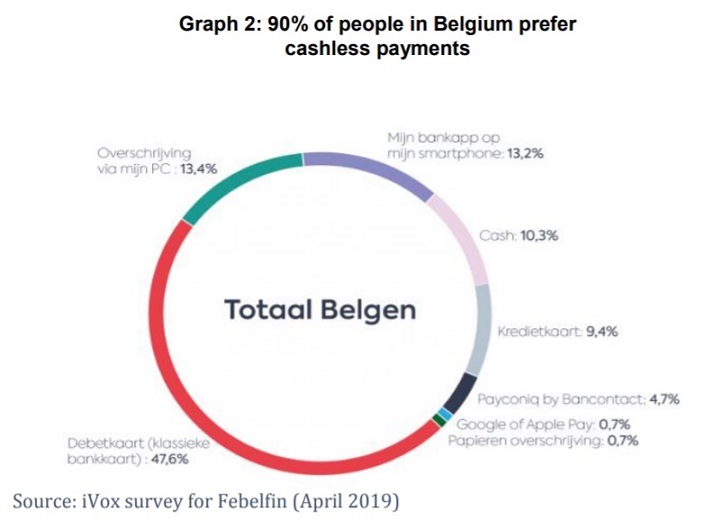

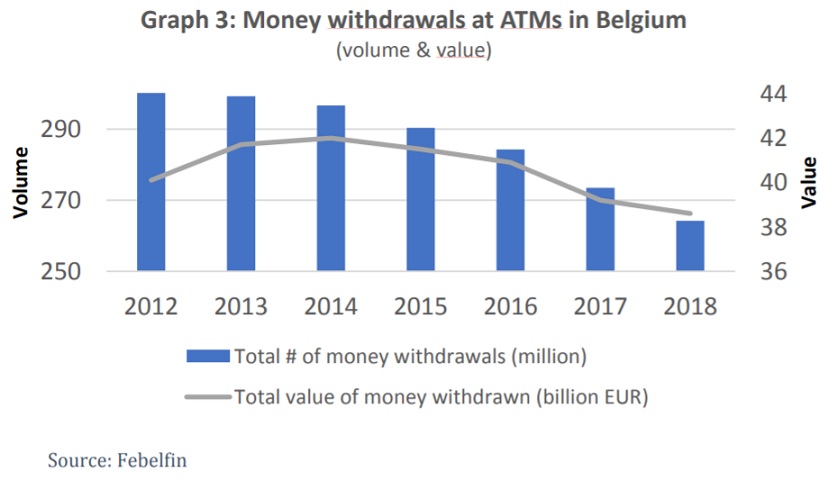

Febelfin figures (see Graph 2) show that 90% of people in Belgium prefer to pay electronically rather than in cash. This change in payment behaviour has consequences for the use of cash. Since 2012, there has been a systematic decline in cash withdrawals from ATMs (see Graph 3) and this decline is expected to accelerate.

Developments in the payments landscape are prompting banks to reconsider their proprietary ATM networks, partly because of the serious investments that continually have to be made in stocking ATMs and implementing security measures. Explosive attacks on ATMs have brought the matter even more sharply into focus. It is against this backdrop that the four big Belgian banks intend to work together in setting up an optimised ATM network that ensures consumers and merchants have secure access to cash facilities.

At present, there is an oversupply of ATMs in certain locations (such as large towns, cities and shopping centres), whereas there are no or hardly any ATMs in other (often remote) locations.

The new network will incorporate a more balanced distribution of ATMs. Based on real needs and objective geographical parameters, it would optimise the availability of cash facilities and limit the distance between them: 95% of people in Belgium would have access to an ATM no further than five kilometres away. Of course, in large towns and cities, ATMs would be more densely located to ensure optimum availability. The number of locations will be determined at a later stage, based on a site coverage plan drawn up by an external agency.

Since as many of the new network’s ATMs as possible will be installed off-premises or at stand-alone sites, the presence of a branch will no longer automatically mean that an ATM is located there. The availability of cash, therefore, will be independent of decisions relating to the branch network.

The roll-out of the new network will be phased, with the first new ATMs appearing around mid2021. The new network will also significantly increase the opportunity to make cash deposits. Customers and merchants will be able to continue using their cards in the way they always have.

The four banks will provide more information on their initiative to any interested parties in the weeks and months ahead. They are opening up their project to all banks with an ATM network of their own in Belgium.

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: