Banks struggle with global payments that look easy for apps like Alipay or WeChat

Corporations demand app-like service for cross-border payments. China’s Alipay, WeChat have shown how quickly money can move – Bloomberg’s article.

General Electric Co.’s Kristen Michaud is a top client in a business that generates $1 trillion a year for banks – and she’s deeply frustrated. Michaud helps run GE’s cash-management system, using 200 banks and 8,000 accounts to move money to remote corners of the world. When sending cash, she doesn’t always know how much intermediaries might nibble away in fees, or when it will reach suppliers. Payments can pass from bank to bank, arriving in strange amounts with memos erased, leaving recipients confused.

“You might have a supplier calling you up saying they didn’t get paid and then you’re spending days working with multiple banking partners to chase down the status,” Michaud said. “It could take multiple days for a bank to respond.”

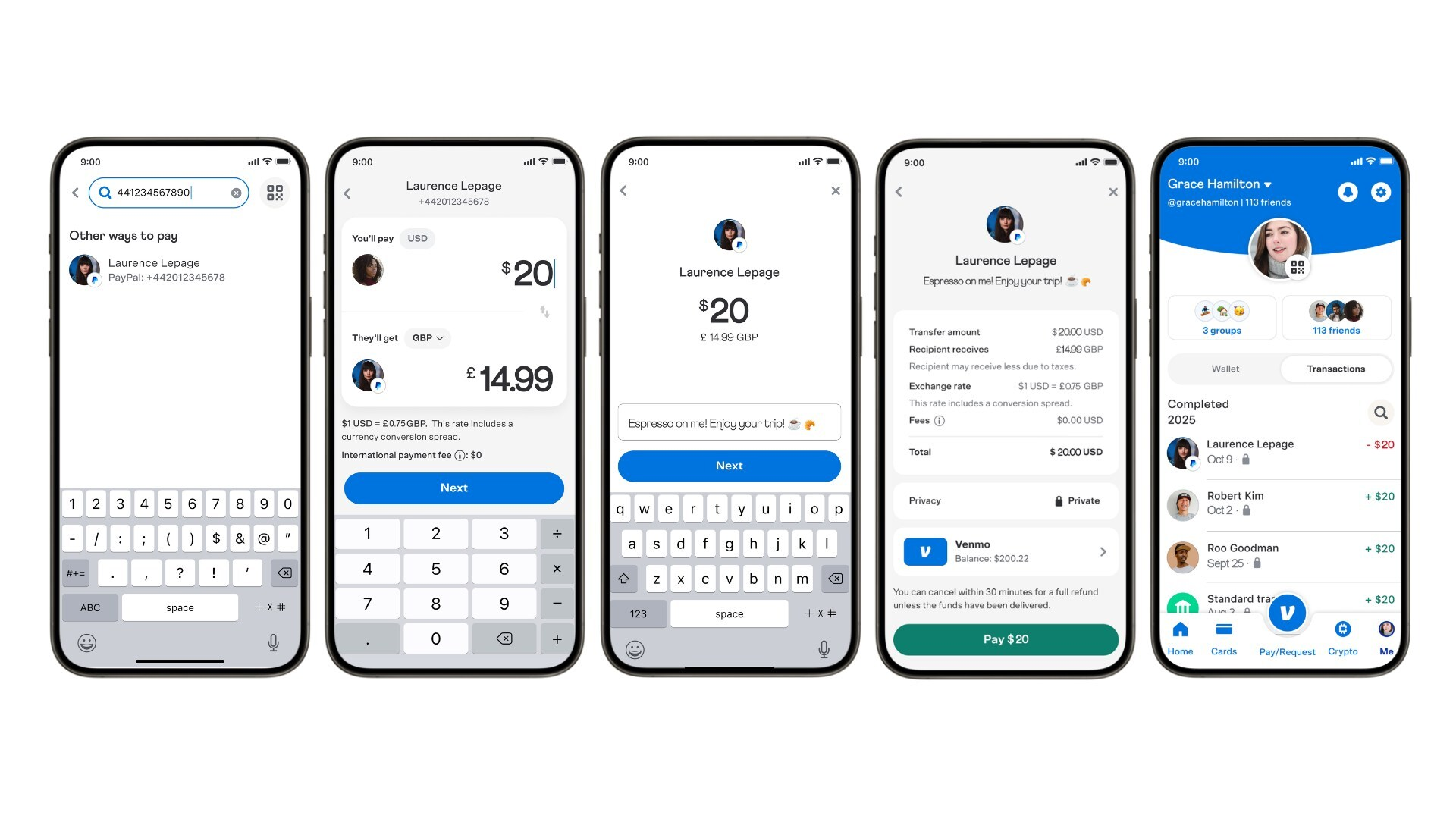

Payment apps – such as Chinese juggernauts Alipay and WeChat Pay – are making the movement of money look so easy that banks’ biggest customers are losing patience with the global patchwork that’s handled their funds for decades. Such apps have barely started serving multinationals, but their presence is putting pressure on financial firms to up their game, or risk losing their grip on another business.

Corporate treasury officials such as Michaud have been expressing growing exasperation at industry conferences, sometimes contrasting the slow, opaque system they use with Chinese apps and services such as PayPal Holdings Inc.’s Venmo that beam money almost instantly between consumers and retailers. If technology can help millennials split a restaurant bill in seconds or let tourists tap phones to pay taxis abroad, why must companies sometimes wait three to five days to confirm their money reached its destination?

“We’re coming into this age that’s more digital,” Michaud said. “Similar to the Amazon example, you want to know if your package was delivered to your house or to your apartment, and so the same should hold true with a payment.”

Banks say they’re working on improvements. And so far, corporations are sticking with them because of their proven security for both money and data. Even if apps enhance services to lure big companies, banks will undoubtedly strive to fend them off. The stakes are high, because handling cross-border payments is especially lucrative.

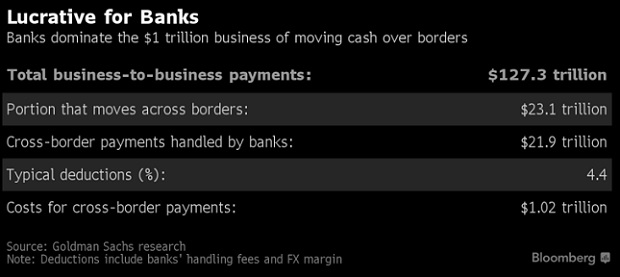

The $23 trillion in corporate money that flows over borders annually is dwarfed by the $104 trillion that moves between businesses within their own countries, but it generates about half of the revenue that facilitators collect. Banks dominate international money flows, handling about 95 percent. Along the way, banks and their partners deduct about $1.02 trillion in fees and foreign-exchange costs, according to Goldman Sachs Group Inc.

Much of the innovation in payments in recent years has occurred on the consumer side, as tech startups sought to wrest business from banks, which then fought back with apps of their own. Many upstarts carry out transactions within their own ecosystem, instantly shifting money from one account to another.

That contrasts with the network corporations use when moving money overseas. They rely on the correspondent banking system, which links domestic banks with foreign counterparts. In a cross-border payment, a corporation’s money may jump from one bank to the next in a chain several links long, with each setting its own timeline and fees along the way.

Harry Newman, the head of banking at SWIFT, the messaging system that connects 10,000 financial institutions around the world, concedes the existing system needs to improve.

“Correspondent banking has been around for a long time and it’s done a good job for many years,” he said in an interview. “But it’s obviously a child of the ’80s and it lacked the transparency and predictability that you really want to see in a modern payments mechanism.”

Cautionary tale

SWIFT has been working on a plan for making overseas transfers more efficient. In a campaign, known as the global payments innovation initiative, SWIFT partnered with banks around the world to help give corporate clients more information on fees and real-time updates on transactions. That transparency pushes correspondent banks to work faster and keep fees competitive. Chinese banks, already facing the stiffest competition from apps, are among the most enthusiastic supporters, according to Newman.

Beyond fintechs, banks are also looking at new technologies to continue their push to improve their treasury services offerings. JPMorgan Chase & Co. has partnered with 75 banks in its Interbank Information Network, which uses blockchain to speed cross-border payments.

For the financial industry, the cautionary tale is China, where banks learned that payments and commerce can happen largely without them. Money there now flows mainly through Alibaba Group Holding’s Alipay and Tencent Holdings Ltd.’s WeChat Pay, which combine social media, commerce and financial services. Consumers sent more than $2.9 trillion inside the two systems in 2016. Could corporations be next?

“The innovations of consumer payments in Asia are redefining the entire payments landscape,” said Manish Kohli, global head of payments and receivables inside Citigroup Inc.’s treasury management business. “This will have an impact on the world of business-to-business and institutional payments.”

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: