Banks remain robust but higher interest rates could impact their asset quality, the EBA finds. „Operational risks remained elevated for EU/EEA banks driven by cyber and data security”.

The European Banking Authority (EBA) published its Q3 2023 quarterly Risk Dashboard (RDB) together with the Risk Assessment Questionnaire (RAQ). The publication also includes information on minimum requirement for own funds and eligible liabilities (MREL). EU/EEA’s banks remained highly profitable, well capitalised and maintained robust liquidity. Banks expect the asset quality to deteriorate as higher interest rates affect borrowers.

. The economic activity in Europe remains subdued and macroeconomic uncertainty is high as the monetary policy response to high inflation is still working its way through the economy, easing inflationary pressures materially during the last months of 2023.

. EU/EEA banks maintained robust capitalisation levels, with weighted average CET1 ratio (fully loaded) at 15.8%, 10bps lower than the historical high of 15.9% reported in the previous quarter and 100bps higher than September 2022. RWAs slightly increased, mainly driven by credit risk.

. MREL shortfall appeared marginal at 0.25% of RWAs on EU/EEA level as of Q2 2023, yet two countries reported a MREL shortfall between 5% and 7% of RWAs.

. Liquidity ratios remained at high levels, despite their slight decrease. Market funding conditions remained benign, as banks managed to issue more, by November 2023, across nearly all debt classes than in previous years.

. Tightened lending standards observed across the EU have so far not led to a decrease in outstanding loans to non-financial corporates (NFCs) and households. Yet, loan growth remained subdued. The autumn risk assessment questionnaire (RAQ) showed that banks were reluctant to increase their lending exposures.

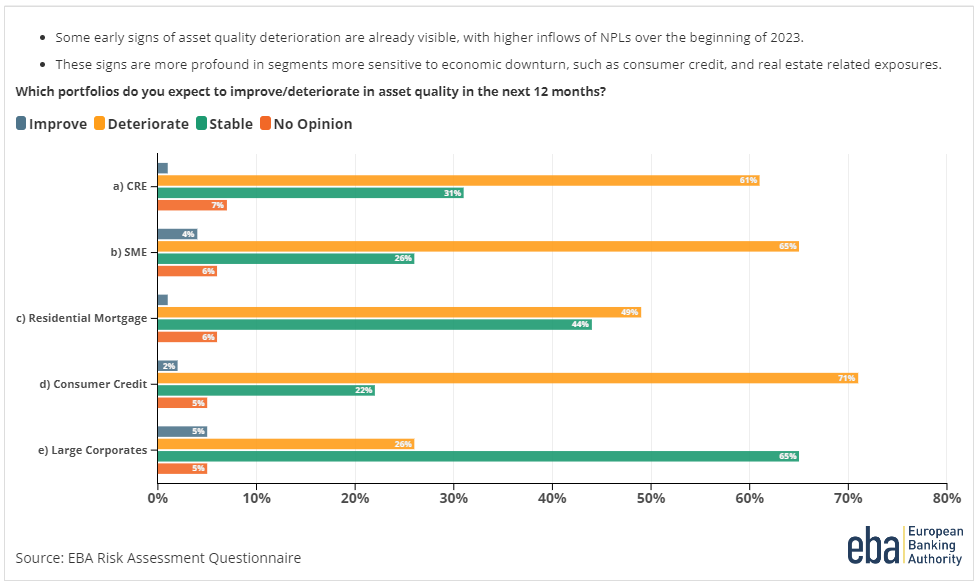

. Asset quality remained robust. Real estate related exposures (both commercial and residential) appear more vulnerable, as a higher share of banks, compared to previous RAQ, expect a deterioration in the asset quality of these portfolios.

. Return on Equity (RoE) of EU/EEA banks was reported at 10.9%, supported by widening net interest margins (1.62% in Q3 2023) and net interest income generation.

. Operational risks remained elevated for EU/EEA banks driven by cyber and data security, followed by conduct and legal risks, similar to previous RAQs. An increasing share of banks, compared to previous RAQs, cites fraud as a main operational risk.

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: