![]()

![]()

Anyone can be a banker these days, you just need the right code, writes Reuters.

Global brands from Mercedes and Amazon to IKEA and Walmart are cutting out the traditional financial middleman and plugging in software from tech startups to offer customers everything from banking and credit to insurance.

For established financial institutions, the warning signs are flashing.

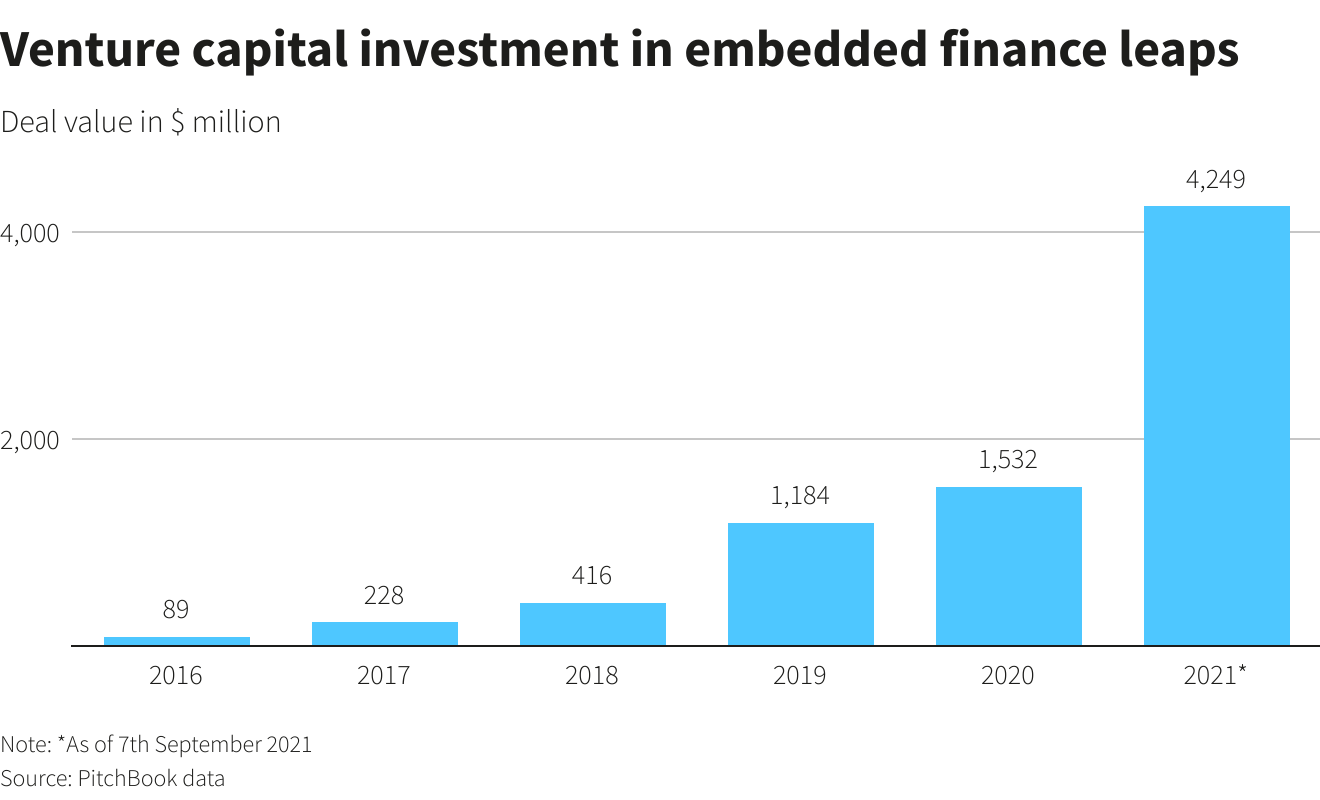

So-called embedded finance – a fancy term for companies integrating software to offer financial services – means Amazon can let customers „buy now pay later” when they check out and Mercedes drivers can get their cars to pay for their fuel.

To be sure, banks are still behind most of the transactions but investors and analysts say the risk for traditional lenders is that they will get pushed further away from the front end of the finance chain.

And that means they’ll be further away from the mountains of data others are hoovering up about the preferences and behaviours of their customers – data that could be crucial in giving them an edge over banks in financial services.

„Embedded financial services takes the cross-sell concept to new heights. It’s predicated on a deep software-based ongoing data relationship with the consumer and business,” said Matt Harris, a partner at investor Bain Capital Ventures.

„That is why this revolution is so important,” he said. „It means that all the good risk is going to go to these embedded companies that know so much about their customers and what is left over will go to banks and insurance companies.”

WHERE DO YOU WANT TO PLAY?

For now, many areas of embedded finance are barely denting the dominance of banks and even though some upstarts have licences to offer regulated services such as lending, they lack the scale and deep funding pools of the biggest banks.

But if financial technology firms, or fintechs, can match their success in grabbing a chunk of digital payments from banks – and boosting their valuations in the process – lenders may have to respond, analysts say.

Forrester analyst Jacob Morgan said banks had to decide where they want to be in the finance chain.

„Can they afford to fight for customer primacy, or do they actually see a more profitable route to market to become the rails that other people run on top of?” he said. „Some banks will choose to do both.”

And some are already fighting back.

Citigroup has teamed up with Google on bank accounts, Goldman Sachs is providing credit cards for Apple and JPMorgan is buying 75% of Volkswagen’s payments business and plans to expand to other industries.

„Connectivity between different systems is the future,” said Shahrokh Moinian, head of wholesale payments, EMEA, at JPMorgan. „We want to be the leader.”

The full article here

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: