And when the Great Unlock happens, what happens to challengers?

an article written by Chris Skinner, the author of the bestselling books Digital Bank, ValueWeb and its new sequel Digital Human.

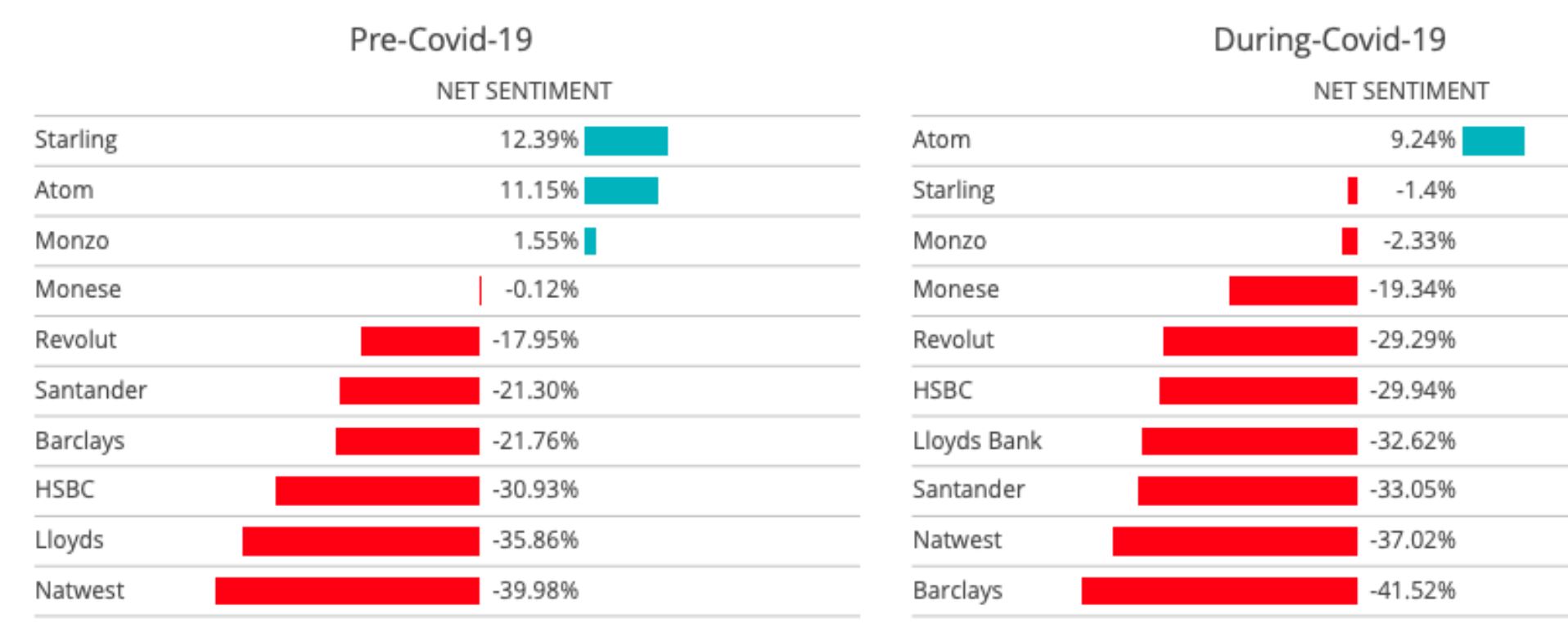

As I ponder the world and everything, this article by Jemima Kelly in The Financial Times keeps coming back to me: The virus has crushed the challenger bank dream

In it she says things like: There comes a time in your life that you realise that some of the friends you used to consider good friends aren’t actually your true friends. These are your party friends. They’re great in the good times, but they lose their charm, or function, when something bad or life-altering happens to you (like losing a loved one or getting seriously ill, for instance).

And: The phenomenon known as “fintech” grew up in the good times, in the aftermath of the global financial crisis. Fintech firms were great during these party years … but the party years are over.

And concludes: In life, when things get rough, you often find yourself back in touch with those old friends and family members who you shunned when you just wanted to party. They might not have been as cool and exciting as your new friends, but they won’t let you down when things get scary.

I can see a simplistic view here. The view that Monzo and Revolut are stumbling and therefore the whole FinTech sector is tainted. Unsurprisingly, I don’t agree.

The real thing here is that there are two camps: traditional and start-up (or is that upstart?). When the pandemic hit, these two camps were split into two further camps: those who were ready and those who were not.

For me, the upstarts who weren’t ready can be forgiven. We have said for years that the upstarts would be hugely challenged when a downturn hit, because they’ve never been through one. Those how rely on credit and loans will probably die, unless their algorithms are solid and robust. As they’ve never been tested, we’ve no idea if they are solid and robust. Those who are trying to grow, based upon a growth model that has to be sustained, will be severely tested as growing during a time of lockdown is almost impossible. That’s where Monzo and Revolut have their issue.

Nevertheless, there are many who are thriving during this period. They were built on solid foundations and can see the end of the pandemic becoming stronger and larger. Some of these are challenger banks like Atom, who relied on asset-backed mortgage markets, rather than a credit card or growth model. Some of these are firms that enable buy now and pay later, like Klarna, as Jemima points out.

However, to question the whole FinTech buzz as just a party animal? Nah. FinTech is more solid than just a few good years of frivolousness. FinTech has a long-term future, and will seriously challenge aspects of finance that didn’t work well from financial inclusion to financial wellness to pure customer focused service.

Which brings me to the traditional banks or, if you’d rather, the incumbents.

As I said last week, they won’t die … but some are anemic. Some are zombies. Some are the Walking Dead.

For me, this was typified by one of the big UK banks who depended upon a customer contact centre in India. India closed with four hours’ notice. With no backup contact centre in the UK, and the almost impossible task of creating one with zero notice, meant that this big UK bank has spent months being uncontactable. Worse than this, they then had issues with their online banking. The result? Lots of disgruntled customers.

I blogged about this yesterday – brace yourself for the great unlock – but the bottom-line is that there are as many incumbents who were unready for the lockdown, in the same way as there were many upstarts who weren’t ready.

The main challenge for upstarts is two-fold: funding and business model.

The main challenge for incumbents is also two-fold: WFH and digital.

Upstarts who were well-funded in March are doing fine; upstarts who have a solid business model and a method of building a business are doing well; upstarts who depended upon the good time marketplace are struggling, as Jemima points out.

Incumbents who were nearly digital in March are doing fine; incumbents who have a business model they have been implementing that is digital, are doing well; incumbents who depended upon the old branch model of banking and had not committed to digital properly are struggling.

There are two sides to this coin.

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: