Romanian banks face four strategic priorities after the high-interest-rate era, including a „radical reduction in cost to serve, not just the branch network”, says Kearney

European Retail Banking Radar, Kearney’s latest study, now in its 18th edition, shows that Europe is entering a period of normalization following the exceptional conditions of 2023–2025. For Romania, however, the challenge extends beyond the normalization of interest rates. It comes at a time when the banking sector must simultaneously navigate a high fiscal deficit, fiscal consolidation measures, weak economic growth, inflation above the EU average, pressure on households’ disposable income, downgrade risk and rising external funding costs, as well as political volatility and uncertainty surrounding the reform agenda.

At the same time, Romania’s banking market continues to consolidate. Banca Transilvania has completed the integration of OTP Bank, UniCredit has merged with Alpha Bank, and the consolidation trend continues to gain momentum.

Against this backdrop, four strategic priorities are emerging for Romanian banks:

1. Profit resilience: „Protect earnings before chasing growth.”

For many banks, the 2027–2028 period will be defined less by aggressive growth strategies and more by cost discipline, risk management, capital optimization, collections, repricing and customer retention. In this environment, M&A transactions are not only growth opportunities but also a way to absorb fixed costs, capture economies of scale and maximize returns on technology and digital investments.

2. Shift the growth engine from „beta rate” to volume growth and relationship banking.

Banks need to accelerate sustainable lending, particularly across mortgages, secured consumer lending, and SME/micro-enterprise financing, supported by digital underwriting and increasingly granular customer pricing. Romania benefits from a strong deposit base, a large customer base and high card adoption, yet it is still not converting these strengths sufficiently into higher lending volumes, investments, insurance penetration and deeper day-to-day customer engagement.

3. Radically reduce the cost to serve—not just the branch network.

A cost-to-income ratio (CIR) of around 59% in Romania, compared with approximately 54% across Europe, suggests that digitalization has often focused on the front end rather than on end-to-end operating model transformation. Products, processes, legacy IT systems, back-office operations, as well as onboarding, servicing and collections all require simplification. Otherwise, consolidation risks adding complexity rather than efficiency. Artificial intelligence has the potential to become a key differentiator.

4. Build meaningful fee income streams.

To date, Romanian banks have largely benefited from strong net interest income (NII). As interest rates normalize, growth in non-interest income (NCI) will become critical to sustaining profitability. Payments, wealth management, bancassurance, subscription-based services and merchant ecosystems will become increasingly important sources of growth. European Retail Banking Radar shows that banking sector growth across Europe is gradually returning to pre-windfall levels, and Romania will not be immune to this trend.

Looking back, many banks successfully captured the benefits of the higher-rate environment but did not reinvest those gains sufficiently into structural transformation. Digital adoption increased, but monetization has remained limited. In many cases, operating models and branch networks have remained overly complex, fee-income propositions have not evolved sufficiently, and business models have remained focused on prudence rather than expanding banks’ role as broader financial intermediation platforms.

Florian Teleabă, Partner Financial Institutions, Kearney:

“Romanian retail banks have successfully captured the benefits of the higher interest rate environment. The next challenge—and the next source of value creation—is to translate this advantage into sustainable growth driven by stronger customer relationships, more diversified revenue streams and higher productivity, rather than balance sheet expansion alone. I don’t believe bank boards and CEOs are primarily concerned about whether growth will slow below 8%. Their real challenge is entering a more demanding operating environment before fully addressing the structural issues around operational efficiency, customer base monetization and risk management.”

European context

Southern European countries, affected a decade ago by the debt crisis and banking restructurings, are now among the best-performing retail banking markets in Europe, according to the 18th edition of Kearney’s European Retail Banking Radar 2026.

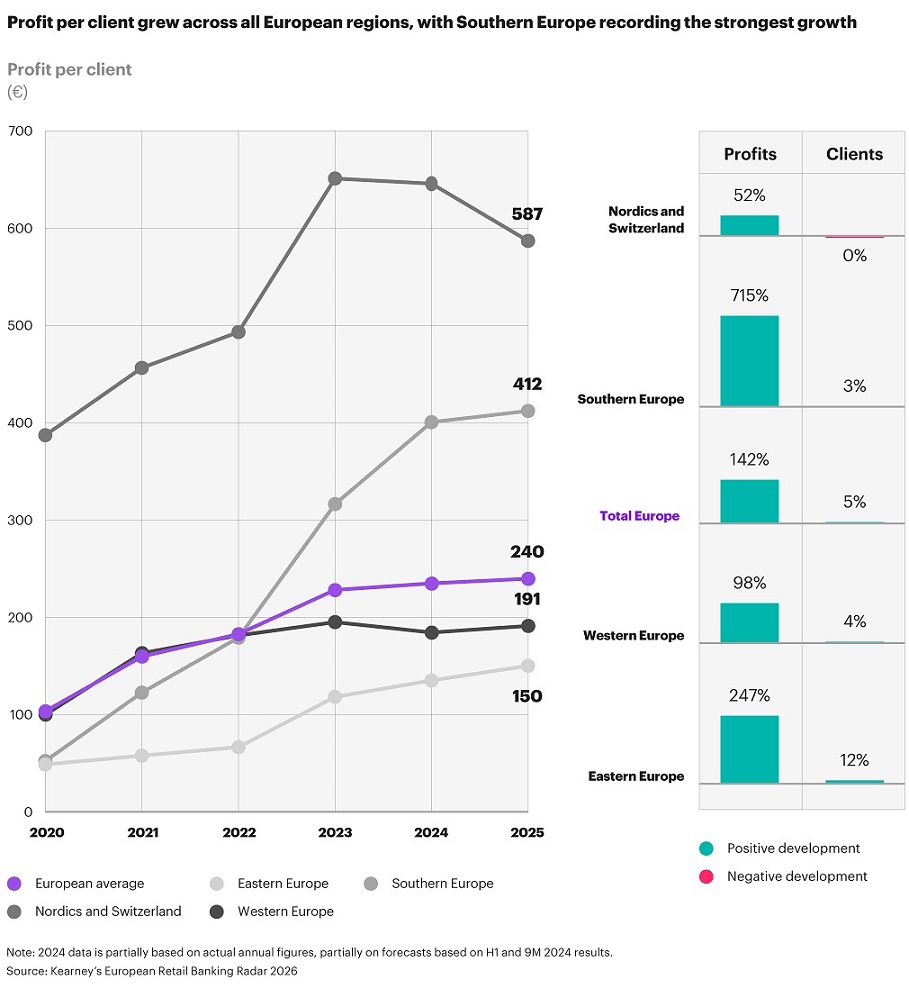

A decade ago, banks in Southern Europe were the sector’s weak link, weighed down by bad loans, bailouts and restructuring. Kearney’s data over the last few years shows the picture has completely changed. Profit per customer across Southern Europe has grown 715% since 2020, far ahead of Western Europe at 91% and Eastern Europe at 206%.

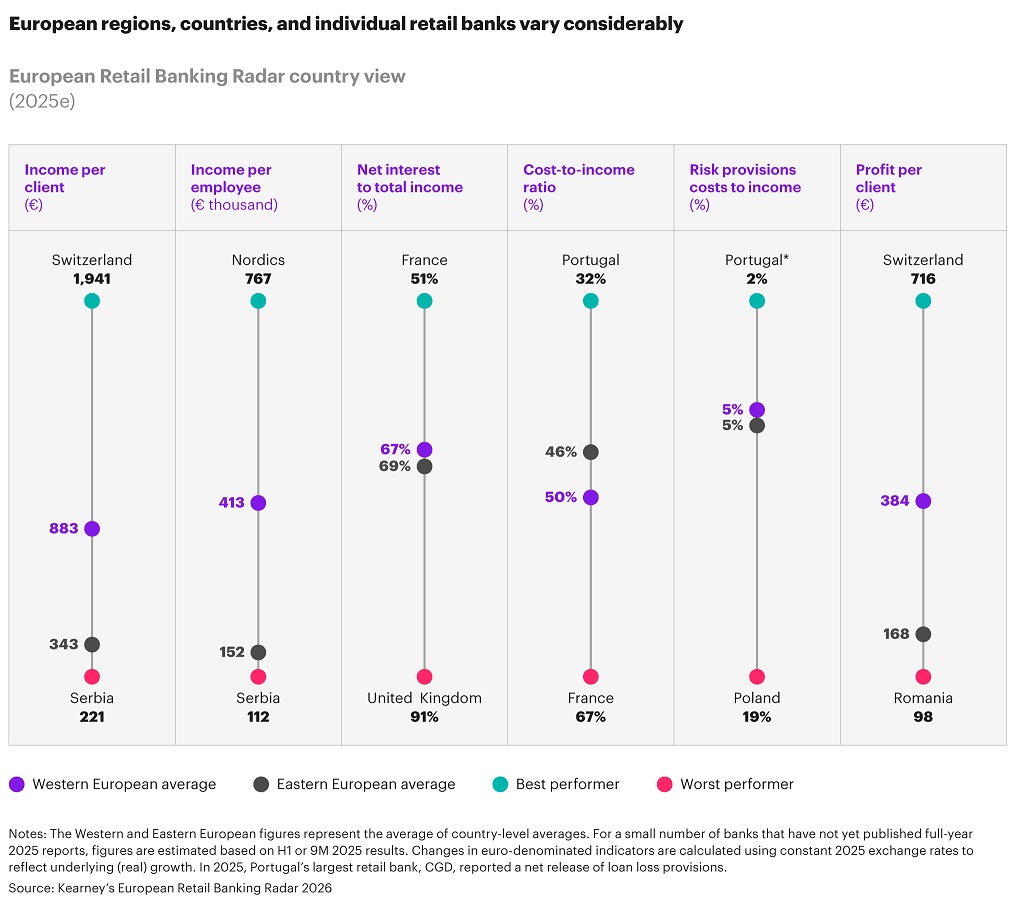

Portugal is now Europe’s efficiency leader, with a cost-to-income ratio of just 32%. Spain follows at 37%. By contrast, France has the highest cost-to-income ratio in Europe at 67%.

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: