Why apps matter: digital banks pass on monetary policy differently

Digitalisation is reshaping how banks pass on monetary policy. Compared with their branch‑based peers, digital banks are faster at adjusting deposit pricing for policy changes, but slower at updating their loan pricing.

an article by Katarzyna Budnik – Adviser ECB – Monetary Analysis Division

As more people manage their finances on a laptop or smartphone rather than at the counter in a local branch, the way monetary policy moves through banks is evolving. This blog post briefly sketches the euro area universe of digital banks – those that operate almost entirely online – and examines their behaviour over the recent monetary policy cycle.

During the 2022-23 monetary policy tightening phase, digital banks adjusted the interest rates they pay on deposits faster and by more than traditional banks. By offering higher interest rates, they kept retail deposits flowing in. At the same time they did not raise lending rates more than their peers. This compressed their margins – the difference between what digital banks earned on lending and what they paid on deposits – relative to other banks. Consequently, digital banks expanded their lending less.

Early evidence from the 2024-25 easing phase points to a partial reversal. Digital banks started to reduce deposit rates for new customers more quickly than traditional banks. This has been supporting a recovery in their margins and lessening their earlier advantage in attracting deposits. The big picture is that bank digitalisation strengthens the bank funding leg of the lending channel of monetary transmission.

Comparing digital and traditional banks

The analysis below is based on a panel of over 170 digital banks operating in the euro area, observed in supervisory reporting from 2016 to 2025. These banks can be grouped into three business types: e-retail – deposit-funded, household-facing; e-service – payments/servicing and fee-heavy; and e-wholesale – market and corporate-focused.

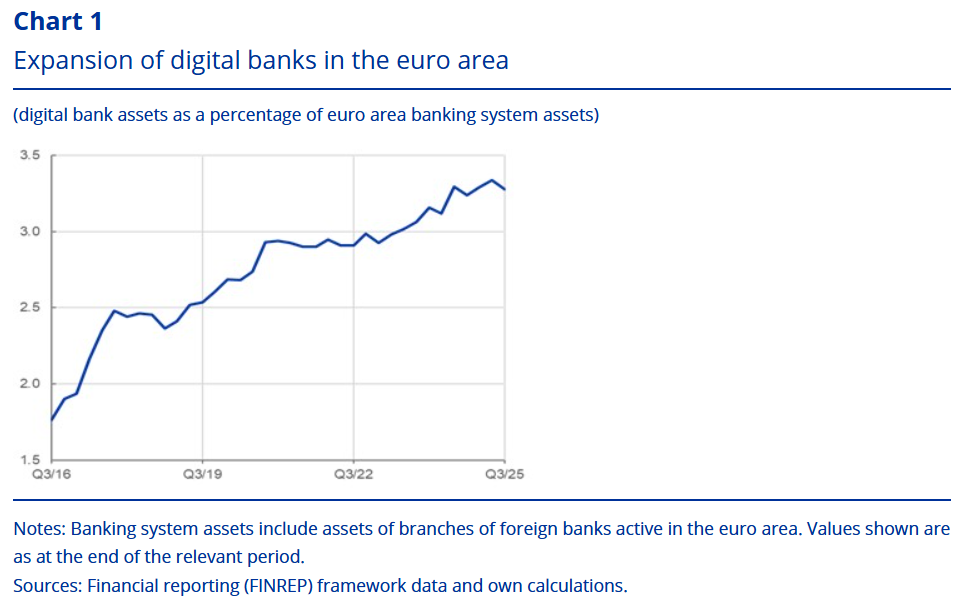

On average, digital banks are smaller than their branch-based peers. Their balance sheets rely more heavily on overnight retail deposits, include larger cash buffers and contain more intangible assets (for example software platforms, IT systems, and brand-related assets). Digital banks also generate a bigger share of income from fees and commissions alongside interest income. Their footprint in the banking system remains modest. However it has grown steadily over the past decade, with many new entrants during the low interest rate period, and the first bank closures occurring during the tightening phase (Chart 1).

Five takeaways about digital banks’ behaviour

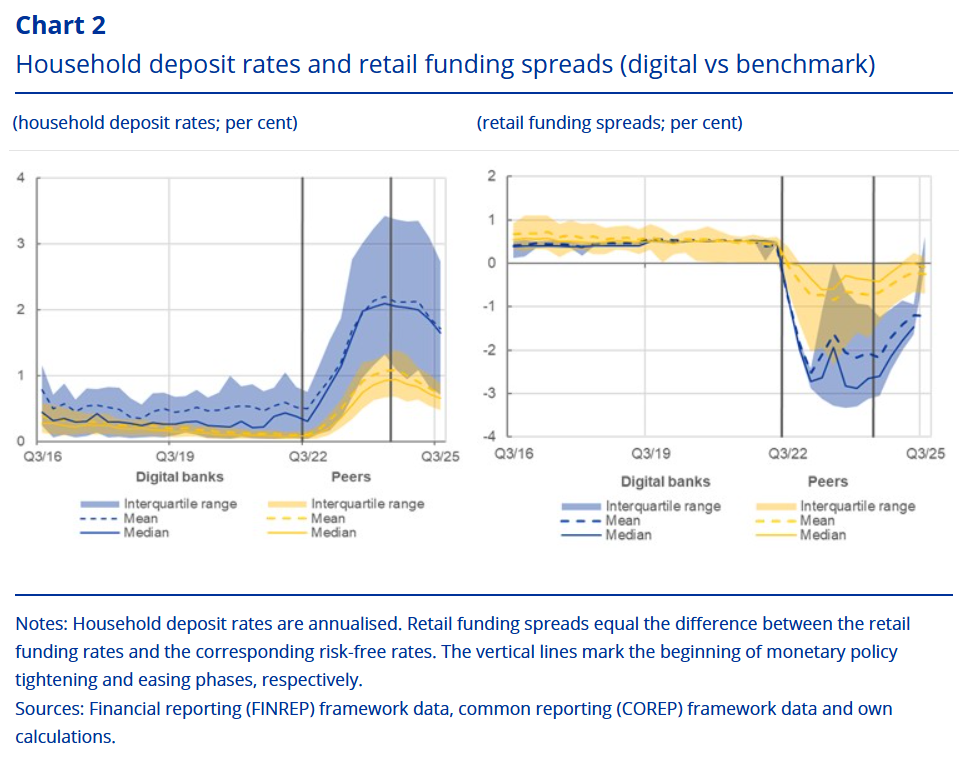

First, deposit pricing adjusts faster at digital banks. When policy rates increased, digital banks lifted household deposit rates both by more, and more quickly, than their peers (Chart 2). This pattern is strongest for stand-alone digital banks – those without the support of a broader banking group that often includes more traditional entities.

Why is that so? It reflects the nature of app-based banking, which lowers search and switching costs. Digital banks face greater pressure to reprice deposits quickly to retain customers. Group-affiliated digital banks tend to adjust more gradually, because group reputation and the branch networks of affiliated banks increase depositor trust, dampening immediate funding pressure.

Second, the loan rates of digital banks are less responsive. Despite higher funding costs, loan rates at digital banks rose by about the same amount as those of their peers.

This implies that transmission is stronger on the funding side than on the lending side for digital banks. Lending competition between digital banks and the desire to attract new customers appear to limit the extent to which they can pass on higher funding costs through loan rates.

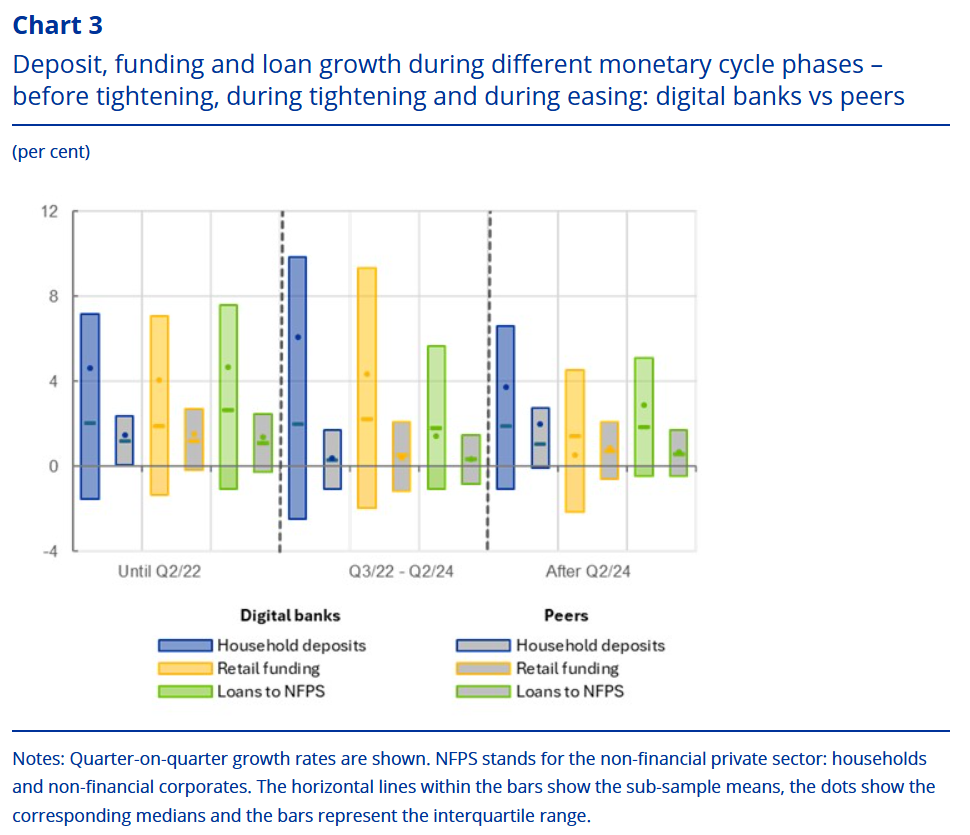

Third, prices did the heavy lifting. Digital banks kept retail deposits flowing through the tightening phase – primarily by paying their depositors well (Chart 3). At the onset of the tightening phase, there was no clear acceleration of deposit inflows to digital banks relative to peers – but there was no relative slowdown either. Their structurally high deposit inflow continued.

This suggests that adjustments during tightening occurred mainly through prices, i.e. higher deposit rates, rather than changes in deposit volumes.

Fourth, digital banks ultimately slowed down their lending compared to peers. As funding costs stayed high and loan repricing lagged, lending growth at digital banks slowed more than at traditional banks. This is consistent with their margins being squeezed.

Fifth, transmission on the funding side also occurs earlier for digital banks in the easing phase. With the first monetary policy rate cuts in 2024-25, new deposit rates at digital banks fell faster than at traditional banks, particularly for longer maturities. This helped their margins to normalise. But the earlier deposit-attraction advantage narrowed, with household deposit inflows declining relative to peers. Digital banks’ lending rates declined more gradually, remaining “sticky” on the way down.

More details: Why apps matter: digital banks pass on monetary policy differently

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: