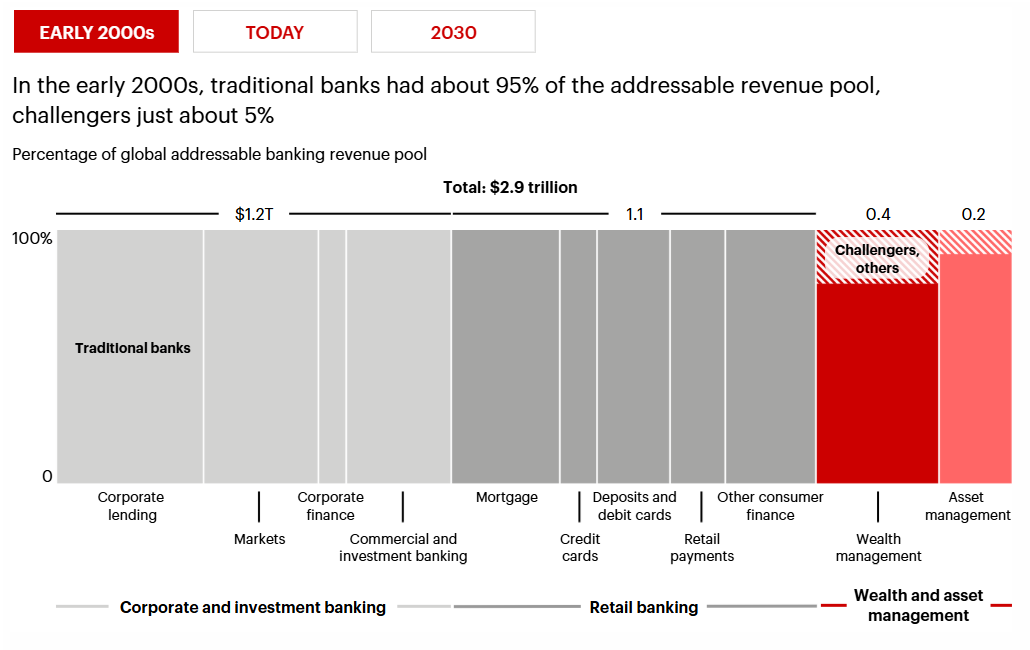

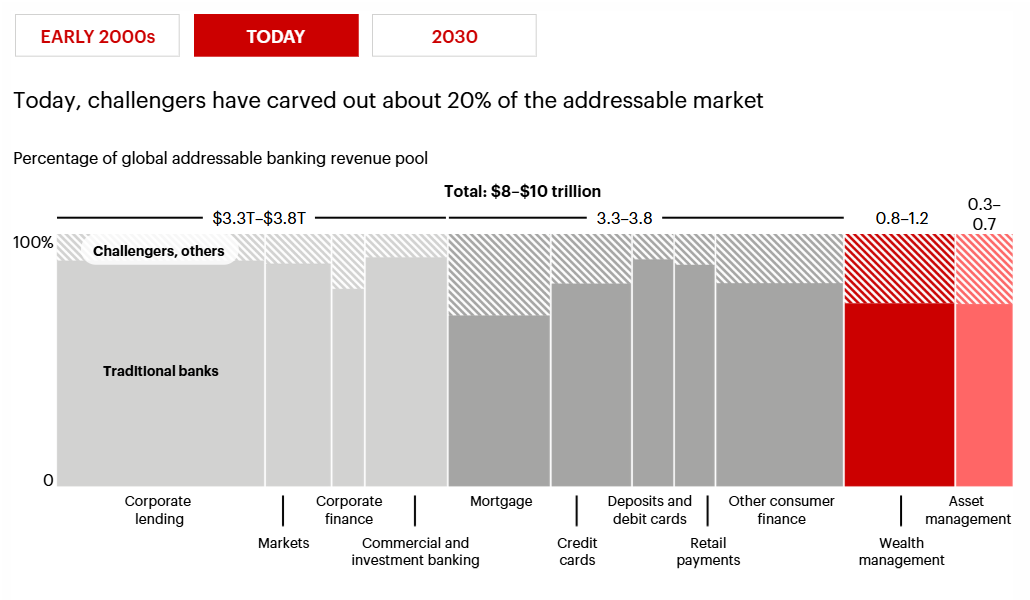

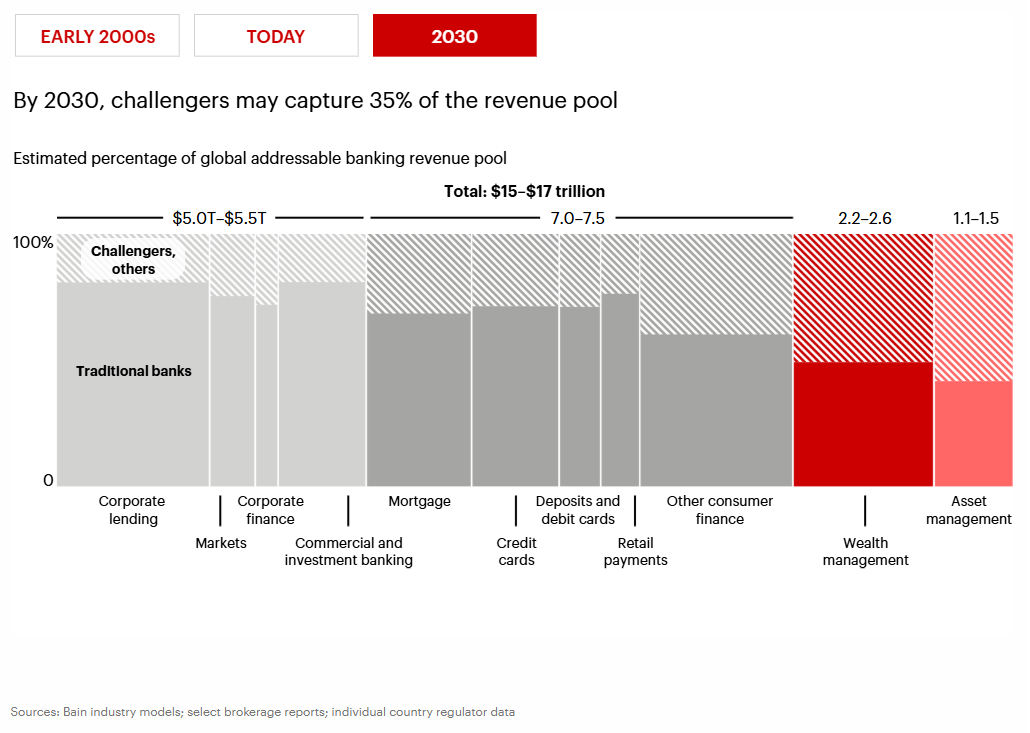

Banking revenue pool – challengers have steadily taken share from traditional banks: around 5% in early 2000s, about 20% today, and 35% by 2030

AI, direct-to-consumer models, and the return of local priorities are redrawing industry lines.

Banking is under pressure as new competitors emerge. Traditional banks now capture about 80% of revenue, down from 95% in the early 2000s. And that downward trend could continue, according to BAIN & Company.

To grasp the challenges that banks face in wealth and asset management markets, it’s worth initially scanning the broader banking landscape. Most relevant is that banks no longer compete only with each other; they are increasingly competing with tech-native platforms, public and private asset managers going direct to consumers, and decentralized finance firms. The traditional full-service, balance-sheet-heavy model is under pressure across all fronts: wealth, payments, credit, and capital markets.

Partly as a result, traditional banks have slipped from capturing 95% of the addressable revenue pool in the early 2000s to about 80% today. By 2030, we estimate they could hold only 65%, further ceding ground to fast-moving challengers emphasizing asset outperformance

Key takeaways from the Bain & Company report

. Tech-native finance firms and direct-to-consumer asset managers are gaining market share, forcing incumbent banks to defend their position across the value chain.

. From AI-driven advice to modular platforms, tokenized assets, and the return of local-market priorities, banks must redesign, not tweak, their approach.

. Owning the client interface is essential, which requires doubling down on proprietary data, trusted advice, and differentiated alpha.

. Banks can consider three strategic paths: becoming a digital gatekeeper, an alpha powerhouse, or an asset-light orchestrator, each of which involves build-buy-partner moves.

Three paths to viability

Broadly speaking, banks aiming to address the challenges head-on can consider three paths, each of which includes options to build, buy, or partner to gain the necessary capabilities and technologies.

The first path is becoming a digital gatekeeper, which might consist of an expanded mobile app plus an API ecosystem to provide customers with front-door access across retail, small business, and wealth segments. To expand the feeder network for new clients, a bank could build its own app and portal, or it could acquire a robo adviser or neobank. Rich data will be essential to provide superior insights and advice to clients, with much of that data coming from partners.

An alternative path involves becoming an alpha powerhouse with a large-scale balance sheet and an edge in using AI to analyze data. To expand geographic coverage, a bank choosing this course could invest in priority growth hubs or acquire digital banking or multi-asset traders in those key regions.

The third path creates an asset-light orchestrator that maintains a minimal balance sheet and coordinates best-of-breed partners. On most dimensions, such as investment manufacturing and advice services, the orchestrator would probably partner with specialist firms.

Banks that want to determine the best next steps should answer a set of high-gain questions:

. Should we double down on genuinely differentiated alpha engines or exit commoditized beta manufacturing altogether? What could our next-generation alpha engines look like in an increasingly efficient market?

. How will we turn proprietary data and client insights into a mass-market advisory proposition that creates a wealth management moat? How can we leverage other data assets, such as those from investment banking or transaction flows, to enhance advice?

. Through which routes can we continue to acquire more new clients over the next few years, especially if we lack major feeder channels? Which client needs and subsegments do we want to target?

. Which build-buy-partner strategies will allow us to outpace both established and emerging rivals, retain ownership of the client interface, and play a defining role in the open-finance API ecosystem?

. How will we use build-buy-partner choices in private credit, tokenized assets, and stablecoin infrastructure to unlock off-balance-sheet capital flows? And how do we protect our broader value chain from disintermediation?

. Which markets will drive 80% of our future growth, and how should we recalibrate our home-base strategy to thrive in a more protectionist world?

In a market defined by choice, customers will gravitate to the firms that earn their trust and prove, not just promise, that they can outperform.

More details here: Six Threats Demand a New Playbook for Banks in Wealth and Asset Management

Dariusz Mazurkiewicz – CEO at BLIK Polish Payment Standard

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: