Merchants in the Netherlands are showing interest in the possibilities of an ‘offline’ digital euro, a payment method that can still be used when there is no electricity or internet connection. However, they are concerned about the potential costs of a new payment method and wary of the investments required to support digital euro payments, such as new software or payment terminals. Many would prefer to continue using their existing payment infrastructure and devices as much as possible.

Merchants also place great value on customer privacy in digital payments. And they appreciate zero-downtime feature, especially point-of-sale businesses in sectors with high volumes of daily transactions (such as supermarkets, street vendors, and fuel and charging stations).

This is according to a DNB survey among a representative group of over 1,000 merchants (including shops, hospitality & catering industry, fuel and charging stations and service providers) in the Netherlands.

A payment method that works even during outages appeals to merchants

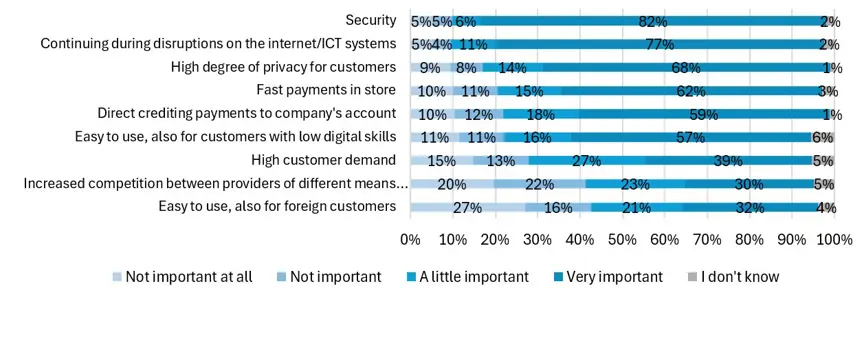

One of the key advantages of the offline digital euro is its ability to keep payment transactions running during network outages. It works without an internet connection – either on a smartphone or via a payment card – making it possible to pay even when the bank or merchant’s network is down. In this way, it can serve as a reliable backup system. This feature is among the most frequently mentioned requirements by merchants surveyed, second only to security, which is seen as a fundamental condition for any trustworthy payment method (see Figure 1).

Figure 1 – Merchants see security, privacy, and resilience during disruptions as essential features of the digital euro

Source: Conclusr/DNB survey of Dutch merchants on the digital euro, summer 2024. 1,023 respondents

The zero-downtime feature is appreciated especially among point-of-sale businesses in sectors with high volumes of daily transactions, such as supermarkets, street vendors, and fuel and charging stations. Merchants also place great value on customer privacy in digital payments. The offline version of the digital euro offers both privacy and resilience, making it a strong complement to the existing range of digital payment options available in the Netherlands.

Merchants want equal or lower costs

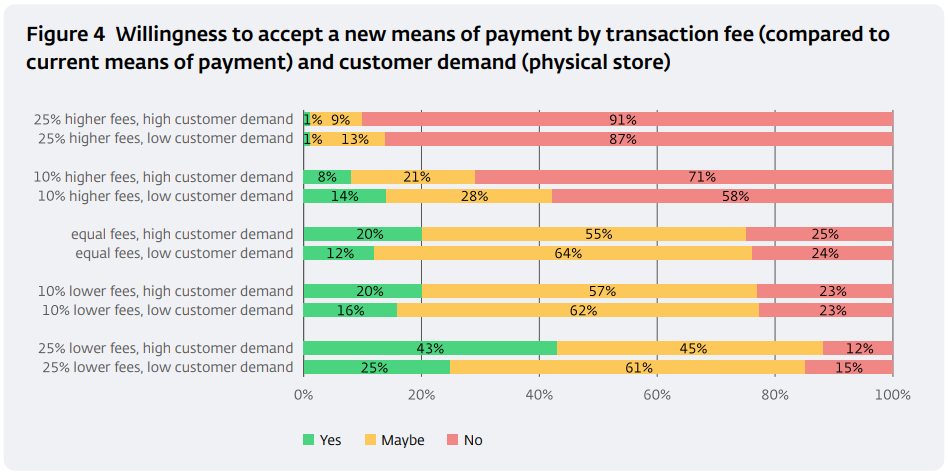

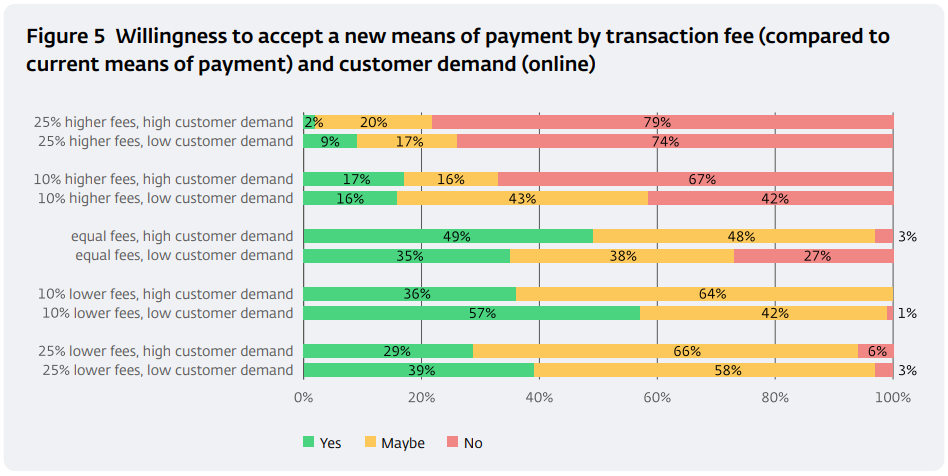

Merchants are concerned about the potential costs of a new payment method: 79% fear that transaction fees for digital euro payments could be higher than those of existing options. They believe the costs should be equal to – or preferably lower than – those of current mainstream payment methods. In addition, two out of three merchants are wary of the investments required to support digital euro payments, such as new software or payment terminals. Many would prefer to continue using their existing payment infrastructure and devices as much as possible.

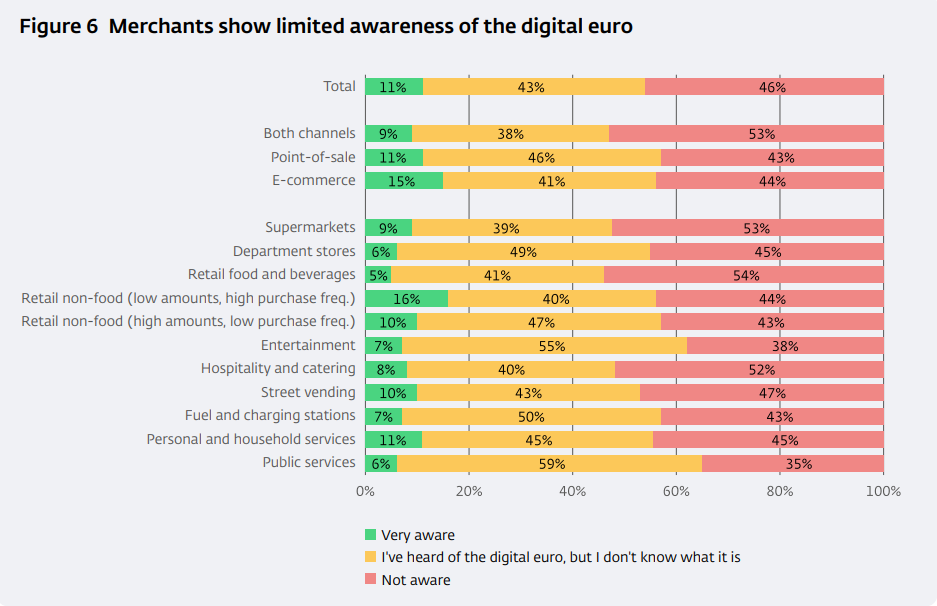

Awareness of the digital euro among merchants is limited

Awareness of the digital euro remains low among the merchants. Nearly half (46%) say they are not familiar with it at all, while 43% have heard of it but do not know exactly what it is. Only 11% consider themselves well informed. This limited awareness is consistent across different sectors and among both small and large merchants. One likely explanation is the lack of active communication so far, as no political agreement has yet been reached on the introduction of the digital euro.

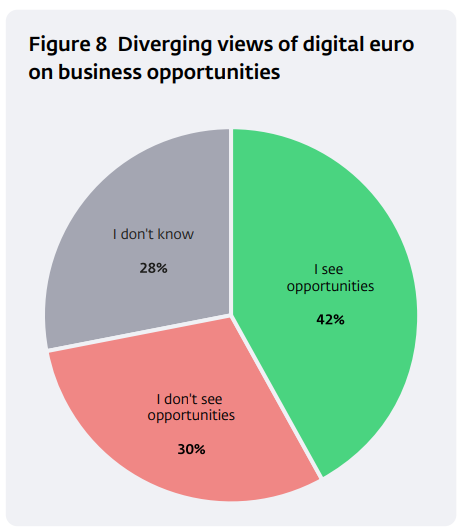

Approximately 42% of merchants see potential opportunities associated with the digital euro (figure 8). Larger non-food retail chains, such as drugstores and kiosks, are especially optimistic.

Among those who do, the most frequently mentioned benefits include enhanced ease of use for consumers and reduced vulnerability to system outages, particularly due to the possibility of offline transactions. This latter point is especially salient in industries characterized by continuous transaction flows, such as supermarkets, street vendors, and fuel and charging stations, and less so in the hospitality and catering industry. In contrast, 30% of retailers see no such opportunities.

The authors of the study conclude that „Dutch merchants are not yet convinced of but open to the digital euro’s benefits, especially its offline use. They need assurance that adopting it will be easy, inexpensive, and risk-free. Policymakers must shape the introduction of the digital euro in accordance with these insights to ensure the digital euro is embraced as a welcome innovation.„

More details: Occasional study – Attitudes of Dutch merchants towards the digital euro

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: