In this exclusive EPC interview, Eric Véronneau – an expert in banking and payments – shares invaluable insights from his extensive industry experience, reflecting on the evolution of the EPC and the future of payments in Europe. Véronneau provides a thoughtful and engaging perspective on the past, present, and future of European payments.

You have been actively contributing to the EPC’s activities for many years, including the establishment of the SCT and SDD schemes. How has the EPC evolved over time?

At the beginning, the European Payment Council (EPC) was very focused on delivering the two basic Single Euro Payments Area (SEPA) payment schemes. Over the years, the EPC then had to adapt its organisation and its working streams to the evolutions of the payment landscape. This can be seen in the maintenance of the running schemes as well as in the development of new schemes, either payment schemes or schemes servicing payments like SEPA Request-to-Pay (SRTP) or SEPA Payment Account Access (SPAA). Here, one of the difficulties for the EPC is to feel and gauge which industry trends will be successful. In this, the quality and knowledgeability of its board and general assembly members is key.

What are the most important developments that the European payments landscape has experienced over the last five years?

The last five years have been characterised by a rapid digitalisation of payments and the emergence of new payment solutions that are either completely separate to existing payment means or built on top of them – for example, EPC schemes or card payments. This movement has been accompanied and encouraged by a growing desire for instantaneity or certainty of payment and by the use of mobile phones as the central devices for making any kind of payment.

What do you think about the digital transformation of payments today?

The digital transformation allows the use of credit transfers in purchasing situations where the card payments were prevalent. This is clearly the case on the internet and also a reality at the point of sale. The European Payments Initiative (EPI) with its Wero offer is the expression of this evolution, as are SPAA and RTP.

How do you see the European payments landscape evolving in the next five years?

The distinction between card payments, credit transfers, and direct debits will continue to disappear. The service provided to the customer in support of their purchase or their need to transfer funds will become paramount. Such services will be provided either to the payer or the payee and they will drive the evolution of the payment solutions.

Is the instantaneity important? In which situation and for which of the actors, the payer or the payee? Will services like deffered debit and/or Buy Now, Pay Later (BNPL) be transposed to credit transfers and direct debits? Which type and which modality of reimbursement will be offered? Which type of reporting?

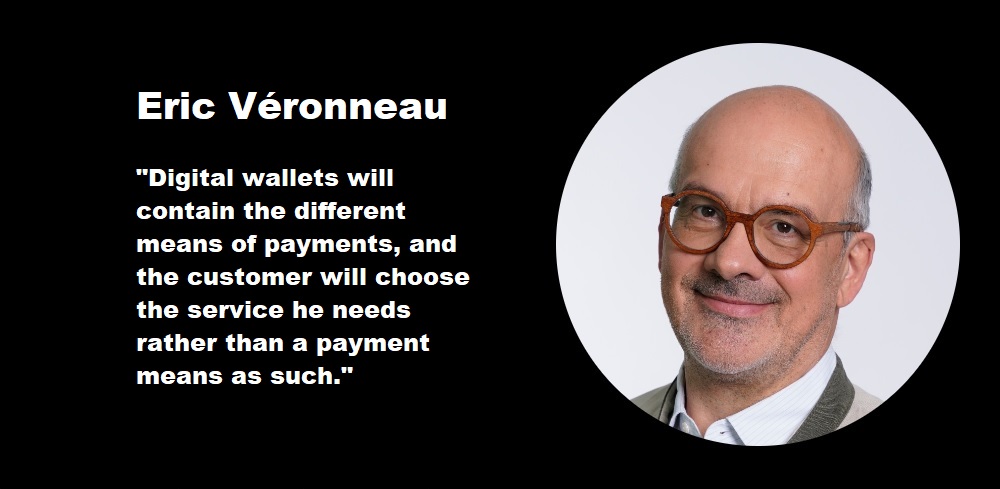

Digital wallets will contain the different means of payments, and the customer will choose the service he needs rather than a payment means as such. And the growing interoperability possibilities between payment systems will allow the expansion of this evolution to international payments, from or to the European Union (EU). The EPC is already looking in this direction with the One-Leg Out Instant Credit Transfer (OCT Inst).

Certainly, the options for the European Central Bank (ECB’s) retail electronic euro and its date of entry into force may also change the landscape but will not change this trend of ‘service first’.

Banking 4.0 – „how was the experience for you”

„To be honest I think that Sinaia, your conference, is much better then Davos.”

Many more interesting quotes in the video below: